OAT: Tomorrow's 2026 Budget Outline The Next Source Of Risk For OATs

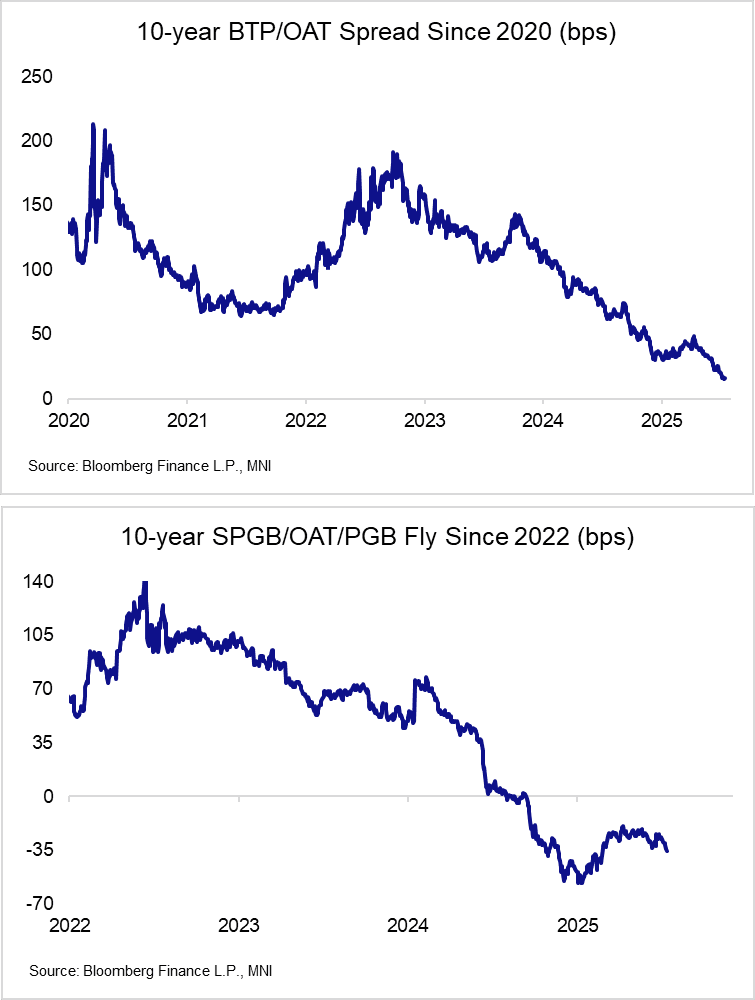

Tomorrow, French PM Bayrou is set to unveil the main proposals of the 2026 state budget, including spending cuts and tax hikes that risk collapsing his minority government. French political risks gradually been priced back into OATs in recent weeks, particularly when assessing French debt against semi-core/periphery peers. Last week, we highlighted a persistent tightening trend in the 10-year BTP/OAT spread, with markets eyeing full convergence if PM Bayrou is forced out of office.

- 10-year GGB yields have also moved below OATs this month, with the GGB/OAT spread currently below -2bps. Meanwhile, OATs have displayed renewed cheapening on the SPGB/OAT/PGB fly since the end of June.

- Bayrou has previously noted that E40bln in fiscal savings are required for the Government to meet its 4.6% 2026 deficit target.

- Without a majority, Bayrou is likely to be forced to use Art. 49.3 of the French constitution to push the budget through without a vote in parliament. The far-right RN party has threatened to vote in favour of a censure motion in the autumn should the PM utilise Art. 49.3, and with the parties of the left also on board, such a vote would be enough to remove Bayrou from office.

- A backdrop of political risks and ongoing fiscal pressures did not stop French President Macron from announcing an additional E6.7bln in defence spending by 2027 yesterday. Macron noted that this spending would not be financed by debt, but economic reforms and a "strength of soul" from the French people. No details were provided, but this is suggestive of the need for yet more fiscal consolidation.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US FISCAL: Available Extraordinary Measures Pick Up Ahead Of Tax Date

Treasury had $144B in "extraordinary measures" available to keep the government financed as of June 11 per a release Friday. That is up from $84B a week earlier and the highest since April 28.

- However, TGA cash continues to fall, to $309B latest (lowest since early April) Combined with a pullback in Treasury cash ($376B), keeping the total resources available to avert an "x-date" in the summer at around $450B .

- There will be another uptick in Treasury cash in the coming days, and it's likely Treasury allowed some of the extraordinary measures to be rebuilt (ie not exercised) in anticipation of more cash coming in.

- This is likely to be the last major uplift before the summer at which point x-date speculation will pick up if Congress hasn't passed a debt limit increase by then.

FED: Two Cuts Priced This Year Headed Into FOMC Week

As we head into the June Fed meeting week, market pricing is reflective of the FOMC’s messaging (that we describe in our preview):

- The next cut is only fully priced by the October FOMC meeting, with September seeing a roughly 80% implied probability of bringing the next 25bp reduction.

- Exactly 50bp of cuts are priced through end-2025, implying two Q4 cuts.

- That’s a shift from just after the May meeting, after which the next cut was fully priced by September, and there were closer to three cuts priced for the rest of the year.

- Overall cuts are seen backloaded this year (after 15bp in September, 29bp of cuts priced in Q4 - Oct/Dec combined), but falls off in Q1 (just 21bp cuts priced, 9bp of cuts priced for January and 12bp for March)

FED: Summary Of Economic Projections: Higher 2025 Inflation, Weaker Growth

The MNI Markets Team’s expectations for the updated Economic Projections are below.

- As of the May meeting, the Federal Reserve staff – whose outlook tends to be broadly shared by the median Committee member – revised their forecasts for growth weaker in 2025 and 2026, “as announced trade policies implied a larger drag on real activity relative to the policies that the staff had assumed in their previous forecast. Trade policies were also expected to lead to slower productivity growth and therefore to reduce potential GDP growth over the next few years. With the drag on demand expected to start earlier and to be larger than the supply response, the output gap was projected to widen significantly over the forecast period. The labor market was expected to weaken substantially, with the unemployment rate forecast moving above the staff's estimate of its natural rate by the end of this year and remaining above the natural rate through 2027."

- On inflation, "The staff's inflation projection was higher than the one prepared for the March meeting. Tariffs were expected to boost inflation markedly this year and to provide a smaller boost in 2026; after that, inflation was projected to decline to 2 percent by 2027."

- Our expectations for these changes fall somewhere in between those projections and the March SEP – a slightly higher unemployment rate, substantially higher inflation in 2025 but to a lesser extent in 2026, and weaker GDP growth this year. Longer-run variables should be unchanged.

MNI Markets Team Expectations For June 2025 Summary Of Economic Projections Medians