JGB TECHS: (Z5) Bounce Fades

- RES 3: 140.08 High Jun 13

- RES 2: 139.05 High Aug 4

- RES 1: 137.30 - High Sep 8 and key short-term resistance

- PRICE: 136.23 @ 14:21 BST Oct 22

- SUP 1: 135.61 - Low Oct 08

- SUP 2: 135.39 - 1.618 proj of the Aug 4 - Sep 2 - Sep 8 swing (cont.)

- SUP 3: 134.69 - 2.000 proj of the Aug 4 - Sep 2 - Sep 8 swing (cont.)

Prices surged last week, in sympathy with global bond markets, helping the price rally to a high of 136.64. This rally proved short-lived, however, as domestic fiscal concerns continue to weigh on prices. This affirms the firm downtrend that’s dominated prices since mid-September, and prices will need to challenge resistance before signaling any broader reversal. Key short-term resistance has been defined at 137.30, the Sep 8 high. The latest sell-off, however, resulted in a break of support at 136.19, the Sep 4 low and a bear trigger. Clearance of this level confirms a resumption of the downtrend and opens 135.39 next, a Fibonacci projection.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA: Government Bond Issuance Today

- Hong Kong to Sell HK$64.37 Billion 91-Day Bills

- Hong Kong to Sell HK$15 Billion 182-Day Bills

- Hong Kong to Sell HK$5 Billion 364-Day Bills

- Bank of Thailand to Sell THB 65bn of 91-Days Bills

- Bank Indonesia to Sell 32D SVBI Bills

- Bank Indonesia to Sell 181D SVBI Bills

- Bank Indonesia to Sell 95D SVBI Bills

- Bank Indonesia to Sell 273D SVBI Bills

- Bank Indonesia to Sell 365D SVBI Bills

- Philippines To Sell PHP 25.0Bln 2044 Bonds (PH0000058786**)

- Philippines To Sell PHP 10.0Bln 2028 Bonds (PIBD0728D649*)

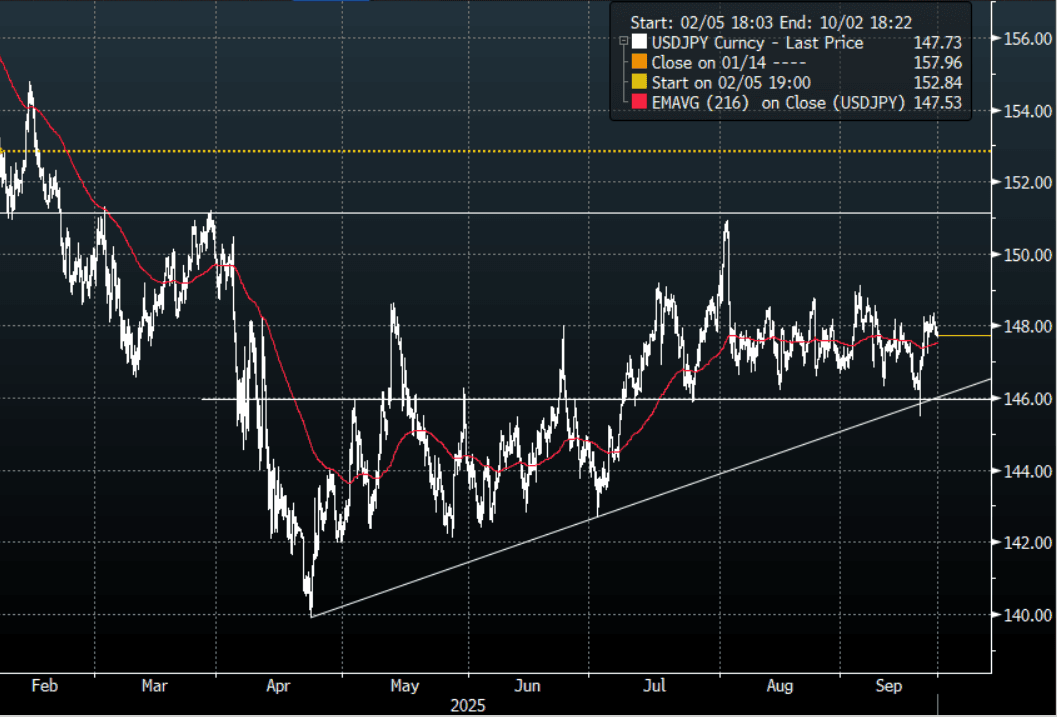

JPY: USD/JPY - Move Stalls Above 148.00, Back To The Middle Of The Range

The overnight range was 147.66 - 148.26, Asia is currently trading around 147.70. USD/JPY stalled above 148.00 and continues to chop around sideways without really going anywhere. The USD retracement stalled though as sellers reemerged even with some clearly hawkish rhetoric from Fed speakers overnight. The price is still in the middle of its recent 146-149 range, and we need a convincing break on either side to see some clearer direction again. Neither the FOMC nor the BOJ were able to provide any clarity, the market will start turning its focus towards payrolls which seems a lifetime away.

- Bloomberg - “Deutsche Bank Says Dollar to Extend Drop Against Yen This Year. George Saravelos, head of FX research anticipates more weakness for the dollar, predicting that it will fall below 140 yen by year-end. Says the need to address inflation in Japan is growing. BOJ rate hikes at a time when the Fed is cutting should support the yen, he says. “Starting from a very undervalued position, the yen has a long runway provided the political pieces fall into place following the upcoming LDP election”

- “Musalem, Bostic, and Hammack were leaning on the more hawkish side,” said Macquarie’s Thierry Wizman. “I am surprised that the USD is weakening and stocks are rising. It seems as if no one really believes the Fed or Powell when they admonish the market for thinking that there are 4-5 more rate cuts on the way” - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 145.00($856m), 145.50($750m), 146.00($476m). Upcoming Close Strikes : 145.00($1.52b Sept 24), 152.00($1.67b Sept 26) - BBG.

- CFTC data shows last week asset managers reduced their JPY longs slightly +71162( Last +87239), leveraged funds again used the dip to add their short position believing the support will continue to hold -58811(Last -49951).

Fig 1 : USD/JPY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA: Coming Up in Asia Today

| 0430GMT | 1130HKT | 1330AEDT | Thailand Car Sales AUGUST |

| 0500GMT | 1200HKT | 1400AEDT | Malaysia CPI YoY AUGUST |

| 0600GMT | 1300HKT | 1500AEDT | HSBC India PMI Composite |

| 0600GMT | 1300HKT | 1500AEDT | HSBC India PMI Mfg |

| 0600GMT | 1300HKT | 1500AEDT | HSBC India PMI Services |

| 0600GMT | 1300HKT | 1500AEDT | Singapore CPI YoY AUGUST |

| 0600GMT | 1300HKT | 1500AEDT | Singapore CPI NSA MoM AUGUST |

| 0600GMT | 1300HKT | 1500AEDT | Singapore CPI Core YoY AUGUST |

| 0800GMT | 1500HKT | 1700AEDT | Malaysia Foreign Reserves |

| 0900GMT | 1600HKT | 1800AEDT | Taiwan Export Orders YoY AUGUST |

source: Bloomberg Finance LP / MNI