NATGAS: TTF Holds Near Low Amid Peace Talks, Mild Weather and Stable Supply

Nov-26 07:59

TTF front month is holding just above the lowest since May 2024 of €28.975/MWh yesterday amid Ukraine-Russia peace hopes, mild weather into December and stable supplies.

- The US’ Witkoff to present the revised proposal to Russian President Putin and Driscoll to meet the Ukrainians after Ukraine said there’s a “common understanding” with the US for a peace plan. Key issues around security and sovereignty are apparently still unresolved.

- Temperatures in NW Europe are forecast to gradually rise to near or above this week and hold steady into early December. CWE wind output has been revised up for most of this week until mid-next week.

- NW European LNG sendout was up to 276.1mcm/d yesterday compared to an average of 273.4mcm/d so far this month, Bloomberg shows.

- European gas storage was down to 78.14% full on Nov. 2, according to GIE data, with net withdrawals still more than normal. The previous five-year seasonal average is 88.4% full.

- Norwegian pipeline supplies to Europe are 333.2mcm/d today. Gassco shows total planned unavailable capacity of 28.4mcm/d until the end of the month but almost no planned outages next month.

- Algeria gas flow to Italy at Mazara is up to 64.8 mcm/d today compared to an average of 50.55mcm/d so far this month, Bloomberg shows.

- ICE TTF futures aggregate trading volume was 422k on Nov. 25.

- TTF DEC 25 up 0.1% at 29.43€/MWh

- TTF Q1 26 up 0.1% at 29.48€/MWh

- JKM Jan 26 up 0.2% at 11.02$/mmbtu

- US Natgas JAN 26 up 0.8% at 4.52$/mmbtu

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Opening Calls

Oct-27 07:57

Gilt Opening Calls, 93.12/93.20 range.

EQUITIES: EU Cash Openig Calls

Oct-27 07:55

Estoxx 50: +0.52%, Dax: +0.43%, CAC: +0.45%, FTSE +0.15%, SMI -0.10%.

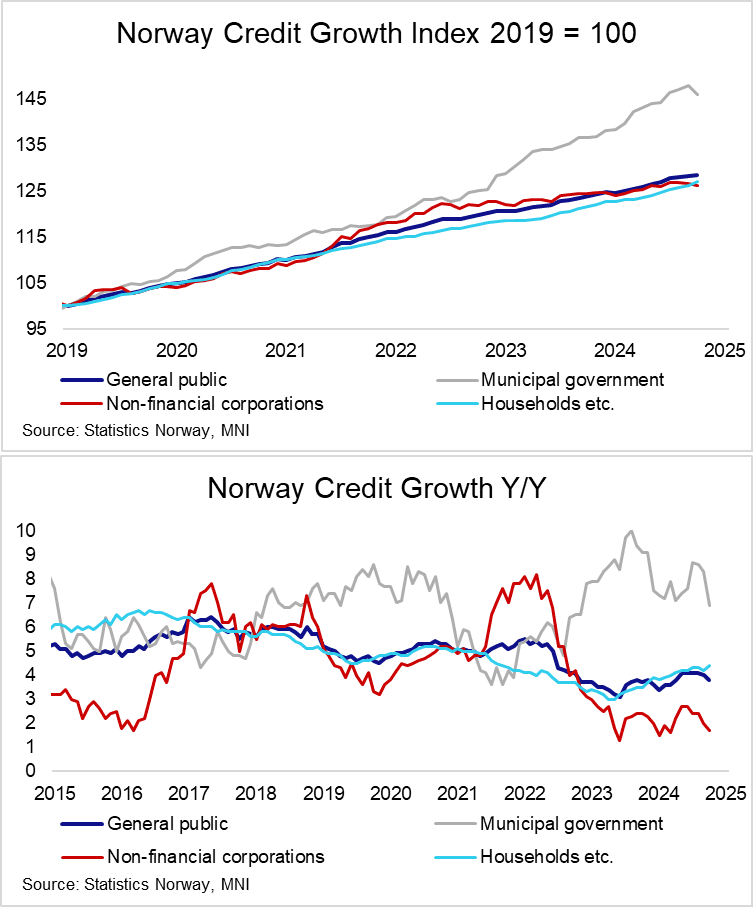

NORWAY: NFC Credit Growth Eases; Downside Econ Risks May Support Faster Cuts

Oct-27 07:42

- Although the Norwegian economy has been resilient through this year, fading offshore tailwinds and a more neutral fiscal policy stance may present downside risks in the years ahead. This may open the door to a faster pace of easing than currently signalled by Norges Bank. That said, no changes to the policy rate nor guidance are expected at next Thursday’s November decision.

- After peaking at 2.7% Y/Y in April/May, Norwegian non-financial corporate lending growth was fallen back to 1.7% Y/Y.

- Household credit growth instead accelerated to 4.4% Y/Y (vs 4.2% prior).

- This week’s Norwegian calendar includes September retail sales (Wednesday) and October unemployment claims data (Friday).

Trending Top

Mar-27 20:13