GERMAN AUCTION PREVIEW: 2.50% Nov-32 Bund

Sep-24 09:07

This morning, Germany will reopen its on-the-run 7-year 2.50% Nov-32 Bund (ISIN: DE000BU27014) for E4bln.

- The launch auction of the line on August 27 was very soft with only E3.170bln of bids received for the intended E4.0bln transaction. Today’s auction will be for the same E4bln size but we note that in Q4 there will only be one auction with a smaller E3bln size, on October 21. If there was more flexibility in the DFA’s funding programme we expect today’s auction would have been downsized after the first was held, too.

- Specifically, the August opening saw a bid-to-cover of 1.19x and a bid-to-offer of 0.79x after desks pointing to the potential for softer demand ahead of the auction, with the 7-year area falling between the demand sweet spots of 5-year and 10-year, making for fewer natural buyers in this area of the curve. The 0.79x bid-to-offer was the joint lowest seen in the German 7-year segment since August 2022.

- Domestically in Germany, Chancellor Merz headlined earlier today, saying his government will make concrete proposals for a pension system reform this year. While not a new theme, it is worth watching the evolution of the German pension system given the potential knock on impact for flows / holdings. On data, today's IFO Business Climate index saw some broad-based underperformance.

- The next German auction will be E5bln of the 10-year 2.60% Aug-35 Bund (ISIN: DE000BU2Z056) on October 1.

- Timing: Results will be available shortly after the bidding window closes at 10:30BST / 11:30CEST.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GERMAN DATA: A Sixth Consecutive Improvement For Ifo Business Climate

Aug-25 08:35

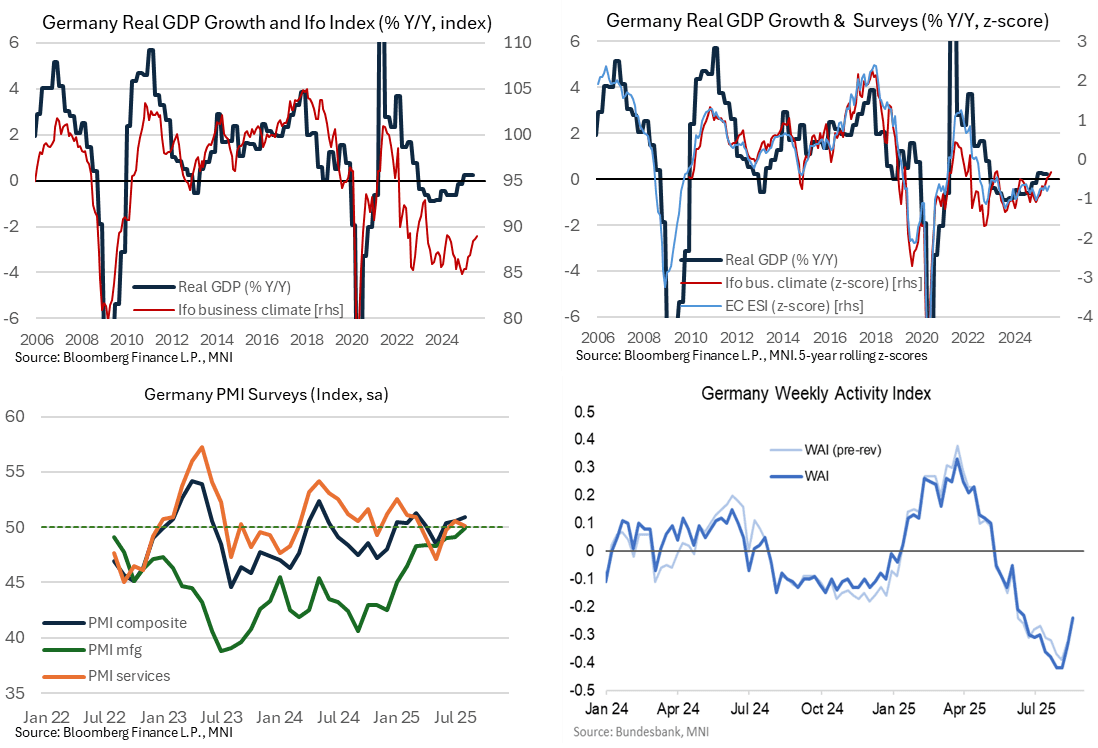

The Germany Ifo business climate index increased for a sixth consecutive month in August as it takes it to the high of its range for the past eighteen months, but it still suggests little material upside to tepid German real GDP growth despite this.

- The Ifo Business Climate index was close to expectations as it slightly improved in August to 89.0 (cons 88.8) from 88.6 in July.

- Whilst still subdued by historical standards, it’s nevertheless at its highest since Apr 2024 on the back of six consecutive monthly improvements.

- This trend improvement has come with increases in both the current assessment and more notably the expectations indexes. This expectations-led improvement continued this month, with the expectations index rising to 91.6 (cons 90.5) from 90.8 vs the current assessment edging a tenth lower to 86.4 (cons 86.7).

- A seeming post-pandemic structural break with the historical fit between the business climate index and real GDP growth complicates the readthrough to growth implications, although rolling z-scores have more recently been useful.

- Here, the Ifo business climate has started to look a little more optimistic than the European Commission’s Economic Sentiment Index (to July) but even then the Ifo series suggests little upside to still tepid German real GDP growth of 0.2% Y/Y as of Q2 (having averaged -0.4% since 1Q23).

MNI: GERMANY AUG IFO BUSINESS CLIMATE INDEX 89

Aug-25 08:00

- MNI: GERMANY AUG IFO BUSINESS CLIMATE INDEX 89

MNI EXCLUSIVE: China's equity market and economic impacts

Aug-25 07:54

- Advisors and analysts share their outlook on China's equity market and its economic impact.

- On MNI Policy MainWire now, for more details please contact sales@marketnews.com