JGBS: Yield Rise Tapered After 40Y Auction, BOJ Noguchi Speech Tomorrow

JGB futures are slightly weaker, -3 compared to settlement levels, but well off lows.

- The Japan Oct Services PPI rose 2.7%y/y, in line with the consensus forecast. This was a step down from the Sep pace of 3.1% (which was revised up from the originally reported 3.0%). Note, we get the Tokyo Nov CPI outcome on Friday.

- BoJ May Hike In December - Per Reuters: "BOJ MESSAGING PREPARING MARKETS FOR POSSIBLE INTEREST RATE HIKE AS SOON AS DECEMBER WITH TWEAK TO COMMUNICATION, SOURCES SAY EXCLUSIVE - BOJ DECISION ON WHETHER TO HIKE IN DECEMBER OR HOLD OFF UNTIL JANUARY REMAINS A CLOSE CALL, ONE OF THE SOURCES SAYS".

- Cash US tsys are ~1bp cheaper in today's Asia-Pac session.

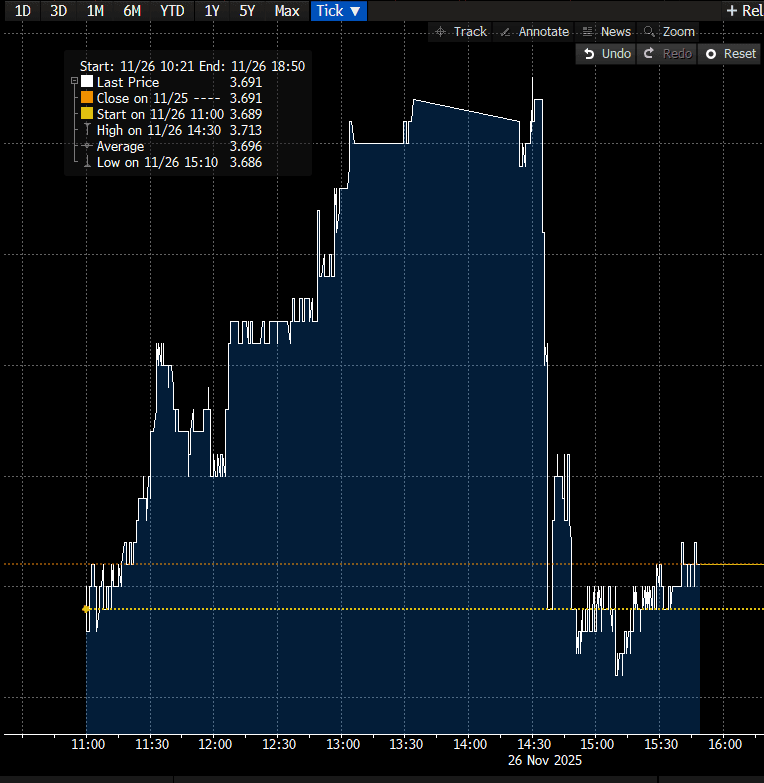

- Cash JGBs are little changed across benchmarks after today's 40-year auction. Demand for today’s 40-year bond issuance was solid, with the high yield coming in below dealer expectations. The auction’s cover ratio held relatively steady at 2.5851x versus 2.60x at the previous issuance. In afternoon trading, the 40-year bond pricing is 2bps richer than pre-auction levels. (see chart)

- Swap rates are 1bp higher.

- Tomorrow, the local calendar will be empty apart from a speech by BOJ Board Member Noguchi in Ohita.

Source: Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OIL: Oil Prices Give Up Early Gains As Excess Supply Key Concern

Oil prices rallied at the start of Monday’s APAC trading as the market was relieved by news that a draft US-China trade deal had been reached which would avoid 100% US tariffs on November 1. Increased protectionism is a negative for energy demand. However, crude has given up most of the early gains as excess supply worries pressure markets again.

- On the one hand new US/EU sanctions may weigh on Russian exports, but on the other hand OPEC could continue to increase its output target.

- WTI is 0.4% higher at $61.74/bbl off the intraday low of $61.49 and above initial support at $55.96. It reached $62.17 earlier, remaining below initial resistance at $62.34. The USD index is flat.

- Brent is up 0.2% to $66.06/bbl after falling to $65.95 but well above support at $60.17. It rose to $66.64 at the start of trading, just above resistance at $66.58 but the break wasn’t held.

- The focus this week is on Wednesday’s Fed decision. The USD OIS market has a 25bp cut priced in with another one at the 10 December meeting.

- Later October Dallas Fed manufacturing and October German Ifo survey are released. The ECB’s Elderson and Tuominen speak.

ASIA STOCKS: NIKKEI and KOSPI Hit New Highs as JCI Breaks Below Key Technicals

Japan's NIKKEI traded above 50,000 and the KOSPI through 4,000 as US - China tensions appear to be easing. The discussions between US and China ahead of the leaders meeting this week has seen some positive outcomes with an initial consensus reached on various bilateral issues including agriculture, according to a statement from the Chinese Ministry of Commerce. Chinese officials said the two sides reached a preliminary consensus on further topics including export controls, fentanyl and shipping levies, while US Treasury Secretary Scott Bessent said Trump's threat of 100% tariffs on Chinese goods "is effectively off the table". This comes ahead of the Thursday meeting with US President Trump and China President Xi in South Korea, on the sidelines of APEC summit. The weekend talks are expected to pave the way for a deal/agreement at the Thursday meeting between the two leaders and Trump expressed confidence in such an outcome. Tech stocks like Samsung in Korea surged by almost 2.9% and Taiwan's TSMC +2.7% whilst some regional defense and ship builders saw gains.

- The NIKKEI hit 2025 lows in April of 31,136 as the trade war kicked off in earnest, yet since then has rallied over 60% to 50,340.

- The KOSPI over that same period is up 75% with the added kicker of tax reform on dividends.

- China's major bourses are up only modestly today with the Hang Seng +1.05%, CSI 300 +1.05%, Shanghai Comp +1.1% and Shenzhen +0.95%. The major China bourses have appeared less correlated to tariff headlines of late as the ongoing surge in new retail equity accounts underpins strong fundamental demand for stocks, amidst growing belief in the economy.

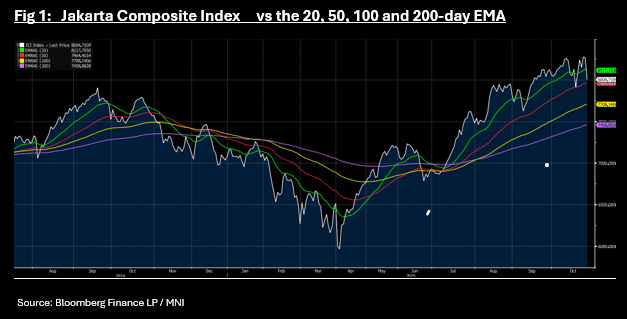

- The outlier today is the Jakarta Composite which is down -3.2% for its biggest one day fall since early September, breaking below the 20-day EMA of 8,117 and below 8,000. At 7,993 is is near to the 50-day EMA of 7,963 which it last traded below in July.

- The NIFTY 50 is up +0.55% in morning trade hitting a new all time high of 25,935.

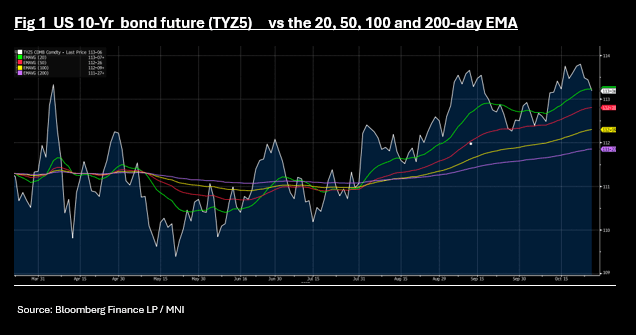

US TSYS: 10-Yr Bond Future Breaks Below Key Technical

The morning's sell off moderated into the afternoon, but the damage was done with bond futures all lower. TYZ5 is down -08 at 113-05+, breaking below the 20-day EMA of 113-07+

Cash bonds remain weak with yields across the curve 2-3bps higher.

- The US 2-Yr is at 3.51% (+2.5bps today)

- The US 5-Yr is at 3.63% (+3bps today)

- The 10-Yr is at 4.03% (+3bps today)

- The 30-Yr is at 4.62% (+3bps) today.

Tonight sees multiple bill issuance, 2-Yr notes, 5-Yr notes as the key auctions for markets.

Key focus for data tonight is Durable Goods, Dallas Fed Mfg, and Capital Goods orders.