MNI US MARKETS ANALYSIS - Stocks Off Lows, Sentiment Soothed

Highlights:

- Equities off lows, pointing to higher open despite mixed-to-poor earnings this week

- No NFP due Friday as shutdown delays publication to next Wednesday - but Canada labor market data due

- Trump due to sign executive orders from 1500ET onwards

US TSYS: Latest Gains Pared But Corrective Nature Starts To Be Questioned

US desks filtering in find Treasuries bear flatter having pared a further push higher with the Asia open along with a flash crash in Bitcoin to $60k in moves that dragged equities lower. A recovery in precious metals and crypto will continue to be watched along with Amazon at the equity cash open after yesterday’s earnings. Calendar focus meanwhile is on the U.Mich consumer survey before Fed Vice Chair Jefferson on the economic outlook.

- Cash yields are 1.5-3.1bp higher, with increases led by 2s.

- 5s30s at 111.5bp (-0.9bp) vs an overnight high of 113.7bp at what was its steepest in nearly a month.

- TYH6 trades close to session lows of 112-04+ (+00+) after an overnight high of 112-16+, the latest resistance level having cleared 20- and 50-day EMAs. Cumulative volumes are high at 710k.

- The M/T trend condition is bearish - MA studies are in a bear-mode set-up - and this suggests that the latest recovery is likely a correction. However, an extension higher would undermine the bear theme and open 112-22 (Jan 7 high). For bears, a reversal lower would refocus attention on 111-09 (Jan 20 low and bear trigger).

- Data: U.Mich consumer survey Feb prelim (1000ET), Consumer credit Dec (1500ET)

- Fedspeak: Jefferson (1200ET) – see STIR bullet

- Politics: Trump signs Executive Orders (1500ET)

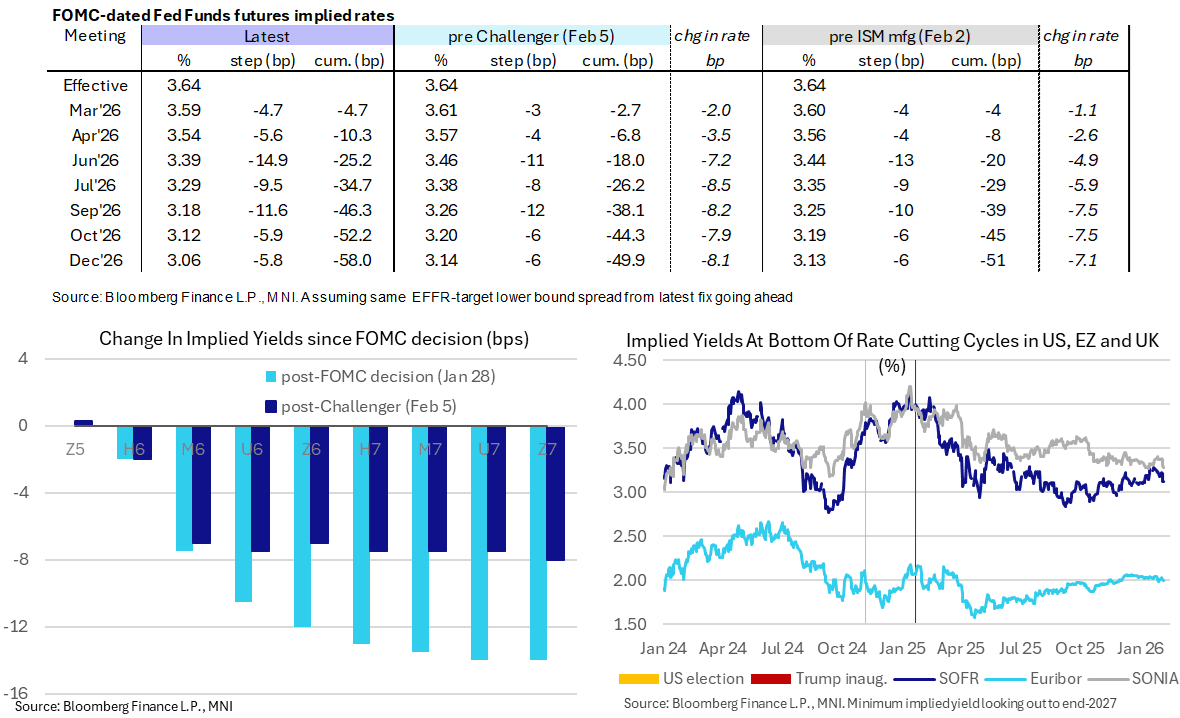

STIR: US Rates Still Reflecting Soft Labor Data, VC Jefferson On The Docket

- Fed Funds implied have lifted off yesterday’s lows (+3bp for 2H26 meetings), reversing the late additional move lower seen as the crypto sell-off extended, but still hold most of the dovish slide on weakness across four separate labor indicators and tech-led equity weakness.

- Cumulative cuts from 3.64% effective: 4.5bp Mar, 10.5bp Apr, 25bp Jun (vs 18bp pre-Challenger, the first of the releases), 34.5bp Jul, 46.5bp Sep (vs 38bp), 52bp Oct and 58bp Dec (vs 50bp).

- SOFR futures meanwhile are 2 ticks lower for the H6 but otherwise little changed on the day, although have also pulled back off highs.

- It holds yesterday’s 8.5bp slide in the terminal implied yield to 3.125% (Z6) to its lowest close since Jan 7.

- Today’s only scheduled Fedspeak is from Vice Chair Jefferson (voter) on the economic outlook and supply-side inflation dynamics at 1200ET (text + moderated Q&A). He tends not to speak publicly often although he did last make an appearance on Jan 16 arguing that policy is well positioned. He sees unemployment holding steady through 2026 whilst core goods prices are up but the tariff hit won’t be long lasting. We suspect he was one of four dots along with Chair Powell who pencilled in two cuts in 2026 (vs the median one) back at the December SEP.

- The latest on the DoJ-Powell subpoenas holding up the Warsh confirmation (Bloomberg link): “Senate Republicans, who have broadly applauded Trump’s nomination of Kevin Warsh to lead the Fed, increasingly view the probe as an unnecessary roadblock in a confirmation process that would otherwise be uneventful.”

ECB: BofA Go Against The Grain With 50bp Of Cuts In 2027 Base Case

BofA, with already one of the more dovish analyst views on the ECB, have gone a little further in that they look for rate cuts in 2027 at a time when some expect a serious consideration of hikes. We will be publishing a full summary of latest analyst views in due course, but for now our preview found that SocGen and TD Securities saw the earliest hikes (Dec 2026) whilst of those specifying rate hike views, most expect them to start in the middle to second half of 2027.

- Specifically, BofA have taken out the insurance cut they had long expected in Mar 2026 (which they had low conviction in ahead of yesterday’s meeting) and instead add two “proper” cuts of 25bp in Mar and Jun 2027.

- “To be clear, it wasn’t ECB communication that did the trick. It was uneventful, as expected. The message was one of data-dependence, no pre-commitment and a meeting-by-meeting approach”.

- “To be more precise, we hold three convictions on the ECB. First, hike are very unlikely absent a shock in the next two years. Second, the ECB is more likely to cut than not, given the asymmetry of risks we see on both growth and inflation. Third, an insurance cut to finalise the cutting cycle would have made sense now. But that window is closing. So when/if them move, we think they will need to move more than once.”

- “What really did it for us to make two cuts our base case for 1H27 was a reassessment of the growth outlook in Germany, in particular. […] We think fiscal-driven growth could be stronger in 2026 but weaker thereafter”. They see a flatter Euro area growth forecast with 1.2% in 2026 (+0.2pps), 1.3% in 2027 (-0.1pp) whilst core inflation moves to 1.7% in 2017.

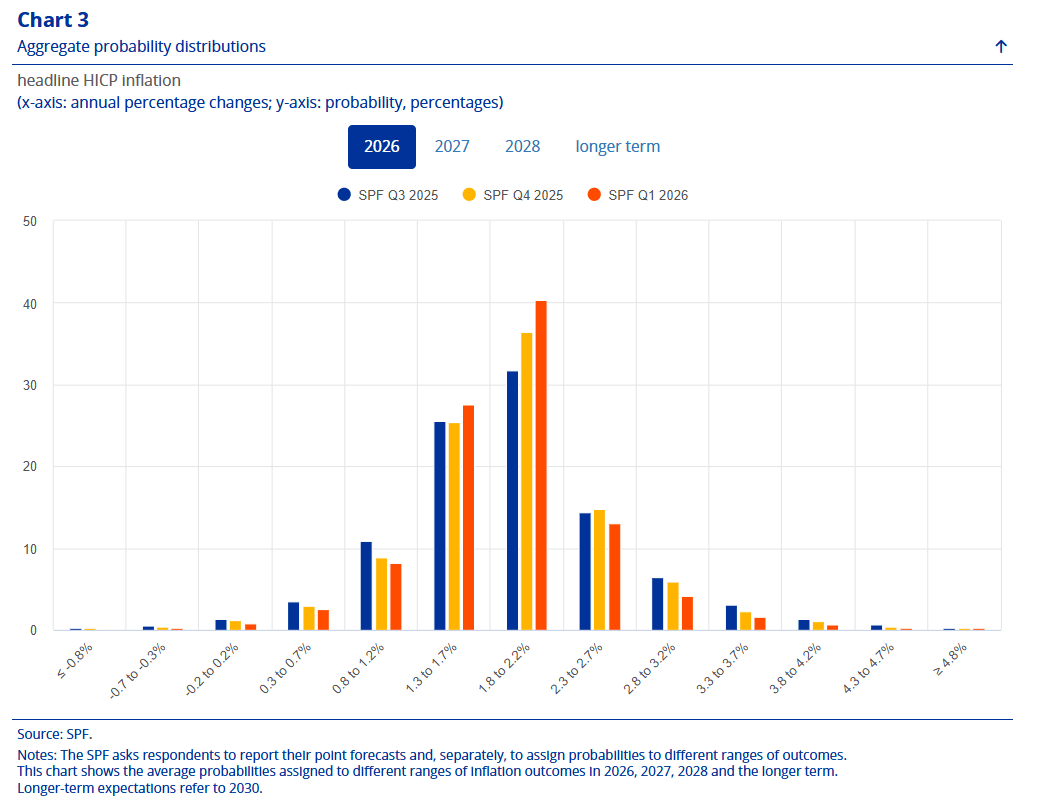

ECB: Q1 SPF Supports ECB Narrative Of "Good Place"

The ECB’s Q1 Survey of Professional Forecasters saw an immaterial revision to median expectations for GDP growth while inflation medians were unrevised. One potentially notable development was that the ECB no longer commented on tariff risks in the press release as it did in previous quarters. Overall, the survey shouldn’t have much impact on the median Governing Council member’s views. Full survey here

- HICP expectations were unchanged for 2026 (1.8%), 2027 (2.0%) while 2028 was added for the first time at 2.1%. There were also no revisions to median core HICP expectations for those years.

- GDP growth expectations for 2026 (1.2%) represent a 0.1pp upward revision, while 2027 stands unrevised (1.4%). For 2028, the survey sees a new 1.3% median.

- Looking at the charts of the survey shows uncertainty for 2026 HICP inflation expectedly decreasing amongst forecasters, with now 40.3% of the sample seeing the measure to average between 1.8% and 2.2% this year (36.4% back in Q4). Downside risks are seen as more prevalent for this year then upside risks, consistent with the ECB's view that headline inflation should edge somewhat below 2% this year. For 2027, 35.7% of forecasters think inflation will come in between 1.8% and 2.2%, meanwhile (36.0% back in Q4).

STIR/BASIS: Bar For ECB Move High, Steady EUR In X-ccy Despite Repo Line News

With various front end Euribor calendar spreads trading close to year-to-date lows we reaffirm our view that that the bar to a near-term ECB rate change is set relatively high, particularly in light of the steady tone in yesterday’s post-decision communique.

- In truth, the major point of discussion since the meeting has been centred on the impending reworking of the of the ECB’s repo line framework.

- The lines run between the ECB and non-systemic central banks in Europe to provide EUR liquidity when required (against EUR denominated HQLA collateral).

- RTRS sources noted that “the ECB is working on opening up access to euro liquidity to more countries, making it cheaper and easier to obtain as part of efforts to bolster the international role of the single currency. ECB President Christine Lagarde has long seen these liquidity lines as a key tool to boost the euro's global reach, particularly at a time when investors are reassessing the dollar's status due to the unpredictable nature of U.S. President Donald Trump's economic policy”.

- In terms of existing use, Commerzbank note that “the liquidity lines with other central banks have in the past mainly been used over year-end, by single digit billion € amounts”.

- In times gone by you may have expected such news/speculation to trigger some (at least marginal) cheapening of EUR vs. USD in x-ccy basis markets, but the ongoing questions surrounding the independence of U.S. institutions, current differentiation in net Fed & ECB liquidity management practices & U.S. trade policy provide structural headwinds for the USD, allowing EUR to trade at a premium to USD out to 5s in x-ccy (vs. the more normal/familiar EUR discount), making for no tangible movement in the market following the news.

US TSY FUTURES: Net Long Setting Dominated On Thursday

OI data points to long setting dominating as Tsy futures rallied on Thursday.

- Over $6mln DV01 of fresh net long exposure was added across the curve, with net short cover in UXY & WN providing some interruption to the wider theme.

- The biggest net positioning swing came in FV futures (~$5.6mln DV01).

- Soft labor market data and ongoing headwinds for U.S. tech names in equity trade drove demand for Tsys on the day.

| 05-Feb-26 | 04-Feb-26 | Daily OI Change | OI DV01 Equivalent Change ($) | |

| TU | 4,767,395 | 4,719,317 | +48,078 | +1,774,826 |

| FV | 6,919,123 | 6,788,168 | +130,955 | +5,618,003 |

| TY | 5,489,346 | 5,460,738 | +28,608 | +1,882,455 |

| UXY | 2,569,210 | 2,598,455 | -29,245 | -2,605,340 |

| US | 1,721,970 | 1,716,563 | +5,407 | +763,603 |

| WN | 2,181,586 | 2,187,420 | -5,834 | -1,068,226 |

| Total | +177,969 | +6,365,322 |

SOFR: Mix Of Short Cover & Long Setting On Thursday

OI data points to net short cover dominating through the reds as SOFR futures rallied on Thursday, before net long setting came to the fore further out the strip.

- Soft labor market data and ongoing headwinds for U.S. tech names in equity trade drove the dovish move.

| 05-Feb-26 | 04-Feb-26 | Daily OI Change |

| Daily OI Change In Packs |

SFRZ5 | 1,356,377 | 1,352,851 | +3,526 | Whites | -98,871 |

SFRH6 | 1,373,740 | 1,421,042 | -47,302 | Reds | -39,743 |

SFRM6 | 1,435,095 | 1,469,351 | -34,256 | Greens | +15,180 |

SFRU6 | 1,458,539 | 1,479,378 | -20,839 | Blues | +23,266 |

SFRZ6 | 1,411,656 | 1,432,529 | -20,873 |

|

|

SFRH7 | 1,040,903 | 1,046,487 | -5,584 |

|

|

SFRM7 | 887,883 | 892,828 | -4,945 |

|

|

SFRU7 | 838,801 | 847,142 | -8,341 |

|

|

SFRZ7 | 904,529 | 882,613 | +21,916 |

|

|

SFRH8 | 514,518 | 524,037 | -9,519 |

|

|

SFRM8 | 446,221 | 447,088 | -867 |

|

|

SFRU8 | 387,121 | 383,471 | +3,650 |

|

|

SFRZ8 | 380,190 | 373,411 | +6,779 |

|

|

SFRH9 | 217,032 | 220,308 | -3,276 |

|

|

SFRM9 | 228,622 | 212,898 | +15,724 |

|

|

SFRU9 | 178,480 | 174,441 | +4,039 |

|

|

EUROPE ISSUANCE UPDATE

GILT AUCTION PREVIEW: On offer at tender next week

- The DMO has announced that it will sell GBP300mln of the 4.25% Dec-49 Gilt (ISIN: GB00B39R3707) via tender on Wednesday 11 February.

- This will be the first time this gilt has been reopened since 2010.

FOREX: AUD and NZD Outperforming Amid Risk Stabilisation

- Weakness in the equity/crypto space late Thursday added to the recent turbulence for precious metals, resulting in a brief spike higher for the dollar in early APAC trade Friday. EURUSD saw fresh pullback lows of 1.1766 overnight but has recovered back to 1.18 since, as risk sentiment has somewhat stabilised and the broader theme of the USD recovery consolidates.

- This also resulted in overnight lows of 0.6897 for AUDUSD which was followed by a notable bounce back to 0.6975, which explains the relative AUD strength on Friday. The most recent pullback from last week’s 0.7094 cycle highs in AUDUSD has been allowing the recent overbought trend condition to unwind. A break of the 20-day EMA intersecting at 0.6880 would be a bearish short-term development, while the overall bullish theme remains intact.

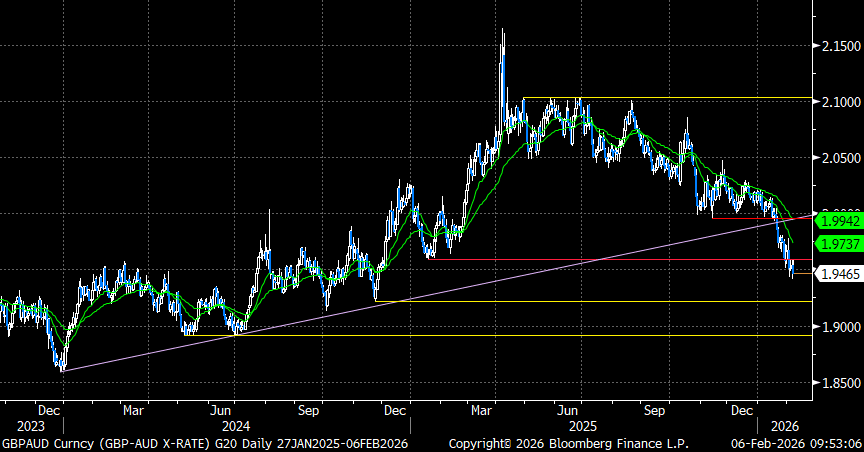

- Idiosyncratic drivers in the UK also weighed heavily on the pound Thursday, allowing GBPAUD to consolidate its notable 3.5% downswing in 2026.

- 156.50 has been capping short-term declines for USDJPY, which is now consolidating around the 157.00 mark as we approach this weekend’s Japanese election. There is sizeable demand for options looking for gains north of the year's highs and re-entering territory at which markets have speculated the MoF could intervene. These are consistent with scepticism around PM Takaichi's "responsible" fiscal policy. It remains to be seen in which directions her plans tilt after the election, which polls suggest will result in Takaichi’s LDP party securing a majority.

- Canadian employment data highlights Friday’s calendar, before preliminary reads of UMich sentiment and inflation expectations. Fed’s Jefferson will speak on the economic outlook.

FOREX: GBPAUD Consolidates Below 2025 Lows, Down 3.5% This Year

- Weakness in the equity/crypto space on Thursday has added to the recent turbulence for precious metals, all combining to dampen the most recent enthusiasm for the Australian dollar, which was among the worst performing currencies in G10 yesterday.

- Despite this, idiosyncratic drivers in the UK have also weighed heavily on the pound, allowing GBPAUD to consolidate its notable 3.5% downswing in 2026. Downside momentum gathered pace on a break of 1.9959 in mid-Jan and was assisted by a break of trendline support, drawn from the Dec 2023 lows. Price has been able to consolidate below the 1.96 (2025 lows) this week, keeping bearish sentiment firmly intact for the cross.

- Downside targets for the move are located at 1.9218 and 1.8918.

- Deutsche Bank remain bullish on AUD, stating it still looks cheap vs relative rates on a short-term chart, and even more so on longer-term charts. They also note the return to high-yielder status could encourage more debt inflows, and think it’s noteworthy that AUD looks cheap vs commodity prices.

- The preliminary reading of Q4 GDP highlights the UK calendar next week, as well as the REC labour report, while speculation surrounding the political sphere will undoubtedly continue to drive short-term GBP sentiment. There are no tier-one releases in Australia, with household spending, consumer and business confidence readings all scheduled.

OPTIONS: Expiries for Feb06 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1800(E3.7bln), $1.2000(E3.3bln)

- USD/JPY: Y156.00($942mln), Y157.00($809mln)

- AUD/USD: $0.6875-90(A$2.1bln)

EQUITIES: Medium-Term Trend Condition in EuroStoxx 50 Futures Remains Bullish

- The medium-term trend condition in Eurostoxx 50 futures remains bullish and for now, the latest pullback appears corrective. Key support lies at the 50-day EMA at 5870.81. It has been pierced, a clear break of this average would undermine the bull theme and signal scope for a deeper retracement. The bull trigger at 6072.00, the Jan 14 / 15 high, has been pierced. A move through this hurdle would resume the primary uptrend.

- A short-term bearish theme in S&P E-Minis has resulted in a break of 6814.50, the Jan 21 low and a recent bear trigger. Note too that the contract is trading below both the 20- and 50-day EMAs. This highlights a stronger short-term reversal and signals scope for a deeper retracement. A continuation lower would open 6691.56, a Fibonacci retracement point. Initial firm resistance is seen at 6917.97, the 50-day EMA.

COMMODITIES: Key Resistance and Bull Trigger for WTI at $66.48, the Jan 30 High

- A bull cycle in WTI futures remains intact. However, the reversal from the Jan 29 high continues to highlight a corrective cycle. Attention is on support at the 20-day EMA, at $61.76. The 50-day EMA lies at $60.21. A clear breach of the 50-day average would highlight a stronger reversal and open $58.53, the Jan 20 low. Key resistance and the bull trigger has been defined at $66.48, the Jan 30 high.

- The latest bounce in Gold highlights a retracement of the Jan 29 - Feb 2 sell-off. The next two resistance points to monitor are $5139.9 and $5314.0, Fibonacci retracement levels. Note that the sharp sell-off from the Jan 29 high highlights a potential top in the L/T trend and from a S/T perspective, an unwinding of the recent extreme overbought condition. A resumption of bearish activity would refocus attention on $4403.0, the Feb 2 low.

| Date | GMT/Local | Impact | Country | Event |

| 06/02/2026 | 1200/1200 | BOE Market Participants Survey | ||

| 06/02/2026 | 1215/1215 | BOE Pill at National MPC Agency Briefing | ||

| 06/02/2026 | - | BOE MPG Agenda Published | ||

| 06/02/2026 | 1330/0830 | *** | Labour Force Survey | |

| 06/02/2026 | 1500/1000 | * | Ivey PMI | |

| 06/02/2026 | 1500/1000 | *** | U. Mich. Survey of Consumers | |

| 06/02/2026 | 1500/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 06/02/2026 | 1700/1200 | Fed Vice Chair Philip Jefferson | ||

| 06/02/2026 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 06/02/2026 | 2000/1500 | * | Consumer Credit |