AMERICAS OIL: US OIL: Americas Open - WTI has recovered

US OIL: Americas Open - WTI has recovered from a low of $57.66/bbl after falling 1.4% yesterday amid Ukraine-Russia peace hopes, finding some support from data showing a US crude stock drawdown and increased December Fed cut pricing. US consumer confidence slipped this month but has been low for ten months as labor concerns persist. A stronger resumption of the bear leg would pave the way for a move towards key support and the bear trigger at $55.99, the Oct 20 low.

- The market is monitoring Ukraine developments with the US’ Witkoff to present the revised proposal to Russian President Putin and Driscoll to meet the Ukrainians after Ukraine said there’s a “common understanding” with the US for a peace plan. Key issues around security and sovereignty are apparently still unresolved.

- The market remains under general downside pressure, pricing in an oversupply next year despite OPEC+ plans to pause output hikes in Q1. The OPEC+ group next meet on Nov. 30

- Goldman Sachs said a peace agreement could cut base case oil prices by $5/bbl into the low $50s next year, according to Bloomberg.

- Russian crude exports to China are heading for the lowest since Feb. 2022 at about 825kb/d in Nov. so far, impacted by sanctions and limited import quotas, Kpler data shows.

- API data yesterday showed a US crude stock fell 1.9mbbl and with a 0.3mbbl draw at Cushing. Gasoline stocks rose 0.5mbbl and distillates rose 0.8mbbl.

- EIA US crude inventories released later today are expected to show a draw of 2.33mbbl and with gasoline build of 0.62mbbl and distillates draw of 0.03mbbl and refinery utilization 0.7%pts higher, a Bloomberg survey shows.

- US cracks are mixed with the gasoline crack higher but distillate lower ahead of the weekly inventory data that are expected to show builds in crude, gasoline and distillates after the API reported a crude draw and product builds.

- Recent weakness in WTI futures highlights a bearish theme. A stronger resumption of the bear leg would pave the way for a move towards key support and the bear trigger at $55.99, the Oct 20 low. Clearance of this level would resume the downtrend. Note that it is still possible a bullish corrective cycle remains in play. Resistance to watch is $61.84, the Oct 24 high. A clear break of this hurdle would signal scope for a stronger correction.

- WTI JAN 26 down 0.1% at 57.90/bbl

- US gasoline crack up 0.3$/bbl at 17.97$/bbl

- US ULSD crack down 0.4$/bbl at 38.93$/bbl

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: US Dollar Tilts Lower Amid Optimism for Risk

- As equities broadly consolidate their surge higher to start the week, the USD is trading on the back foot, with the likes of EUR and GBP rising to session highs in recent minutes, playing catch up to the AUD, which continues to outperform on the session.

- For EURUSD, although signs appear nascent, the pair has found support below the 1.1600 handle and a positive close today would be the fourth consecutive winning session. As noted above, markets will continue to monitor key support at 1.1542. JP Morgan hav noted that a close above 1.1710 would bolster their long bias conviction. In the crosses, EURCHF has bounced around 50 pips from the key medium-term support around 0.9210.

- GBPUSD has returned to 1.3350, however the string of losing session last week keeps a bearish threat present. EURGBP has been consolidating back above 0.8700, but will need a break above 0.8769 to confirm a resumption of the uptrend.

- Greenback price action has allowed USDJPY to fade further, after the overnight high practically matched the key resistance point at 153.27. The weaker dollar index sees spot gold off its worst levels, despite remaining down 1.9% on the session.

US TSYS: Early SOFR/Treasury Option Roundup: Leaning Toward Puts

SOFR/Treasury options flow leaning toward downside puts outright & spread, modest overall volumes on day 27 of the US gov shutdown. Underlying futures modestly lower/off lows ahead two bill and Tsy coupon auctions today. Projected rate cut pricing vs. late Friday levels (*): Oct'25 steady at -24.2bp, Dec'25 at -49.4bp (-50.2bp), Jan'26 at -62.2bp (-63.7bp), Mar'26 at -73.5bp (-75.8bp).

- SOFR Options

- 6,600 SFRZ5 96.50/96.62 call spds ref 96.36

- 9,000 SFRZ5 96.25/96.37/96.50 put trees, 7.5

- -2,000 0QX5 96.25/96.75/96.87 put flys, 1.5 vs. 96.97/0.08%

- 2,500 0QX5 96.75 puts, 0.25 ref 97.005

- +2,200 SFRX5 96.50/96.56 call spds, 0.25 ref 96.36

- Treasury Options

- 16,900 Friday wkly 10Y/TYZ5 113 put spd

- 2,000 TUF6 104/104.25/104.38/104.5 put condors ref 104-14.75

- +1,250 TYZ5 114 straddles, 119 vs. 113-06/0.43%

- +1,500 TYZ5 112 calls, 126 vs. 113-09/0.87%

- +2,500 TYZ5 112.5 puts, 15 vs. 113-09/0.28%

- -1,200 TYZ5 113.25 straddles, 106-107 vs. 113-05.5/0.05%

- over -8,000 wk5 TY 113 puts, 10-11, (exp 10/31)

- -5,000 USZ5 116/118 put spds, 46 vs 117-28/0.28%

- -2,700 TUG6 104.5 straddles, 34-33

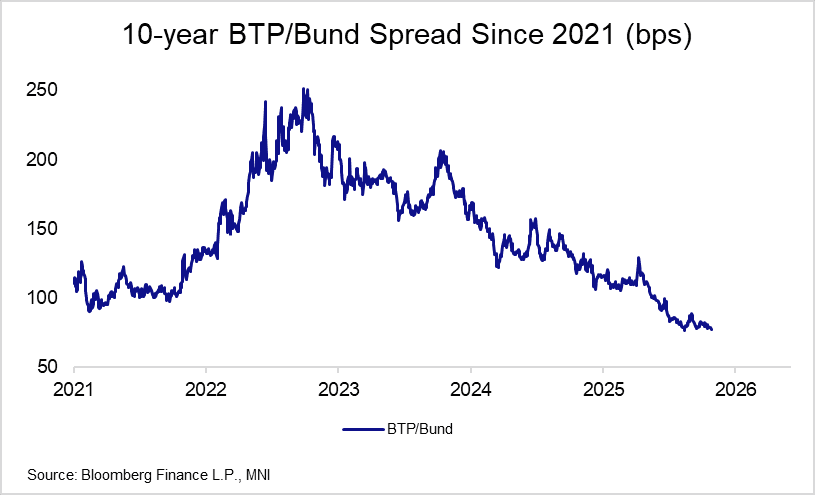

EGBS: /VOL: BTP/Bund Spread Eyeing Year-to-date Closing Low; Q3 Flash GDP Thurs

Improved risk sentiment and a pullback in EUR rates volatility has allowed the 10-year BTP/Bund spread to narrow to its lowest since mid-August. Confirmation of a US/China trade deal on Thursday could open the door for a test of the ~76.7bps year-to-date closing low seen on August 13. However, a push towards the 70bp figure may require stronger domestic activity signals, keeping focus on Thursday's flash Q3 GDP report (current consensus 0.1% Q/Q vs -0.1% prior).

- We have previously flagged that the biggest risk to Italian fiscal consolidation is not on the primary balance side, but on the country's subdued medium-term growth trajectory.

- The BTP/Bund spread is 1.5bps narrower at 77.5bps at typing, with benchmark Italian yields 0.5-1.5bps lower across the curve.

- EUR 3m10y swaption vol is ~1bp lower at 53.5bps, down from ~57bps on October 13. Goldman Sachs believe "the probability of a vol spike in Europe seems contained, given the decline in inflation, improved growth outlook and sufficient policy space to buffer eventual shocks". However, they note that "low valuations have lowered the bar for realized vol to outperform implied vol in Europe".