JPY: USD/JPY Back To 156.00 On US Yield Fall, But Key Support Intact

USD/JPY fell under 156.00 (lows reached at 155.80) as the Fed cut 25bps as expected and wasn't as hawkish as feared in terms of the outlook. We track around 155.95/00 in early Thursday dealings. Yen gains were around 0.55% for Wednesday's session, but broader technicals are unchanged. Support at the 20-day EMA near 155.50 remains intact, while upside focus will rest on 157.89, the Nov 20 high and bull trigger.

- US Tsy yields were lower across the board on Wed, led by the front end (2yr off 8bps). US-JP yield differentials rolled back over but remain within recent ranges (2yr swap rate spreads around +225bps). This spread hasn't been able to break under +220bps in recent months.

- USD/JPY remains too high relative to yield differentials, but this wedge has been in place for some time.

- Market pricing for a Dec hike is off recent highs, while BBG notes: " Bank of Japan Governor Kazuo Ueda’s policy path may include as many as four rate increases by 2027, with three more coming after a widely anticipated move next week, according to a former executive director." The central bank outcome is due next Friday.

- On the data front today, we have the Q4 BSI survey for manufacturing and all industry, as well as weekly offshore investment flows. Later on Nov Tokyo office vacancies print. These prints are unlikely to shift the sentiment needle from a yen standpoint.

- Note in the option expiry space the following for NY cut later today: Y154.95-00($1.1bln), Y156.00($2.8bln).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Yields Rise on Shutdown Optimism

Treasuries finished weaker into the close, after trying to stage a comeback mid-way through the US trading day. As optimism increased over a potential US government shutdown end following eight Democrats broke ranks indicating their support, with a vote to come.

The US 10-Yr Treasury Futures had drifted to a low of 112-15+ before selling off to 112-26+ before rallying back to the mid-point of the range at 112-19+. The mid-point of the range is the mid-point between the 50-day EMA and the 100-day EMA. The 10-Yr is set to open at

Cash sold off with yields 1-3.5bps higher across the curve with the long end the best performers. The 10-Yr had trended around 4.12% before a further sell off to 4.1453%. A rally then preceded down below 4.10% before finishing at 4.11%. Whilst the odds of a rate cut in December has eased, the ebb and flow of treasuries overnight was aligned with the news flow on the government shutdown.

- The US 2-Yr is at 3.59% (+3bps)

- The US 5-Yr is at 3.719% (+3.3bps)

- The US 10-Yr is at 4.122% (+2.3bps)

- The US 30-Yr is at 4.711% (+1.1bps)

The bid to cover on both auctions exceeded the prior overnight, indicating strong demand for bills.

With the data calendar empty due to the shutdown and issuance focused on bills, the bond market's focus on shutdown headlines was inevitable and was the main driver overnight, and likely to continue today.

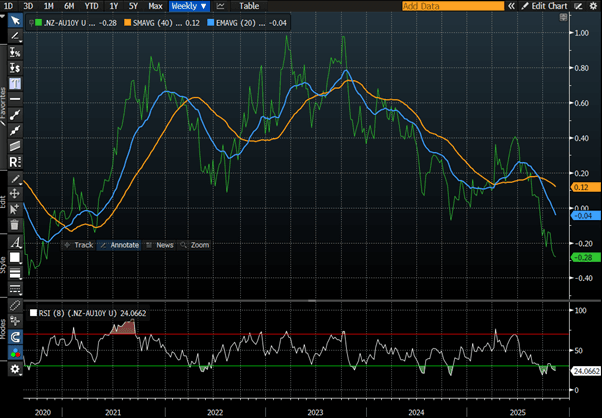

BONDS: Little Changed, NZ-AU 10Y Diff Near Cycle Lows

NZGBs are little changed despite US tsys finishing Monday’s session with a modest bear-flattener, with yields 1-3bps higher.

- Optimism buoyed as the US Govt shutdown appears to be nearer an end after eight Democrats broke formation with colleagues to reopen the Govt.

- Stocks rallied, led by chip makers while Health Care sector shares continued to decline in the second half - if the US Govt shutdown ends without an extension of Affordable Care Act (ACA) subsidies.

- No economic data on Monday, Tuesday limited to NFIB Small Business Optimism at 0600ET. Markets open for Veterans Day "holiday" - may weigh on volumes Tuesday.

- NZ-AU 10-year differential is 2bps wider at +28bps but near its lowest since 2020. (see chart)

- Swap rates are 1bp lower.

- RBNZ dated OIS pricing is little changed across meetings. 28bps of easing is priced for November, with a cumulative 37bps by February 2026.

- Today, the local calendar will see the RBNZ's Inflation Expectations data.

- On Thursday, the NZ Treasury plans to sell NZ$250mn of the 4.50% May-30 bond, NZ$150mn of the 4.25% May-34 bond and NZ$50mn of the 5.00% May-54 bond.

Bloomberg Finance LP

OIL: Signs US Government Shutdown To End Supports Risk Appetite & Oil

Oil prices were boosted by stronger risk appetite on Monday following news that some Democrats will support the bill to reopen the US government. The focus of the week will be on supply/demand information though – US inventory data and IEA/OPEC/EIA monthly reports.

- WTI rose 0.5% to $60.05/bbl but is still down 1.4% in November. It reached $60.48 before declining to $59.41 but moves below $60 were difficult to hold. Initial support is at $58.83, 6 November low, and resistance at $62.59, 24 October high.

- Brent was 0.7% higher at $64.07/bbl off the intraday low of $63.32. It made a high of $64.34 earlier. Technicals suggest that the benchmark is in a corrective cycle for now with initial resistance at $65.98 and support at $62.84.

- The US imposed an additional 25% punitive tariff on India for its Russian oil purchases. US President Trump said that a US-India trade deal is close which would reduce the average tariff rate. However, Russia’s Interfax reported that India continues to buy Russian crude despite Trump commending them for reducing purchases.

- Countries are finding ways around the sanctions on Russia’s Lukoil and Rosneft with the former’s West Qurna 2 field in Iraq being transferred to state firms to ensure production continues, according to Bloomberg.

- The market will monitor monthly reports closely this week for any deterioration in the excess supply situation. The IEA increased its 2026 surplus forecast in its October monthly report. It publishes updates on 13 November, while its annual outlook, EIA short-term energy outlook & OPEC report are out 12 November.