JGBS: Twist-Steepener On A Data-Light Session

In Tokyo morning trade, JGB futures are stronger, +9 compared to settlement levels, but off session bests.

- (MT Newswires) Japan's service sector growth momentum slowed in December 2025, with the Services PMI falling to 51.6 from 53.2 in November, indicating the softest expansion in business activity since May 2025, according to S&P Global's report.

- Cash US tsys are flat to 1bp richer, with a flattening bias, in today's Asia-Pac session. US ADP private employment & JOLTS data today, NFP Friday.

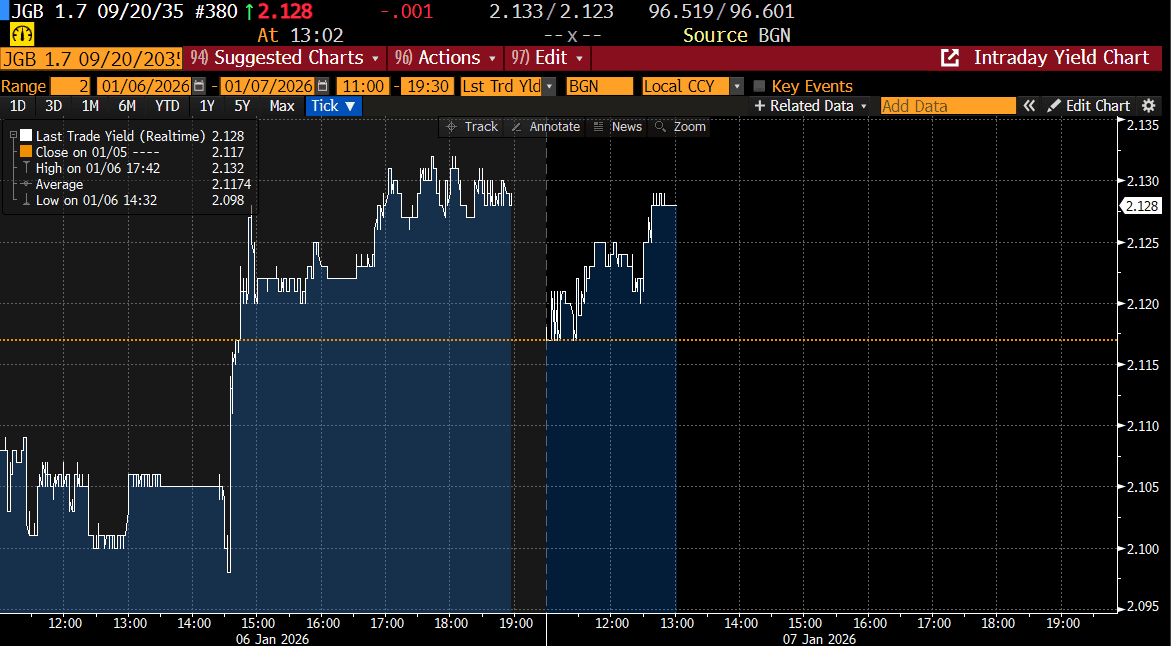

- Cash JGBs have twist-steepened across benchmarks, with yields 1.5bps lower (4-year) to 2.8bps higher (40-year). The benchmark 10-year yield is 0.1bp lower at 2.128% versus the cycle high of 2.134% (see chart).

- ICYMI, the 10-year JGB auction yesterday delivered weakish results, with the low price failing to meet expectations at 100.00, according to the Bloomberg dealer poll. Moreover, the cover ratio decreased to 3.3037x from 3.5913x and the tail lengthened to 0.05 from 0.04.

- Swap rates are 1bp lower to 2.5bps higher, with a steeper curve.

Source: Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

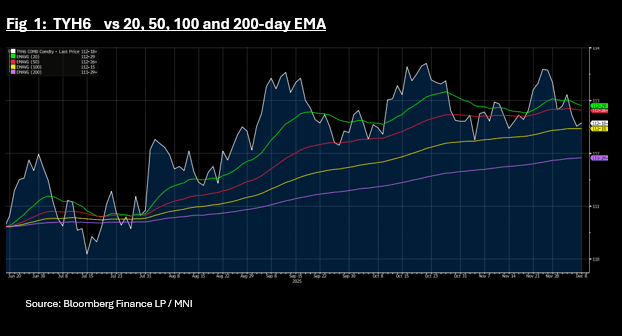

US TSYS: Yields Lower as TYH6 Fails Key Tech Resistance

US bond futures have edged higher in the Asia morning session, with the 10-Yr failing to break below a key technical. Opening at 112-18+ TYH6 was near to the 100-day EMA of 1132-15+ but has bounced higher in early trade to be up by +02 to 112-18+

Cash is stronger across the curve with yields -0.2 - -0.6 lower with short and intermediate maturities outperforming.

- The 2-Yr is at 3.556% -0.6bps

- The 5-Yr is at 3.708% -0.5bps

- The 10-Yr is at 4.133% -0.4bps

- The 30-Yr is at 4.791% -0.2bps.

Ahead tonight is a 13 and 26 week bill auction, with the focus being the U$58bn 3-Year auction.

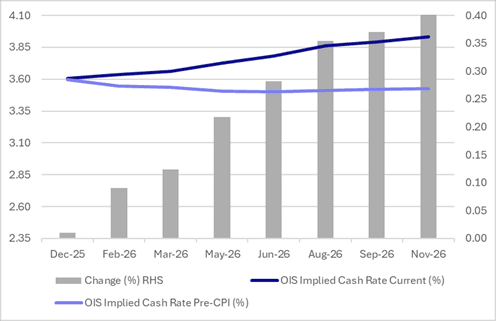

STIR: RBA-Dated OIS Pricing Fully Prices Hike By August 2026

RBA-dated OIS pricing is slightly firmer today, showing tightening across all meetings, with the probability of a 25bp hike rising from 2% tomorrow to 105% by August and 141% by December 2026.

- After today’s move, pricing is 9-40bps firmer across the curve beyond December 2025, than pre-Monthly CPI levels (26 November), led by December 2026.

Figure 1: RBA-Dated OIS – Current Vs. Pre-CPI Monthly

Source: Bloomberg Finance LP / MNI

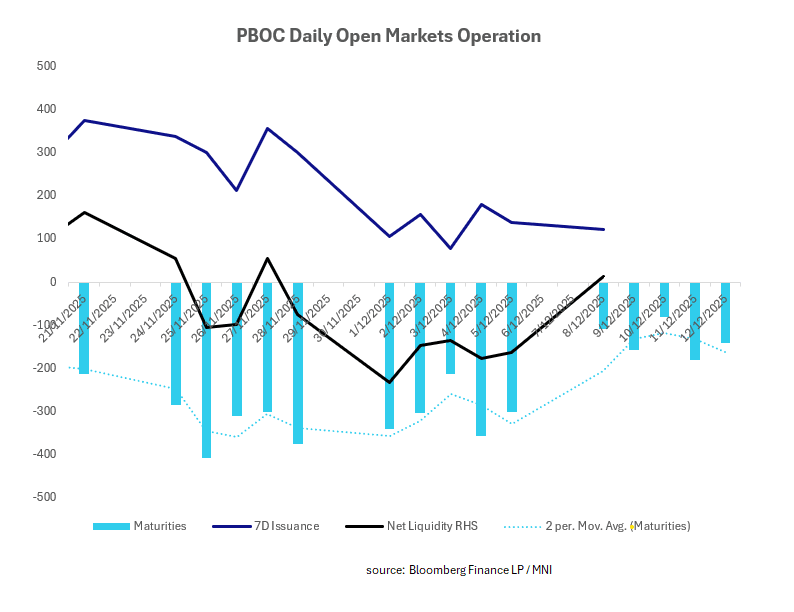

CHINA: Central Bank Injects CNY14.7bn via OMO

Last week the PBOC withdrew 7-day liquidity, adding 3-month liquidity. The week ahead has (relative to last) a more moderate redemption schedule and likely to see the resumption of some moderate injections.

- The PBOC issued CNY122.3bn of 7-day reverse repo at 1.4% during this morning's operations.

- Today's maturities CNY107.6bn.

- Net liquidity injects CNY14.7bn.

- The PBOC monitors and maintains liquidity in the interbank system through the issuance of reverse repo.

- The CFETS Pledged Repo Deposit Institutions 7 Day Weighted is at 1.40%, from prior close of 1.43%.

- The China overnight interbank repo rate is at 1.31%, from the prior close of 1.31%.

- The China 7-day interbank repo rate is at 1.40%, from the prior close of 1.40%.