USDCAD TECHS: Testing Support

- RES 4: 1.4200 Round number resistance

- RES 3: 1.4192 Channel top drawn from Jul 23 low

- RES 2: 1.4140/67 High Nov 5 / 50.0% of the Feb 3 - Jun 16 bear leg

- RES 1: 1.4131 High Nov 21

- PRICE: 1.4051 @ 16:35 GMT Nov 26

- SUP 1: 1.4049/3991 20- and 50-day EMA values

- SUP 2: 1.3916 Bull channel base drawn from the Jul 23 low

- SUP 3: 1.3888 Low Oct 29 and a key support

- SUP 4: 1.3833 Low Sep 24

The bullish USDCAD condition has faded, with prices testing support Wednesday. While prices hold above the 20-day EMA, the pair will hold the bulk of its recent gains, keeping attention on any rally toward 1.4140, the Nov 5 high and the next key resistance. Note too that the top of the bull channel, drawn from the Jul 23 low, is at 1.4192 and also represents a key resistance. Key support to watch lies at 1.3991, the 50-day EMA. A clear breach of the average would expose the base of the channel at 1.3916.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: Macro Since Last FOMC - Growth: Mixed Private Surveys

Taking up some of the data slack since the government shutdown heavily curtailed official data, private sector surveys have been mixed whilst the Fed’s Beige Book suggested softer activity.

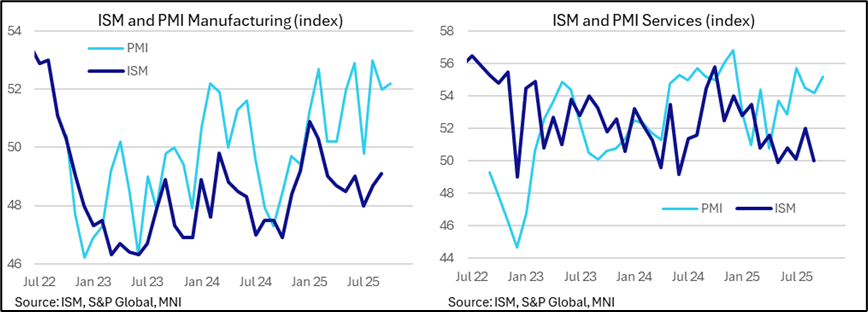

- ISM manufacturing index was little changed in September at 49.1 (highest since February, albeit by 0.1pt) although the ISM services index disappointed as it dipped 2pts to 50.0 for its lowest since May with new orders fully rewinding what had been a strong increase in August for also back towards the breakeven 50 level.

- More encouragingly, the latest flash S&P Global US PMI surveys for October were robust with the composite rising to a three-month high of 54.8 on the back of services strength, but there remains a significant discrepancy between the optimistic PMIs and much more subdued ISM surveys.

- Meanwhile, consumer confidence softened slightly in October according to the University of Michigan and Conference Board’s consumer survey will be released on day one of the two-day FOMC meeting, although Powell has cautioned on the poor correlation with realized consumption.

- Looking at overall economic activity, the Beige Book reported that while the same number of districts (4) reported declining activity, this time 5 saw little/no change in activity (2 prior) and just 3 reported growth (vs 6 prior).

- Despite the more mixed evidence from recent private releases, the prior momentum in the economy has seen Fed officials including both Powell and Waller ponder the gap between strong economic data and a weak labor market, including which might be a more reliable indicator.

FED: Macro Since Last FOMC - Growth: Robust Official Data Before Shutdown

With the sole major inflation report accounted for (see 1547/49ET bullets), we now turn to activity and labor market developments seen since shortly after the last FOMC meeting.

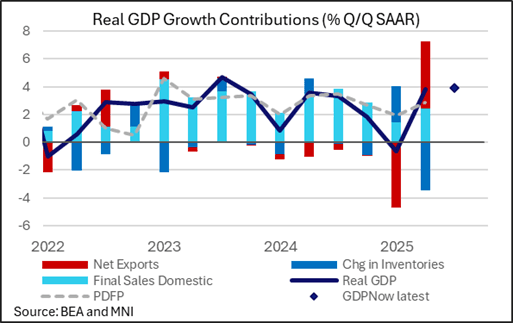

- Activity data continued a theme of surprising robustness the week after the FOMC decision, with the third release of Q2 national accounts seeing real GDP growth revised higher again from 3.3% to 3.8% annualized.

- Consumption helped drive it and in turn painted a much more encouraging picture for final sales to private domestic purchasers – a favorite of Fed Chair Powell’s – at 2.9% (revised from 1.9%) after the 1.9% in Q1 and 2.9% averaged in 2024.

- The following day, the monthly personal income and outlays report for August suggested this robust consumption growth continued well into Q3, rising a strong 0.4% M/M.

- Beyond that however and we are largely in the dark when it comes to official data, although it’s left economic activity clearly on a strong footing with the last update from the Atlanta Fed’s GDPNow pencilling in real GDP growth of 3.9% for Q3.

AUDUSD TECHS: Bullish Theme

- RES 4: 0.6660/6707 High Sep 18 / 17 and a bull trigger

- RES 3: 0.6629 High Sep 30 & Oct 01 and key short-term resistance

- RES 2: 0.6574 50.0% retracement of the Sep 17 - Oct 14 bear leg

- RES 1: 0.6560 High Oct 27

- PRICE: 0.6554 @ 16:27 GMT Oct 27

- SUP 1: 0.6440 Low Oct 14

- SUP 2: 0.6415 Low Aug 21 / 22 and a bear trigger

- SUP 3: 0.6373 Low Jun 23

- SUP 4: 0.6357 Low May 12

AUDUSD continues to trade above its recent lows. Attention remains on the Oct 14 reversal pattern - a hammer candle. It signals the end of the bear cycle that started Sep 17. Note that the initial firm resistance at 0.6541, the 50-day EMA, has been pierced. A clear break of this hurdle would strengthen a bullish theme. For bears, a breach of 0.6440, the Oct 14 low, would instead cancel the reversal pattern and reinstate a bear threat.