CANADA DATA: Vacancies Continue To Mount Amid Broader Labour Loosening (2/2)

Even so, the August SEPH release overall showed growing labour market slack.

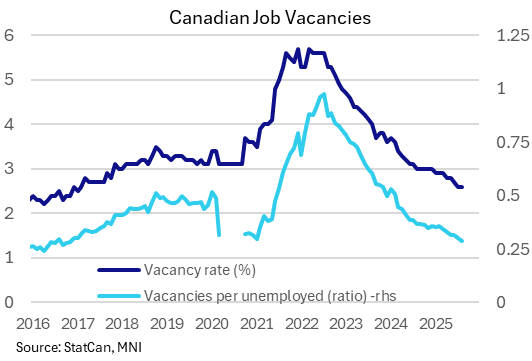

- Firstly, job vacancy data were weak, with openings falling 2.4% to 457.4k - the lowest since August 2017.

- Only one sector saw a rise in gains (agriculture, forestry, fishing and hunting); there's been a notable likely trade-conflict related fall in transportation and warehousing in which vacancies were at the lowest since May 2017.

- Notably the BOC's statement eyed "Job losses continue to build in trade-sensitive sectors and hiring has been weak across the economy."

- The ratios were even weaker, reflecting a rise in unemployed. Vacancies per unemployed Canadian fell to the lowest on an unrounded basis since 2016. In July 2022 there was nearly one job (0.98) per unemployed person; that ratio has now fallen below 0.29.

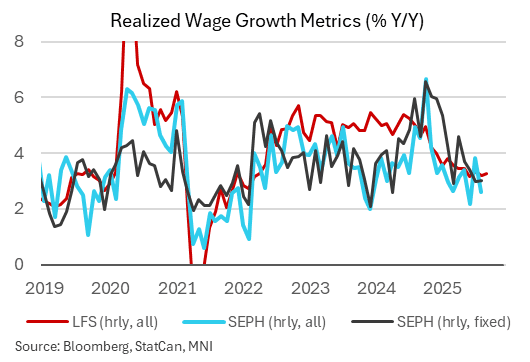

- Meanwhile, earnings and worked hours readings were on the soft side. Average weekly earnings were up 3.0% Y/Y after 3.2%, though flat M/M; average weekly hours worked were little changed by down 0.6% Y/Y. These are still some of the weakest figures seen over the last 3 years.

- Generally, all of these metrics continue to echo the broader theme of gradual labor market loosening.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Late SOFR/Treasury Option Roundup: Better Calls, Rate Cut Pricing Rises

SOFR/Treasury options revolved around low delta calls Tuesday, in addition to some chunky vol selling in the second half. Underlying futures have pared gains in the second half, curves twist steeper with short end rates outperforming. US Gov shutdown likely at midnight tonight. Projected rate cut pricing gaining vs. late Monday levels (*): Oct'25 at -24.2bp (-22.7bp), Dec'25 at -44.2bp (-41.3bp), Jan'26 at -53.7bp (-50.7bp), Mar'26 at -64.7bp (-60.9bp).

- SOFR Options:

- +15,000 SFRZ5 96.75 calls, 1.75 ref 96.31

- -12,000 SFRX5 96.12/96.62 strangles, 1.75-2.0

- -3,000 SFRV5 96.31 straddles, 6.25-6.0

- -12,900 0QV5 96.93 calls 4.5 ref 96.905

- 26,000 SFRX5 96.50/96.56 call spds

- 2,000 2QZ5 97.18/97.43 call spds ref 96.805

- 2,500 SFRX5 95.93/96.00/96.06 put flys ref 96.295

- 5,000 0QZX5 96.37/97.62 strangles

- +5,000 SFRF6 96.50/96.62/96.81 broken call flys, 0.5 ref 96.495

- 8,000 SFRZ5 96.06 puts ref 96.305

- +1,500 0QZ5 96.50/96.62/96.75/96.87 put condors, 3.5 ref 96.90

- 10,000 SFRV5 96.43/96.50 call spds, 0.25-0.5 ref 96.34

- +2,000 SFRZ5 96.18/96.31/96.50/96.62 put condors, 6.0

- +4,000 SFRZ5 95.93/96.06/96.18 put flys, 2.25

- Treasury Options:

- +87,000 TYZ5 113 calls, 46 vs. 112-19/0.42% (open interest 87,527 coming into the session). Paper was a large buyer of low delta calls last week: +100,000 TYZ5 113.5 calls, 38 vs. 112-21 to -21.5/0.35% and appr +200k TYZ5 114 calls since Mon from 31-33.+11,000 TYX5 111/112 put spds +1/-1 over 113.75 calls

- 8,600 FVX5 110 calls, 7.5 ref 109-07, total volume over 18.6k

- 10,000 TYZ5 113/113.5/114/114.5 4x4x4x3 call condors ref 112-19.5 to -20

- 4,400 FVX5 109.25/109.75/110/110.75 broken call condors, 6.5 ref 109-05.75/0.06%

- 2,000 TYX5 108.75/117.25 strangles ref 112-20

- +3,300 Wed Weekly TY 112.5 calls, 16 (exp 10/01)

FED: Vice Chair Jefferson: Softening Labor Market May Need Support

Fed Vice Chair Jefferson gave a speech early Tuesday morning that suggested a monetary policy outlook in line with that of most of the rest of the Fed leadership, including Chair Powell. As such we would guess he is among the 9 FOMC participants who anticipate making a further 2 25bp rate cuts by year-end to a median 3.6%, the same outlook that we think is shared by the core of the FOMC.

- He says "with respect to the path of the policy rate going forward, I will continue to evaluate the appropriate stance of monetary policy based on the incoming data, the evolving outlook, and the balance of risks. I will also consider and assess information about government policies and their effects on the economy."

- Like the broader Committee, "I see the risks to employment as tilted to the downside and risks to inflation to the upside. It follows that both sides of our mandate are under pressure".

- But he nods to greater risks to employment, noting "the unemployment rate could edge a bit higher this year before moving back down next year" and "With the unemployment rate at 4.3 percent, the labor market is softening, which suggests that, left unsupported, it could experience stress." As such he supported the September 25bp cut.

- On the economic landscape: "Recent data indicate that U.S. economic growth has moderated, and the risks to both sides of our dual mandate have shifted. Employment growth has slowed because of weaker growth in labor supply and a softening in labor demand. The uptick in the unemployment rate suggests that demand has fallen by a bit more than supply and that the downside risks to employment are rising. Meanwhile, higher tariffs are showing through to higher inflation for some goods. I expect that the effects of tariffs on inflation, employment, and economic activity will further show through in coming months."

- On inflation, his outlook is relatively benign, noting "core goods prices have been rising, reflecting tariff effects. In contrast, core services inflation, outside of housing, has generally trended sideways this year, while housing inflation appears to be on a gradual downward trend."

- He says that inflation expectations appear contained and "While tariff-related inflation is apparent in the prices of some goods, it is also notable that it so far has been lower than what many forecasters predicted this spring....I expect the disinflation process to resume after this year and inflation to return to the 2 percent target in the coming years."

EURJPY TECHS: Trend Theme Remains Bullish

- RES 4: 177.08 2.000 proj of the Feb 28 - Mar 18 - Apr 7 price swing

- RES 3: 176.00 Round number resistance

- RES 2: 175.43 High Jul 11 ‘24 and a key medium-term resistance

- RES 1: 175.13 High Sep 29

- PRICE: 173.55 @ 16:35 BST Sep 30

- SUP 1: 173.39/172.42 Intraday low / 50-day EMA

- SUP 2: 170.97 Low Aug 14

- SUP 3: 169.73/45 Low Jul 31 / 23.6% of the Feb 28 - Jul 28 bull leg

- SUP 4: 168.46 Low Jul 1

The trend EURJPY is unchanged, it remains bullish and the latest pullback is considered corrective. Recent gains confirm a resumption of the uptrend and maintain the bullish price sequence of higher highs and higher lows. MA studies are in a bull-mode too, highlighting a dominant uptrend. Sights are on 175.43, the Jul 11 ‘24 high and a key M/T resistance. The 20-day EMA has been pierced. Support to watch lies at 172.42, the 50-day EMA.