ECB: Q1 SPF Supports ECB Narrative Of "Good Place"

Feb-06 09:30

The ECB’s Q1 Survey of Professional Forecasters saw an immaterial revision to median expectations for GDP growth while inflation medians were unrevised. One potentially notable development was that the ECB no longer commented on tariff risks in the press release as it did in previous quarters. Overall, the survey shouldn’t have much impact on the median Governing Council member’s views. Full survey here

- HICP expectations were unchanged for 2026 (1.8%), 2027 (2.0%) while 2028 was added for the first time at 2.1%. There were also no revisions to median core HICP expectations for those years.

- GDP growth expectations for 2026 (1.2%) represent a 0.1pp upward revision, while 2027 stands unrevised (1.4%). For 2028, the survey sees a new 1.3% median.

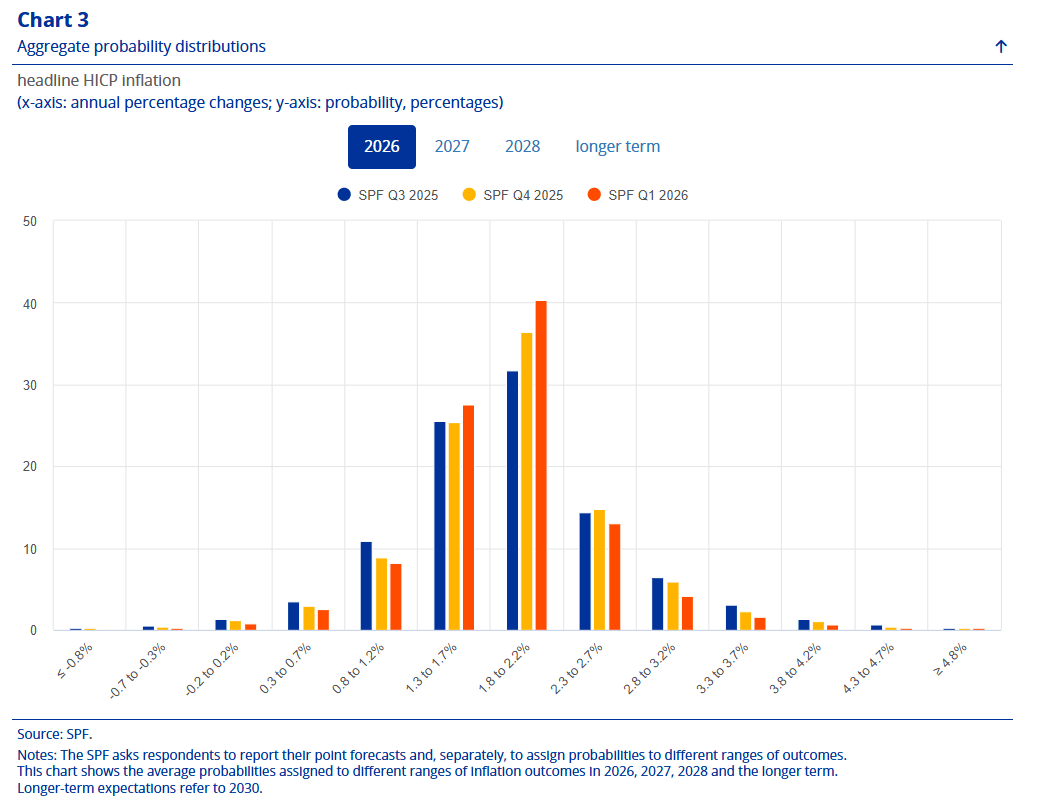

- Looking at the charts of the survey shows uncertainty for 2026 HICP inflation expectedly decreasing amongst forecasters, with now 40.3% of the sample seeing the measure to average between 1.8% and 2.2% this year (36.4% back in Q4). Downside risks are seen as more prevalent for this year then upside risks, consistent with the ECB's view that headline inflation should edge somewhat below 2% this year. For 2027, 35.7% of forecasters think inflation will come in between 1.8% and 2.2%, meanwhile (36.0% back in Q4).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: UK DEC CONSTRUCTION PMI 40.1 (42.3 EXP, 39.4 NOV)

Jan-07 09:30

- MNI: UK DEC CONSTRUCTION PMI 40.1 (42.3 EXP, 39.4 NOV)

OPTIONS: Expiries for Jan07 NY cut 1000ET (Source DTCC)

Jan-07 09:27

- EUR/USD: $1.1725(E685mln), $1.1775(E1.4bln)

- USD/JPY: Y156.00($677mln), Y157.00($903mln)

- NZD/USD: $0.5650(N$1.1bln)

- USD/CAD: C$1.3800($1.3bln), C$1.3835($852mln)

EGBS: Sell-Side Expect Spreads To Hold Tight In '26

Jan-07 09:24

EGB spreads to Bunds are little changed to start ’26, with peripheral spreads holding at the lower end of historical ranges, while OATs continue to embed some political and fiscal risk, owing to well-documented issues in France.

- Goldman Sachs point to a continuation of tight spreads in 2026, suggesting that the “sovereign risk factor will remain benign”.

- They forecast BTP/Bunds at 75bp, OAT/Bunds at 70bp and SPGB/Bunds at 55bp come end ’26. For OATs they suggest that “markets have adjusted to chronic, rather than acute, political uncertainty. With the risk of early elections having receded, we think widening risk is contained and expect the idiosyncratic premium in OATs to diminish further once markets get clarity on the 2026 deficit bottom-line, likely in Q1”.

- Elsewhere, Societe Generale note that they “do not expect the EGB tightening trend to reverse in the coming months. While a sharp tightening appears unlikely after last year’s strong performance, if supply is well absorbed and investors continue to seek carry, spreads could narrow slightly”.

- For OATs they write “government stability matters more than the precise deficit target. A government collapse - whether this month or later in H1 - could trigger volatility, with 80bp vs. Bunds within reach. An earlier fall would weigh more heavily on spreads, as the risk of legislative elections, albeit low, would remain, whereas a later fall would carry little such risk given proximity to the 2027 presidential elections. If negotiations drag on for weeks or months without toppling the government, we expect the 10y OAT/Bund spread to hover around 65-70bp, breaking below 65bp only if broader EGB spreads tighten and BTP/Bunds moves under 60bp”.

Related bullets

Related by topic

EUR/USD

Bunds

Germany

Euribor

European Central Bank