CANADA DATA: Volatile Retail Sales Won't Stop BOC Worrying About Consumption

Sep-19 13:19

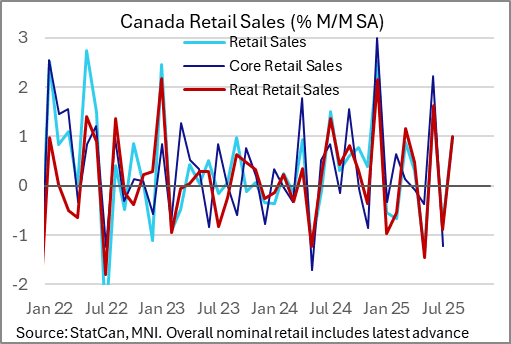

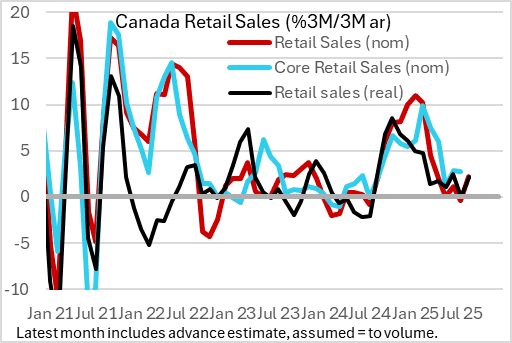

Retail sales growth was weak in July as expected, particularly in core terms, but August's advance reading suggests a solid enough rebound - continuing the volatility in this series. The August reading, if borne out, suggests a slow but relatively steady rate of consumption in Q3 which probably won't be a major mover for the Bank of Canada after this week's 25bp rate cut.

- Sales matched StatCan's flash estimate in July, contracting 0.8% M/M - with a small upward revision to June to 1.6% (1.5% prelim). Ex-auto sales however fared far worse, contracting 1.2% (consensus was -0.6%), albeit offset by a 0.3pp upgrade to 2.2% in June.

- This translated into a 0.8% M/M decrease in volume terms, and came on poor sales across the board (sales fell in 8 of 9 subsectors). Sales were particularly hit by supermarket sales reversing (-2.5% in Jul after +2.6% in Jun). and weak clothing retail (-2.9%), though as implied but the broader aggregates, motor vehicle and parts dealer sales rose (0.2%) albeit gas sales fell 0.9% (though this reflected lower prices, as volumes rose 0.2%).

- Attention as usual was on the advance indicator, which showed that August sales rose 1.0% M/M. That makes a material difference to overall sales momentum, with 3M/3M annualized sales potentially picking up from -0.4% in July (weakest in a year) in nominal terms to 2.2% (5-month high), and from 0.0% (also weakest in a year) to 2.1% in volume terms.

- The BOC described Q2 consumption as growing at a "healthy pace" (the July MPR expected "Consumption growth remains modest in the second half of 2025") but Gov Macklem's opening statement said "in the months ahead, low population growth and weakness in the labour market will likely weigh on household spending."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EUR: EUR/USD Boosted on Cook Headlines, EUR/GBP Strength

Aug-20 13:10

- EUR/USD holding the day's gains headed in to the Wall Street opening bell, buoyed by both the modestly softer USD on the call from Trump for Fed's Cook to resign, as well as firm EUR/GBP buying in recent trade, which tips the cross comfortably through 0.8648 highs to print the best levels of the week.

- EUR/GBP has shrugged off the higher-than-expected UK inflation print to rally near 50 pips off the post-data low to mirror the market view higher services CPI today may have only minimal feed-through to the BoE's decision-making process for the rest of this year.

- As a result, EUR/GBP is following the 50-dma higher, which should remain strong support at the close of 0.8626.

SOFR OPTIONS: Mixed Sep'25 SOFR Trade

Aug-20 13:08

- -20,000 SFRU5 95.81/SFRZ5 95.87 put spds, 0.75 net/Sep over

- +4,000 SFRU5 95.62/96.31 call over risk reversals, 0.25 ref 95.9025

CROSS ASSET: Lower Yields are helping some USD Downside

Aug-20 13:06

- A new session high for US Tnotes, now testing Yesterday's high of 111.27, just ahead of the small initial resistance at 111.30+.

- Outright Order flows are still fairly subdued, with all the volumes going through in Desks rolling their September Position into the December Expiry.

- Nonetheless and since Trump's post on Fed Cook, the USD is now on the backfoot, DXY tests session low, and EUR, CHF, and Gold are all testing their respective new intraday high.