USDJPY TECHS: Trend Structure Remains Bullish

* RES 4: 160.21 2.236 proj of the Dec 5 - 9 - 16 price swing * RES 3: 160.00 3.000 proj of the Sep 1...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BOC: Governing Council Not Sure Whether Next Move Likely A Cut Or A Hike

The deliberations to the Bank of Canada's December meeting portrayed a Governing Council that was uncertain on the direction of its next move beyond the currently-signaled indefinite rate hold (link here)

- The key paragraph here mentioned that they discussed "whether it was more likely that their next move would be to raise or lower the policy interest rate. Given the high level of uncertainty, members agreed that while the current policy rate was at about the right level in the current situation, it was difficult to predict when and in which direction the next change in the policy rate would be."

- This was a little less subtle of a steer about the optionality being considered by Governing Council than Gov Macklem in the press conference, who didn't exactly dismiss the possibility of hikes next year, noting that BOC will be assessing data in a "symmetric way" in looking for material changes to the outlook in "either direction".

- Markets continue to pencil in a little under one 25bp rate hike through end-2026, unchanged vs before the Deliberations release.

- The messaging on the economy was basically in line with what we already heard in the policy statement and Gov Macklem's press conference.

- Indeed despite encouraging labor market and GDP readings, Governing Council was circumspect on the outlook. One of the key areas of uncertainty was on trade: "members agreed the Canadian economy was showing signs of resilience after a year of trade upheaval, but uncertainty remained high. They would remain cautious in interpreting incoming data given recent volatility and would be prepared to react if their outlook changed materially."

- In particular they discussed the upcoming trade renegotiations with the US and Mexico: "the upcoming review of the Canada-United States-Mexico Agreement (CUSMA) was a significant risk. The uncertainty leading up to and during negotiations would likely weigh on business investment. Members shared that business leaders they had met across the country saw the future of CUSMA as a significant strategic risk to their businesses. A worst-case scenario involving the dissolution of CUSMA and higher tariffs would be very damaging to the Canadian economy. Alternatively, a resolution of CUSMA negotiations that provided some stability in North American trade policy could spur on business investment."

EURGBP TECHS: Support Remains Intact For Now

- RES 4: 0.8865 High Nov 14 and a bull trigger

- RES 3: 0.8840 High Nov 20

- RES 2: 0.8818 High Nov 26

- RES 1: 0.8797 High Dec 17 and a key resistance

- PRICE: 0.8730 @ 15:42 GMT Dec 23

- SUP 1: 0.8721 Low Dec 9 & 23 and a key near-term support

- SUP 2: 0.8706 76.4% retracement of the Oct 8 - Nov 14 bull leg

- SUP 3: 0.8670 Low Oct 21

- SUP 4: 0.8656 Low Oct 8 and a key support

A bull cycle in EURGBP that started Dec 9 remains in place for now, and support to watch lies at 0.8721, the Dec 9 low. A clear break of this level would undermine the bull theme and instead signal scope for a deeper corrective pullback. This would open 0.8706, a Fibonacci retracement point. Initial key short-term resistance has been defined at 0.8797, the Dec 17 high. Clearance of this hurdle would be a bullish development.

US DATA: Corporate Profits Buoyant, But Disposable Income Slowdown A Concern

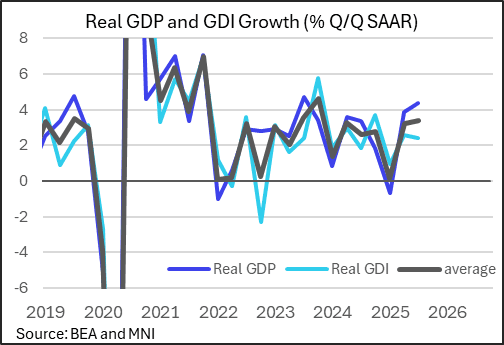

The 1st reading of Q3 GDP also included an initial read of real Gross Domestic Income (GDI), which posted an estimated 2.4% Q/Q SAAR growth rate. That's substantially lower than the GDP growth rate of 4.3% and slower than the 2.6% printed in Q2. We took note of relatively soft dynamics for personal income which stood in contrast to robust corporate profits.

- This was the 2nd consecutive quarter GDI has printed well under GDP; the average of the two measures nonetheless ticked up to 3.4% (3.2% prior) for the best reading since Q3 2023. It also makes for the biggest "statistical discrepancy" (GDP - GDI as % of GDP) at 1.2% since Q3 2024, but since the figures should theoretically be equal the differential tends to narrow over subsequent revisions.

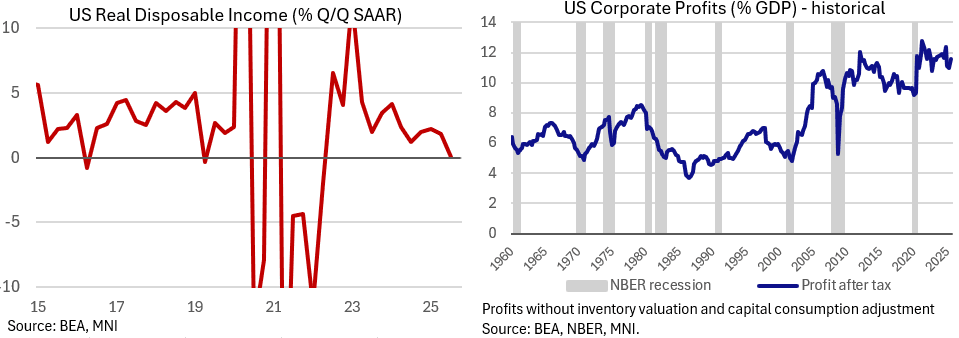

- Corporate profits (with inventory valuation and capital consumption adjustments) led the quarterly GDI gain, rising $166B (after a net negative 1st half, -$41.0). The breakdown of nonfinancial businesses ($100.4B)' profits by sector wasn't made available in this print, but overall they represented 2/3 of domestic industries' profits.

- After-tax corporate profits remain very elevated vs the longer-run historic series, at over 11% of GDP.

- We took note of relative weakness in personal income, however, with real disposable income growth basically flat in Q3 for the slowest growth since Q2 2022; the Y/Y rate (1.5%) was the weakest since Q4 2023.

- This came as nominal disposable income growth came in at just 2.8%, eroded by inflation; the savings rate fell to the lowest (4.2%) since Q4 2022.

- All of these series tend to get revised heavily in future quarters so we wouldn't read too much into it, but that marks the 2nd consecutive quarter of noticeable slowdown in real disposable income, amid a clear cooling in the labor market as a whole.

- It doesn't suggest particularly firm underpinnings to PCE spending, which is providing the single biggest pillar to growth (2.4pp of the 4.3% posted in Q3).