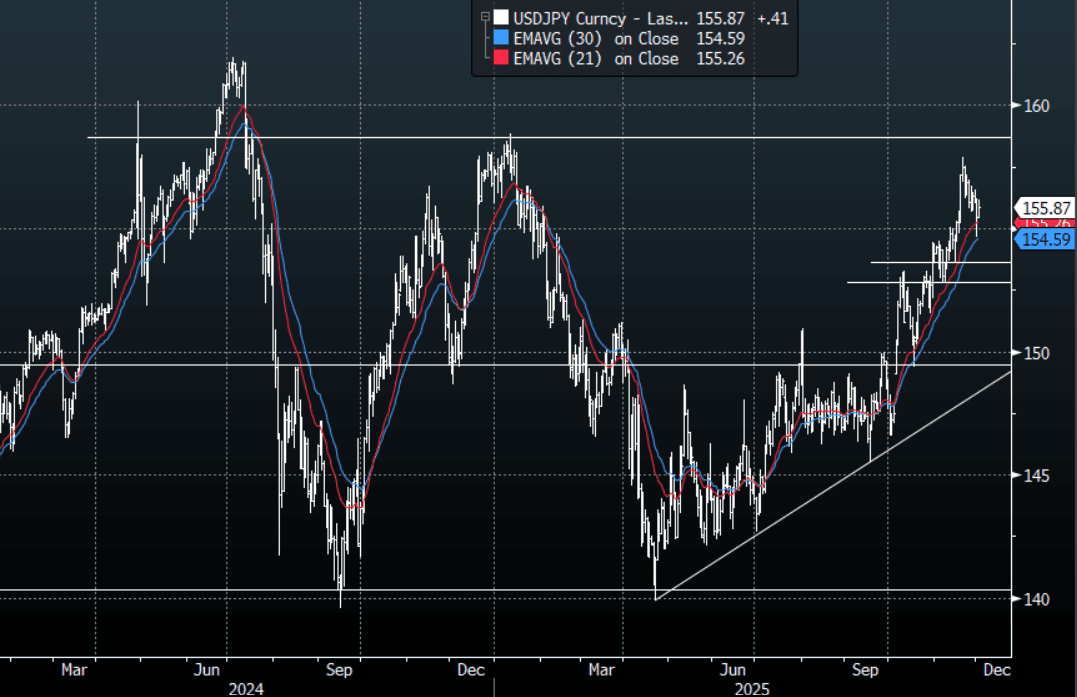

JPY: USD/JPY - Consolidates Around 156.00

The overnight range was 155.72 - 156.18, Asia is currently trading around 155.90. The pair chopped around the 156.00 area overnight without really going anywhere. The market is pricing in the fact that the Yen move looks like it could force the BOJ into action in December. This should keep the move that looked about to go parabolic a little more contained in the short-term but I suspect the market will still look for opportunities to express a long USD. Technically USD/JPY continues to look like it wants to test higher with the first big support back toward the 153-155 area which should see buyers remerge. In today's Asian session I suspect we will continue to consolidate within a wider 155.50-156.50 range, with risk turning around its poor start to the week a short Yen might best be expressed in the crosses.

- MNI POLICY: Ueda Sharpens Dec Rate Hike, Risks Credibility. A hold at the Bank of Japan’s Dec. 18–19 meeting would be inconsistent with the bank’s recent market communications and would undermine its credibility, following Governor Kazuo Ueda’s comments on Monday that strongly indicated policymakers are set to raise the 0.5% rate this month, MNI understands.

- Options : Close significant option expiries for NY cut, based on DTCC data: 155.50($1.27b). Upcoming Close Strikes : 153.00($1.2b Dec 4), 155.00($1.4b Dec 5), 156.00($1.14b Dec 8) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 101 Points

- Data/Event : S&P Global Japan PMI’s

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

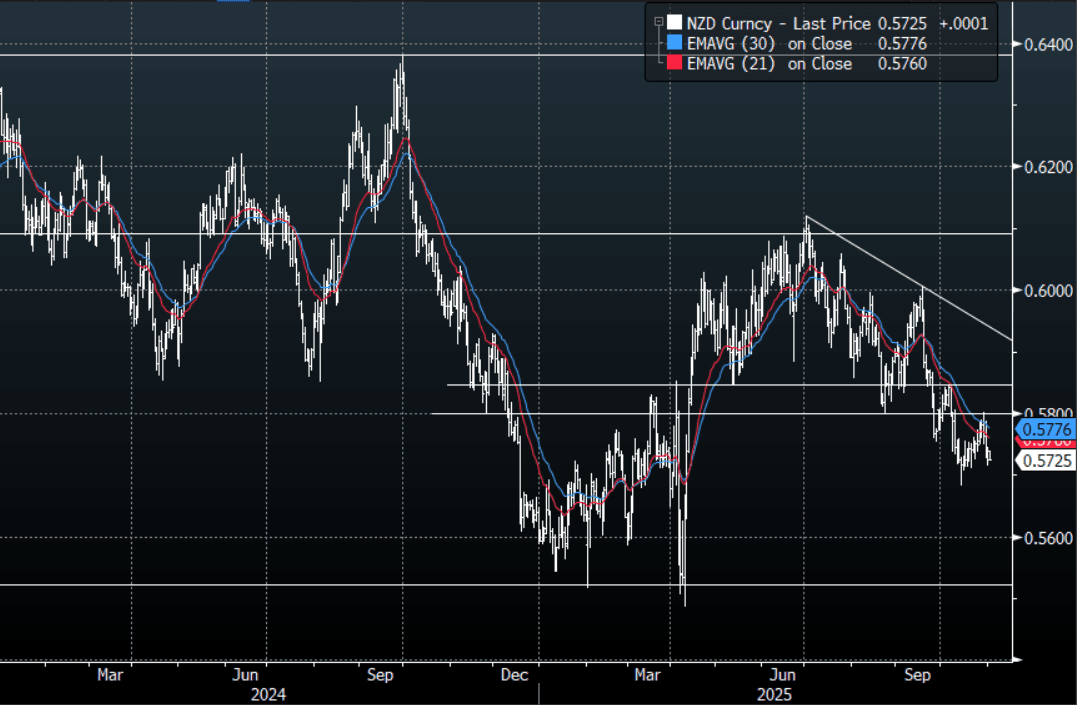

NZD: NZD/USD - Pauses Toward 0.5700, Remains A Sell On Rallies

The NZD/USD had a range Friday night of 0.5714 - 0.5733, Asia is trading around 0.5725. US yields retraced on Friday night but the USD continues to grind higher challenging levels last seen in July/August. The NZD found some demand back toward 0.5700 and consolidated in a tight range over month-end. While price remains below the 0.5800/50 area I suspect rallies continue to be faded looking for a potential move back towards the 0.5500/0.5600 area. NZD continues to stand out as a short against a resurgent USD but it is worth noting that because of the size of the market the market can very quickly become all positioned the same way, so I think the USD will need to build on its challenge higher for the NZD to test those lows.

- Bloomberg Economics is reporting Payrolls point to a deeper jobs slump and thus a 2% OCR. New Zealand’s labor market hasn’t stabilized yet. That’s their takeaway from the analysis of high-frequency payroll data. Apparent signs of a bottom in monthly jobs figures keep getting revised away, making it too soon for the Reserve Bank of New Zealand to take comfort. To secure a sustained recovery, the official cash rate will need to fall further below neutral. They see the OCR hitting 2.00% early next year.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5650(NZD1.1b Nov 5), 0.5675(NZD1b Nov 5), 0.5750(NZD604m Nov 5) - BBG

- Data/Event: October Cotality home values and September building permits are released today. The construction sector has lagged the rest of the economy but the ANZ business survey is showing some recovery.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUSTRALIA: RBA Expected To Be On Hold & Stay Cautious, Forecasts Updated

There are a lot of data releases this week but attention will be firmly on Tuesday’s RBA decision and accompanying press conference and updated staff projections. After trimmed mean inflation rose back to the top of the 2-3% band in Q3, the market and economists now broadly expect rates to be left at 3.6%. The CPI data drove those expecting a November rate cut to remove it from their forecasts. The Board is likely to remain highly data dependent and cautious given inflation’s renewed shift higher and the emerging domestic recovery.

- Given the RBA’s August trimmed mean CPI forecast was 2.6% in Q4 2025, the Q3 data is likely to drive a near-term upward revision to its inflation forecasts at a minimum.

- The consumer recovery is important to the RBA’s outlook and September household spending is published on Monday. Bloomberg consensus believes it will increase 0.4% m/m & 5.5% y/y after rising 0.1% m/m & 5.0% y/y. The Q3 volume measure will also be released, which should give an indication of consumption for the national accounts.

- The Melbourne Institute’s inflation gauge for October is released Monday. It has been trending higher since mid-year and rose to 3.0% y/y in September from 2.8%.

- In terms of housing, September building approvals print on Monday and are forecast to rise 5.0% m/m after falling 6.0% m/m. The series is volatile due to the multi-dwelling component.

- Monday also sees the final October S&P Global manufacturing PMI and ANZ-Indeed October job ads. Final October S&P Global composite & services PMIs are published on Wednesday.

- September merchandise trade prints on Thursday. The trade surplus is forecast to widen to $4bn from $1.8bn in August. Export growth has been soft while goods imports are picking up suggesting solid domestic demand.

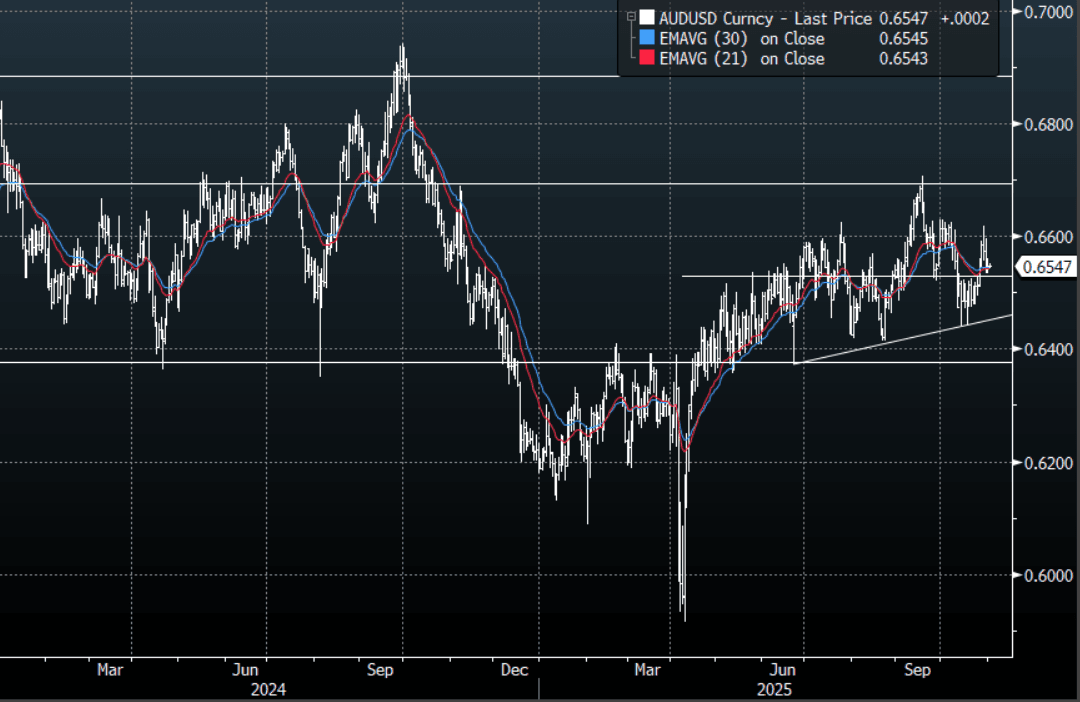

AUD: AUD/USD - Consolidates Around 0.6550 Ahead Of RBA Tomorrow

The AUD/USD had a range Friday night of 0.6533-0.6553, Asia is trading around 0.6545. US yields retraced on Friday night but the USD continues to grind higher challenging levels last seen in July/August. The AUD/USD is back within its recent 0.6400-0.6650 range with the pivot being around 0.6500-0.6550 where I would expect some demand first up, RBA tomorrow but the market is not expecting them to move.

- MNI Policy: RBA Board To Hold, Push Out Midpoint Return. The Reserve Bank of Australia Board is expected to keep the cash rate at 3.6% next Tuesday following stronger-than-expected Q3 inflation and is likely to push back the anticipated return of inflation to the midpoint in updated forecasts released alongside the decision.

- Bloomberg reports Australian home prices climbed at the fastest pace in more than two years in October, underscoring how a resurgent property market threatens to complicate the RBA’s efforts to cool inflation in this week’s rate decision.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6600(AUD 338m). Upcoming Close Strikes : 0.6625(AUD944m Nov 4), 0.6300(AUD600m Nov 4) - BBG

- Data/Event: Melbourne Institute Inflation, ANZ-Indeed Job Advertisements, Building Approvals, Household Spending

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P