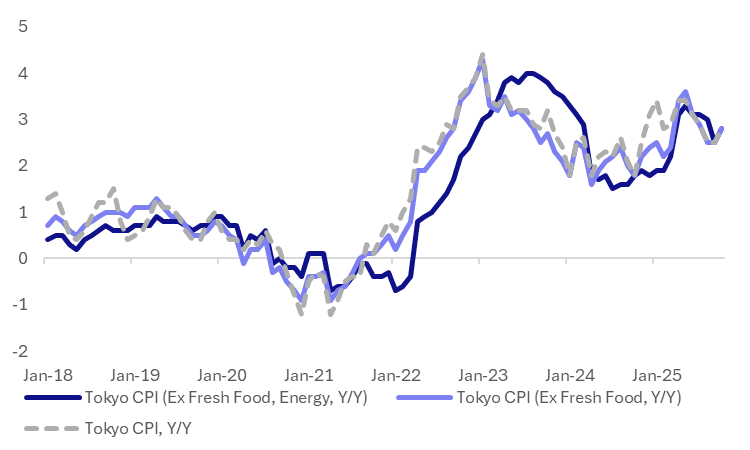

JAPAN DATA: Tokyo CPI Bounces, Strong M/M Detail, Firms Inflation Outlook

Tokyo Oct CPI was stronger than forecast, all the measures at 2.8%y/y, versus 2.4%y/y forecast for headline and 2.6% for the core ex fresh food and core ex fresh food, energy measures. The trends are presented in the chart below. We remain off 2025 highs, but are elevated from an historical standpoint. This data should add incrementally to the BoJ's confidence around achieving its inflation target (in the second half of its forecast horizon to March), but it is only one data print and would likely need to see further m/m evidence before bringing forward when it expects to hits inflation target (and therefore feel confident it can raise rates again). Note that retail and selling prices rose in October amid corporate price revisions typically implemented in April and October. Hence focus will be on follow up Nov/Dec trends.

- The m/m prints were firm across the board. The headline up 0.6%, while ex fresh food was 0.6% higher, and ex fresh food, energy gained 0.75. Goods prices rose 0.9%, while services were up 0.4%, after a 0.4% fall in Sep.

- The utilities 4.8%m/m rise helped the headline rebound, ending a four month run of declines. Subsidies impacted recent trends in this space.

- Gains were solid elsewhere though, with entertainment rebounding +1.9%m/m (after falling 2.6% in Sep). Transport was up 0.9% and household goods rose 0.6%. Food was also firmer at +1.2%m/m. Only clothing was down in m/m terms.

- In y/y terms, trends were relatively steady, with food to 5.9% from 6.1%. Entertainment rose to 2.7% from 1.9% prior. Only 4 out of the 10 sub categories have y/y rates above the 2% level.

Fig 1: Japan Tokyo CPI Y/Y Rebounded In Oct

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Cash Open

TYZ5 is trading 112-13+, down 0-02+ from its close.

- The US 2-year yield opens around 3.612%.

- The US 10-year yield opens around 4.158%, up 0.01 from its close.

- 10-Year yields remain subdued below 4.20% as the market prices in a US shutdown, I suspect buyers continue to be around 4.20% initially and look to fade the move higher. The jobs data if released will be key this week and if not then the ADP starts to take on a lot more relevance.

- MNI FED: Vice Chair Jefferson: Softening Labor Market May Need Support. Fed Vice Chair Jefferson gave a speech early Tuesday morning that suggested a monetary policy outlook in line with that of most of the rest of the Fed leadership, including Chair Powell. As such we would guess he is among the 9 FOMC participants who anticipate making a further 2 25bp rate cuts by year-end to a median 3.6%, the same outlook that we think is shared by the core of the FOMC.

- MNI US DATA: JOLTS Reaffirms "Low Hiring, Low Firing" Labor Market Narrative. Job openings were relatively steady in August in the latest JOLTS report, totaling 7,227k (SA, vs 7,200k consensus) with July's slightly upwardly revised to 7,208k (from 7,181k). But secondary metrics suggested further loosening in labor market conditions, and while there was no marked deterioration in the month, overall the report bolstered the prevailing "low hiring, low firing" narrative.

- Data/Events: MBA Mortgage Applications, ADP Employment Change, S&P Global US Manufacturing PMI, ISM Manufacturing, Construction Spending

MNI: BOJ: MAJOR FIRM FY25 CAPEX PLANS ABOVE HISTORICAL AVERAGE

- BOJ: MAJOR FIRM FY25 CAPEX PLANS ABOVE HISTORICAL AVERAGE

MNI: MNI BOJ SEPT TANKAN LARGE MFG INDEX 14; JUNE 13; MEDIAN 15

- MNI BOJ SEPT TANKAN LARGE MFG INDEX 14; JUNE 13; MEDIAN 15

- BOJ TANKAN LARGE NON-MFG INDEX 34; JUNE 34; MEDIAN 34