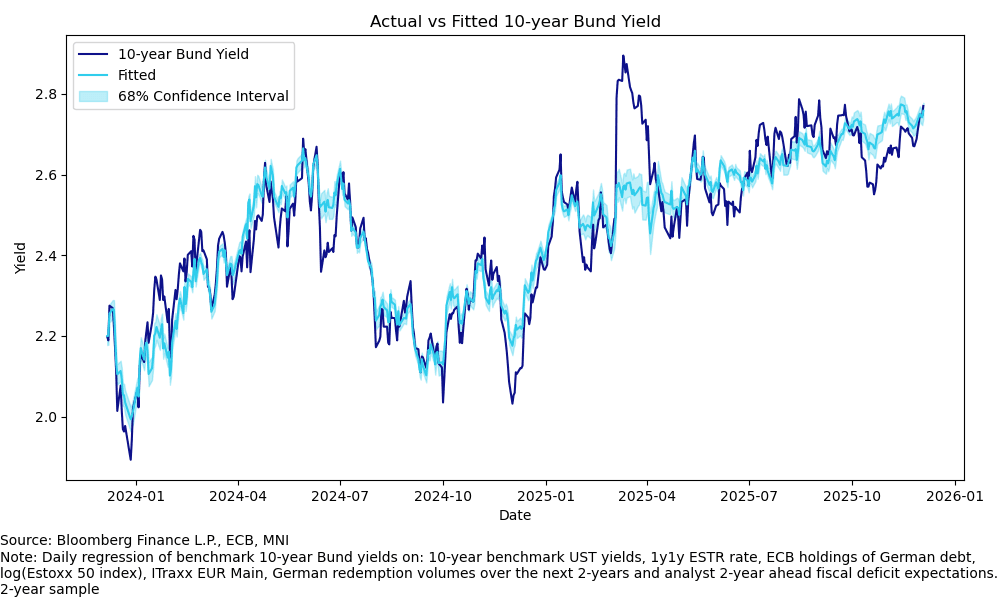

BUNDS: 10-year Yields Align With FV; Analysts Look For Further Upside In '26

As highlighted through the week, the bias for EGB yields has been to the upside, with 10-year Bunds piercing the Sep 25 high of 2.78% and eyeing the 2.80% figure next. Clearance of 2.80% would mark the highest yield level since Chancellor Merz's fiscal loosening announcement in March. Looking ahead, the bias amongst analysts is for further increases through 2026, driven by German fiscal expansion and associated supply increases, continued ECB balance sheet run-off and increasing considerations around the need for ECB rate hikes.

- The highest forecast submitted to Bloomberg (as of November 17) is for a 10-year Bund yield of 3.25% by Q4 2026. Meanwhile, the lowest projection we have seen is Morgan Stanley at 2.45%. That call is based on an assumption that the ECB will cut to 1.50% next year.

- In the near-term, focus will be on today’s German pension system vote, the German 2026 issuance plan (expected W/C 15 December, but no set date yet) and the ECB decision/updated projections on December 18.

- The ~10bp rise over the past week has seen Bund yields re-align with our linear fair value model, fitted to ECB expectations, UST yields, risk proxies and fiscal/supply expectations.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGB OPTIONS: Bund Call Spread

RXZ5 130.00/130.50cs, bought for 10 in 4.2k.

RIKSBANK: Observations From the MPU: Cautiously Optimistic On Labour Market

A few observations from the Riksbank's latest Monetary Policy Update, none of which drastically change the message from today's policy statement. Governor Thedeen will hold a press conference at 1000GMT/1100CET. EURSEK has moved to fresh session lows over the last 30 minutes, but aggregate moves remain containted and there's still no reaction in 2-year SEK swap rates. Link to MPU here

"The uncertainty about economic developments abroad is still high. The war in Ukraine and tensions in the Middle East are still contributing to the uncertainty. US trade policy is also contributing, as it can change unexpectedly once again"

- Unsurprising inclusions in the Riksbank's international risk assessment. However, it’s an interesting comparison with the ECB, which noted in October that positive developments in these risk factors were reasons to assume some downside growth risks have “abated”.

"Although the demand for labour is weak, some indicators point to the situation on the labour market being on the verge of a turnaround, in line with the Riksbank’s forecast. The number of newly-registered vacancies and companies’ recruitment plans have increased somewhat."

- We noted in our preview that lard labour market data (i.e. the LFS data) remains weak. However, we also highlighted that the Public Employment Service's data suggested early signs of a turnaround in conditions (slightly lower unemployment claims, slightly higher vacancies). Taken alongside a small uptick in the Economic Tendency Indicator’s expected employment series, it seems the Riksbank is taking an optimistic view on the labour market outlook (in line with its September MPR projections).

"The Riksbank assesses that the krona will continue to strengthen somewhat going forward and contribute to dampening inflation."

- The Riksbank has held this view throughout the year despite the krona outperforming the G10 basket YTD.

"Overall, it is not certain how much households will choose to consume when their incomes rise going forward, which could affect how much the fiscal policy stimulus boosts economic activity"..."There are now also signs that the lower interest rates are yielding a positive impact on household consumption, although it will take longer before monetary policy has its full impact"

- Highlights that there is still a little uncertainty around whether proposed 2026 fiscal measures will stimulate consumption. We noted in September that the seasonally adjusted household net saving rate rose to 16.2% in Q2, up from 14.9% in Q1 for the highest since Q2 2024 (and before that, Q1 2021).

- Even though disposable income growth is extending further into positive territory, and past Riksbank rate cuts have reduced the burden of interest payments, households remain cautious. The Board will hope that the recent recovery in consumer confidence will filter into lower savings rates in the coming months.

MNI: EUROZONE OCT FINAL SERV PMI 53.0 (52.6 FLASH, 51.3 SEP)

- MNI: EUROZONE OCT FINAL SERV PMI 53.0 (52.6 FLASH, 51.3 SEP)

- EUROZONE OCT FINAL COMPOSITE PMI 52.5 (52.2 FLASH, 51.2 SEP)