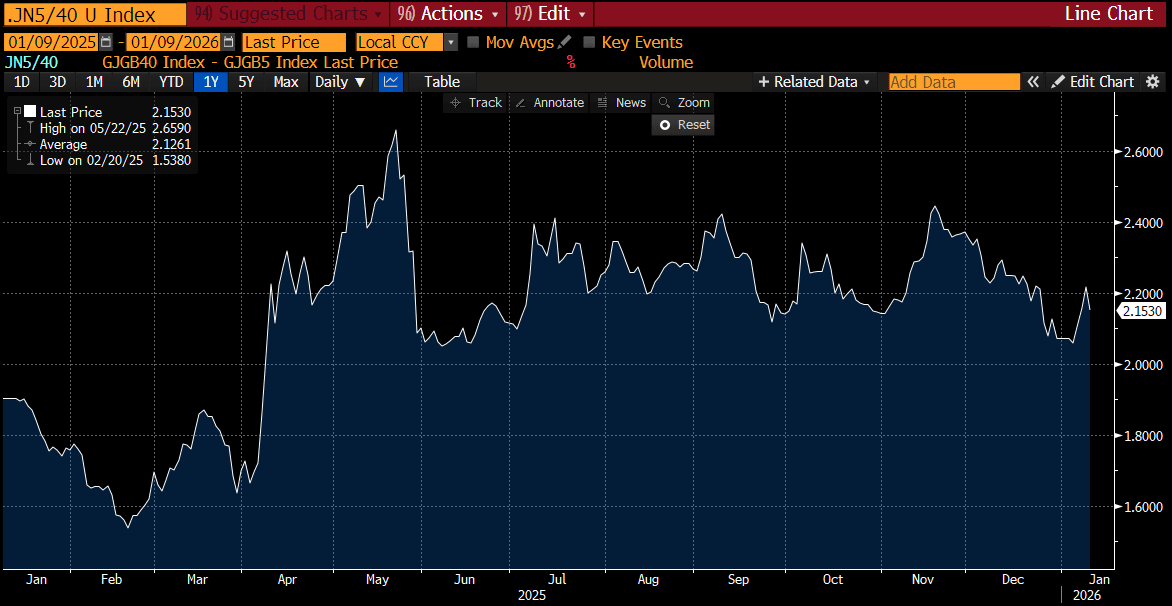

JGBS: Twist-Flattener, 5/40 Curve Flatter But Mid-Range

JGB futures are holding weaker, -19 compared to settlement levels, but have moved away from session cheaps seen in the aftermath of today’s stronger than expected household spending data.

- Japan real household spending rose 2.9%y/y in Nov, well above the -1.0% forecast and -3.0% Oct outcome. In m/m terms spending was up 6.2%, the strongest monthly rise since 2021.

- Real spending outcomes have been running ahead of the real cash earnings measure. This divergence widened in Nov. Whilst yesterday's labour earnings data was disappointing, the BoJ regional economic report still pointed to positive wage momentum for 2026 - via our policy team: many branch managers reported expectations for sustained pay increases, with several pointing to wage growth at levels similar to or higher than those seen in 2025.

- Cash US tsys are slightly cheaper in today's Asia-Pac session, with consensus looking for nonfarm/private payrolls growth of 69k/75k. The December data will carry more signal to the market and Fed than the highly unusual November report.

- Cash JGBs are holding a twist-flattening across benchmarks in today's session, with yields 2.2bps higher (5-year) to 4.2bps lower (40-year) (see chart).

- Swap rates are 1bp higher to 3bps lower, with the curve flatter.

- The local market is closed on Monday for a holiday.

Source: Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OIL: A Hawkish Fed Would Be Seen As Negative For Oil Demand, EIA Data Out Later

Crude has held onto most of Tuesday’s losses during today’s APAC session as it range trades ahead of the Fed decision later. A rate cut is widely expected, which is positive for US energy demand, but a hawkish tone regarding the policy outlook would likely weigh on oil prices. The EIA data release today could also be a market mover.

- WTI is up 0.2% to $58.35/bbl off the intraday low of $58.27, while Brent is also 0.2% higher at $62.05/bbl after falling to $61.96. The USD index is little changed.

- The market focus has returned to demand/supply fundamentals and it will be monitoring Thursday’s IEA and OPEC reports closely after today’s Fed and EIA data.

- A record market surplus in 2026 has been forecast for some time and upward revisions will be watched closely, especially given increased OPEC and non-OPEC output and elevated levels of seaborne crude.

- Bloomberg reported that US oil inventories fell 4.8mn barrels last week, according to those familiar with the API data. Product stocks were higher with gasoline stocks up 7.0mn and distillate 1.0mn.

- Not only is the FOMC decision announced later on Wednesday but Q3 US employment costs and November budget data also print. The BoC also decides rates. ECB President Lagarde gives an interview on the future of the euro and dollar. The ECB’s Donnery and Machado also appear.

FOREX: USD - BBDXY Well Supported Heading Into FOMC

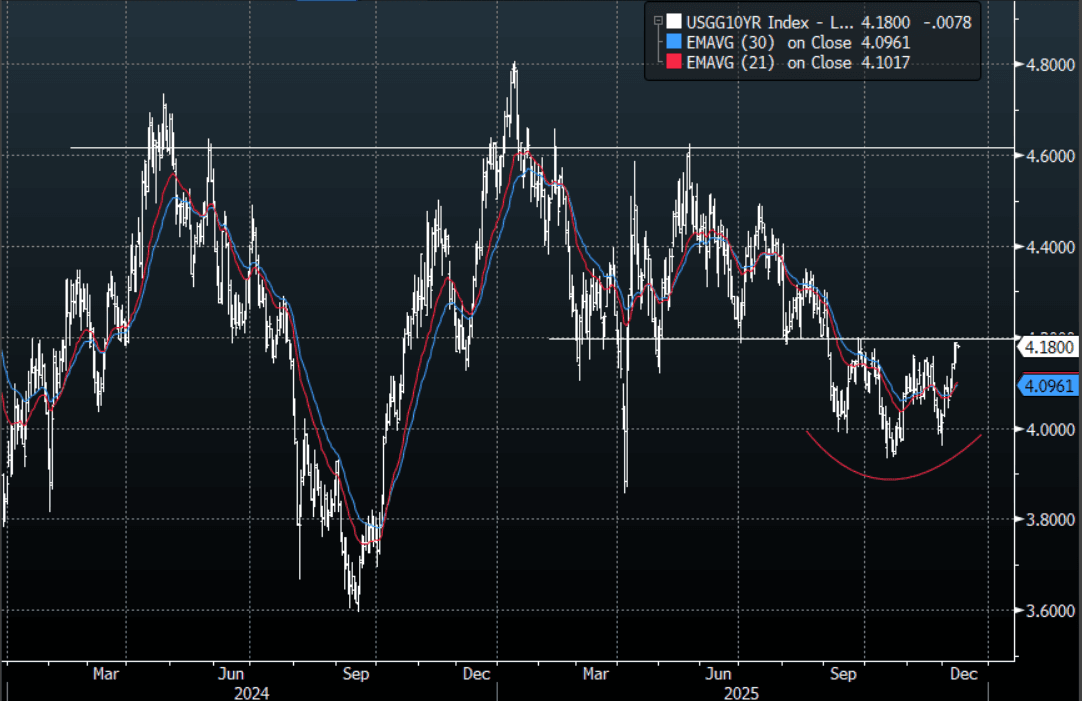

The BBDXY has had a range today of 1214.46 - 1215.08 in the Asia-Pac session; it is currently trading around 1214, -0.05%. The USD has traded sideways in a quiet Asian session. US yields continue to extend higher as we approach the FOMC, and both risk and the USD have begun to take notice. The USD continues to see decent demand back toward the 1210-1211 area and it looks like the range 1210-1230 could be here for the moment, or at least until the FOMC. On the day look for resistance again back towards the 1216-1218 area where sellers should remerge initially, a break above here would imply a test of the pivot around 1221-1223. The US 10-year yield is approaching the pivotal 4.20% area so the FOMC will have a big say in whether this area breaks or caps yields going into the end of year. Which has direct implications for the fortunes of the USD.

- EUR/USD - Asian range 1.1622-1.1629, Asia is currently trading 1.1625. The pair continues to consolidate above the 1.1600 area. On the day, all eyes will be focused on the FOMC tomorrow morning, dips toward 1.1580-1600 should be supported initially, looking to retest the 1.1660-1680 area again eventually.

- GBP/USD - Asian range 1.3296-1.3305, Asia is currently dealing around 1.3305. The pair is consolidating around the 1.33 area. I remain skewed toward shorts but patience is required and we are now approaching levels where I will be watching for any signs of potentially topping out. On the day GBP should see support back toward the 1.3250-1.3280 area, while above here look for the market to test the 1.3350-80 area again at some point. FOMC will dictate which side is tested.

- Cross asset : SPX +0.02%, Gold $4205, US 10-Year 4.18%, BBDXY 1214, Crude Oil $58.35

- Data/Events : Italy Industrial Production MoM

Fig 1: US 10-Year Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

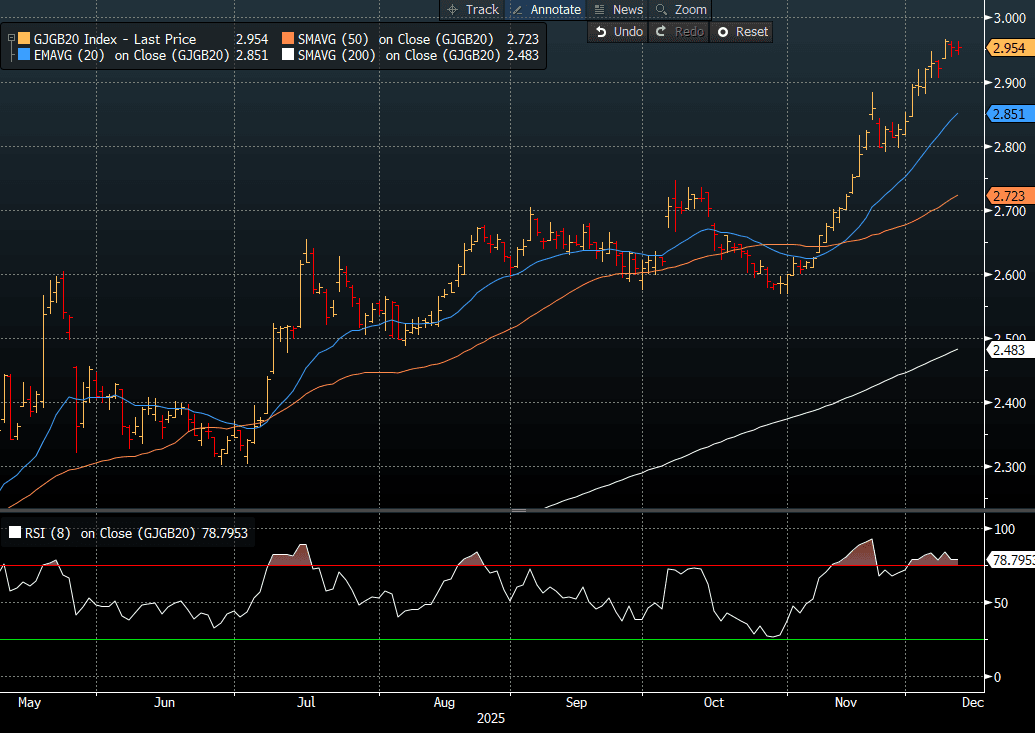

JGBS: Little Changed, PM: Econ Growth Vs Rising Yields, 20Y Supply Tomorrow

JGB futures are slightly weaker, -4 compared to settlement levels.

- PM Takaichi said Japan should prioritise economic growth rather than worry excessively about rising bond yields. She noted that yields reflect many factors, and it’s difficult to isolate the impact of fiscal policy. Takaichi emphasised that Japan’s debt-to-GDP ratio is gradually improving and highlighted the stability of the JGB market, supported by predominantly domestic ownership, while acknowledging potential risks if foreign ownership grows. – BBG

- She said rising yields have mixed effects on the economy, raising borrowing costs but also boosting household income. On currencies, she stressed the importance of stable, fundamentals-driven FX moves and said the government will act if market conditions become disorderly. - BBG

- Cash US tsys are ~1bp richer in today's Asia-Pac session ahead of today's FOMC policy decision. Inter-meeting communications reinforced that the FOMC is finely split between those who would ease further and those who are resistant - if not outright opposed - to providing further accommodation.

- Cash JGBs are little changed across benchmarks out to the 40-year (+15.bps).

- Swap rates are 1-2bps higher, with a flattening bias.

- Tomorrow, the local calendar will see BSI Survey, International Investment Flow and Tokyo Avg Office Vacancies data alongside 20-year supply (see chart).

Source: Bloomberg Finance LP