FRANCE DATA: Tariff Impact Clear, But Several Risks Still In Pipeline (2/2)

Ministry of Commerce data highlights a sharp drop in Y/Y French exports to the Americas since March, with exports falling 6.5% M/M in April and 6.4% M/M in May. The US makes up around ~80% of “Americas” exports. Clearly, already implemented tariffs and associated trade policy uncertainty are having an impact on trade with the US.

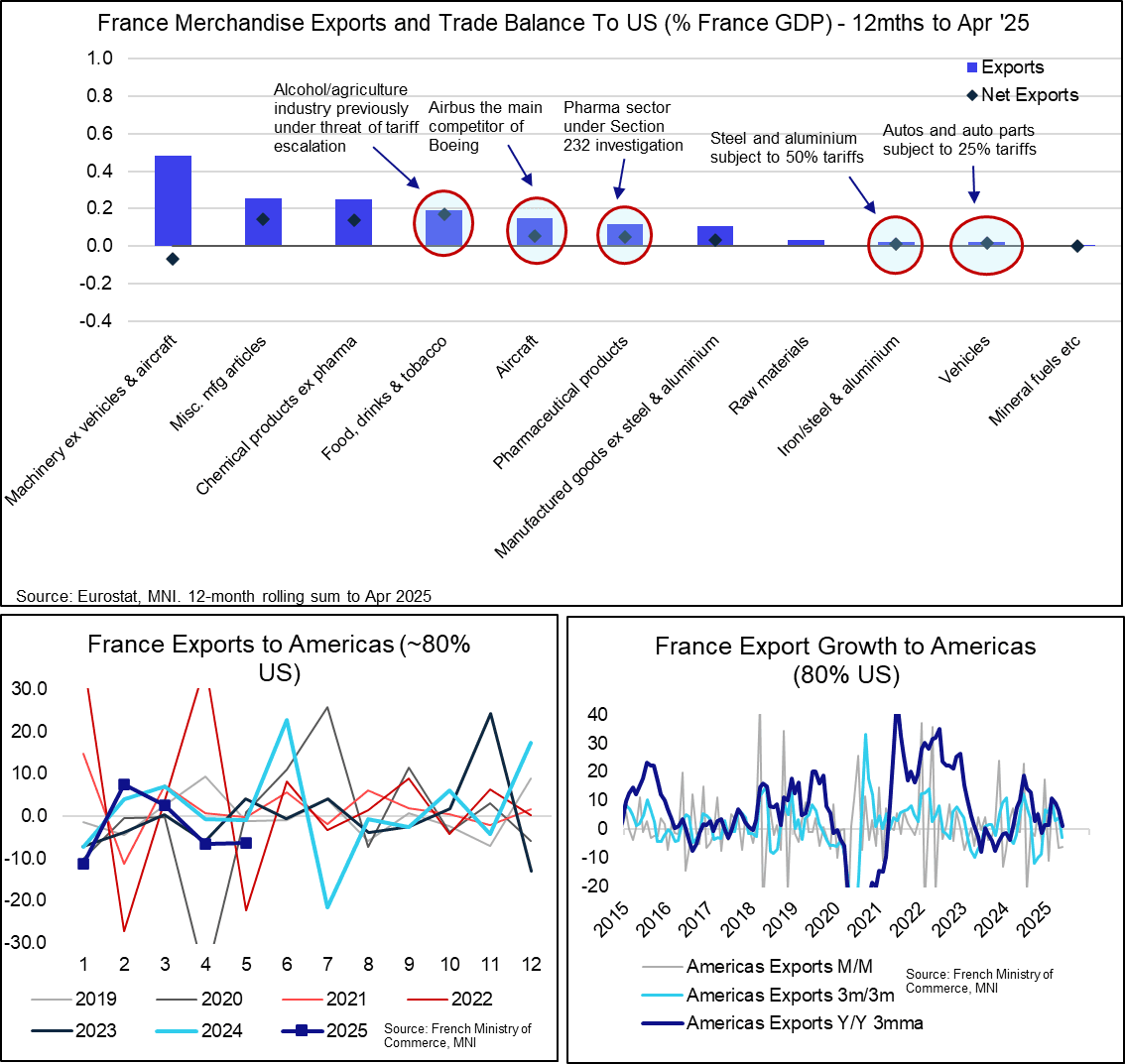

- However, Eurostat data suggests France is not too exposed to the sector-specific 50% steel/aluminium and 25% autos levies imposed by the US.

- Instead, officials will be more concerned by French sensitivity to:

- (i) Pharmaceuticals, which are currently subject to a Section 232 investigation.

- (ii) Aircraft, given Airbus’ position as Boeing’s main competitor.

- (iii) Food, alcohol and tobacco, with the agricultural sector threatened with 17% tariffs over the weekend and the alcohol sector previously being threatened with punitive measures following initial EU retaliatory plans.

- Other machinery/manufacturing exports to the US are also worth ~0.8% GDP, so are impacted by the 10% baseline reciprocal tariff.

- This sensitivity to potential future tariff announcements has likely underscored the French Government’s slower, more detailed, preference for trade negotiations than the likes of Germany (whose auto industry is more sensitive to already-announced sector-specific tariffs, for example). Reports that spirits and aircraft may be exempted from tariffs in the latest US offer will come as a relief to some French producers.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGB TECHS: (M5) Rallies Off Lows

- RES 3: 147.74 - High Jan 15 and bull trigger (cont)

- RES 2: 146.53 - High Aug 6

- RES 1: 141.48/142.95 - High May 2 / High Apr 7

- PRICE: 139.19 @ 15:53 GMT Jun 06

- SUP 1: 138.54 - Low May 22

- SUP 2: 136.57 - 1.382 proj of the Jan 28 - Feb 20 - Feb 26 bear leg

- SUP 3: 134.89 - 2.000 proj of the Jan 28 - Feb 20 - Feb 26 bear leg

JGBs have rallied off recent lows, however a bearish theme remains intact following the reversal that started Apr 7. A continuation lower would signal scope for an extension towards 136.57, a Fibonacci projection. On the upside, a reversal higher would instead refocus attention on 142.95, the Apr 7 high. The first important resistance to watch is 141.48, the May 2 high. A break of this level would be viewed as an early bullish signal.

US TSYS/SUPPLY: MNI UST Issuance Deep Dive: June 2025

We've just published our UST Issuance Deep Dive - Download Full Report Here

- May’s refunding round saw guidance as well as coupon sizes for the current quarter unchanged.

- The August round (Jul 28-30) could prove more compelling, reflecting both pressure at the long end of the Treasury curve as well as a shifting fiscal outlook amid tariff revenues contrasted with impending tax cuts (not to mention the likelihood of approaching the debt limit at around that time if it’s not lifted).

- Future Coupon Upsizing: We’ve seen some expectations that Treasury could lean against some of those trends in the August refunding, with potential signals if not immediate action on adjusting buybacks or even reducing issuance duration in order to reduce pressure on the long end. MNI’s current expectation is that coupon sizes will only be increased in early 2026. We will update in our next Deep Dive at end-June, with our full refunding preview coming in late July.

- Upcoming issuance: June is set to see $315B in nominal Treasury coupon sales, in addition to $23B in 10Y TIPS and $28B FRN for a total of $366B. Sales for the month start in the coming week, on Tuesday June 10 with $58B of 3Y Note, Wednesday June 11 with $39B of 10Y Note, and Thursday June 12 with $22B of 30Y Bond.

- May Auction Results: Against a backdrop of continued steepening pressure for global sovereign curves, May’s coupon auctions saw strong sales at the short-end/belly contrasted with tails at the long-end.

US FISCAL: Extraordinary Treasury Measures Tick Up As Cash Depletes

Treasury had $84B in "extraordinary measures" available to keep the government financed as of June 4 per a release Friday. That is up from $68B a week earlier though Treasury has exhausted three-quarters of the total initially available ($362B) when the debt limit impasse began in January.

- Combined with a pullback in Treasury cash ($376B), the total resources available to avert an "x-date" in the summer are down to a total $460B, the lowest since April 10 before the annual tax take accelerated.

- There will be another uptick in Treasury cash late next week/early the following week around the mid-June tax date, but this is likely to be the last major uplift before the summer at which point x-date speculation will pick up if Congress hasn't passed a debt limit increase by then.