US TSYS: Latest Gains Pared But Corrective Nature Starts To Be Questioned

US desks filtering in find Treasuries bear flatter having pared a further push higher with the Asia open along with a flash crash in Bitcoin to $60k in moves that dragged equities lower. A recovery in precious metals and crypto will continue to be watched along with Amazon at the equity cash open after yesterday’s earnings. Calendar focus meanwhile is on the U.Mich consumer survey before Fed Vice Chair Jefferson on the economic outlook.

- Cash yields are 1.5-3.1bp higher, with increases led by 2s.

- 5s30s at 111.5bp (-0.9bp) vs an overnight high of 113.7bp at what was its steepest in nearly a month.

- TYH6 trades close to session lows of 112-04+ (+00+) after an overnight high of 112-16+, the latest resistance level having cleared 20- and 50-day EMAs. Cumulative volumes are high at 710k.

- The M/T trend condition is bearish - MA studies are in a bear-mode set-up - and this suggests that the latest recovery is likely a correction. However, an extension higher would undermine the bear theme and open 112-22 (Jan 7 high). For bears, a reversal lower would refocus attention on 111-09 (Jan 20 low and bear trigger).

- Data: U.Mich consumer survey Feb prelim (1000ET), Consumer credit Dec (1500ET)

- Fedspeak: Jefferson (1200ET) – see STIR bullet

- Politics: Trump signs Executive Orders (1500ET)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

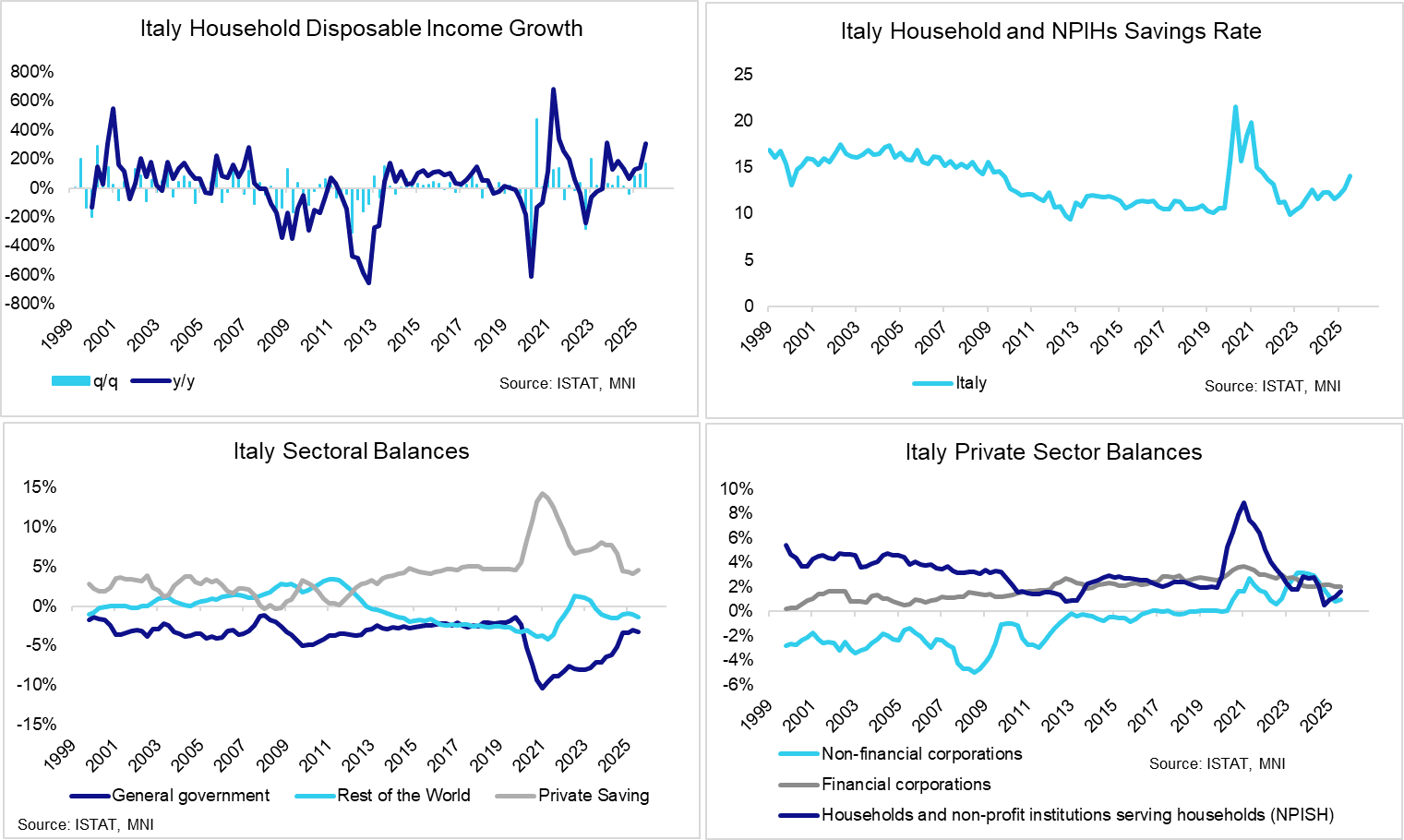

ITALY DATA: Households Are Saving - Not Consuming - Disp Income Rises

Italian households have been hesitant in channelling increases in disposable income to consumption. The Government will hope that a tax cut to middle-income earners in the 2026 budget will help spur additional household spending in 2026, supporting a cyclical economic recovery. Bloomberg consensus currently sees annual Italian consumption growth at 0.9% in 2026, up from a projected 0.8% in 2025.

- Italian disposable income growth was 1.7% Q/Q in Q3, corresponding to a 3.1% Y/Y rate (vs 1.4% in Q2). However, the savings rate rose to 14.1%, up from 12.7% in Q2 for a four year high.

- Italian sectoral balances have been broadly stable since the start of 2025. Government fiscal consolidation post-covid - which was delayed by the (fiscally) expensive Superbonus scheme - has mostly been reflected in declining private sector (primarily household) savings balances. However, the current account has also moved back into surplus (i.e. foreign saving has declined) since 2023.

OUTLOOK: Price Signal Summary - Bear Threat In Oil Futures Remains Present

- On the commodity front, the trend structure in Gold is bullish and a sharp sell-off late December appears corrective - for now. The trend is overbought and a deeper retracement would allow this condition to unwind. First support at $4351.9, the 20-day EMA, has been pierced. A clear break of the average would expose the 50-day EMA at $4215.8. For bulls, a resumption of gains would open $4578.3, a 1.618 projection of the Oct 28 - Nov 13 - Nov 18 swing.

- The trend theme in WTI futures is unchanged, it remains bearish and recent gains appear to have been corrective. Moving average studies are in a bear-mode position, highlighting a dominant downtrend. A resumption of the bear leg would signal scope for a move towards $53.77, a 1.764 projection of the Jul 30 - Aug 13 - Sep 26 price swing. First resistance is at $58.41, the 50- day EMA.

US TSYS: TYH6 Close To Resistance With ADP, ISM Services and JOLTS Ahead

Treasuries have firmed overnight, mainly in London hours, in a further reversal off yesterday’s lows with assistance from soft European data. The WSJ reported that Secretary of State Rubio told lawmakers that recent administration threats against Greenland didn’t signal an imminent invasion and that the goal is to buy the island from Denmark.

- Cash yields are 0.5-4.2bp lower on the day, with declines led by the long-end.

- 30Y yields trade at 4.823% for a sizeable pullback after briefly testing the 4.88% level three times yesterday.

- TYH6 trades close to session and week highs of 112-18 (+07) on reasonable cumulative volumes of 325k.

- It comes close to resistance at 112-19+ (50-day EMA) after which lies 112-25+ (Dec 30/31 high) as it shifts away from support at 112-01+ (Dec 23 low) and 111-29 (Dec 10 low, bear trigger).

- Data: MBA mortgage applications (0700ET), Monthly ADP Dec (0815ET), Chicago Fed CARTS (0830ET), ISM services Dec (1000ET), JOLTS Nov (1000ET), Factory orders Oct (1000ET),

- Fedspeak: Bowman on banking supervision (1610ET, text + Q&A)

- Bill issuance: US Tsy $69B 17W bill auction (1130ET)

- Politics: Press briefing by WH Press Sec Leavitt and other cabinet officials (1100ET), Trump signs Executive Orders (1430ET)