HYBRIDS: SoftBank: EUR Hybrids (SOFTBK; NR/B+/NR)

Oct-22 09:59

Not putting a formal FV on this but:

• IPT: EUR Bmk 37NC7 6.75%-7% (z+436-461)

• Seniors z+285

• Proximus Sub_Sen 133bps; TELEFO 140bps; Bayer 175bps; VW 164bps

• IPT Sub_Sen is 151bps at the tight end. (436 minus 285)

• The company successfully monetised Alibaba and is investing heaving in AI (OpenAI, ABB Robotics, Ampere).

• PROXBB 4.75 NC31 is the best comp but Senior Proximus is only z+95 in 7yr compared to z+285 for Softbank.

• The senior Softbank bonds look wide compared to PROXBB/JABHOL/EXOIM if the Hybrids go well.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGB OPTIONS: Bund Call Spread

Sep-22 09:58

RXX5 131/132cs, bought for 4.5 in 3k Total.

EQUITY OPTIONS: Estoxx Outright Put Seller

Sep-22 09:57

SX5E (19th Dec) 5300p, sold at 103 in 13k vs 4.55k at 5450.

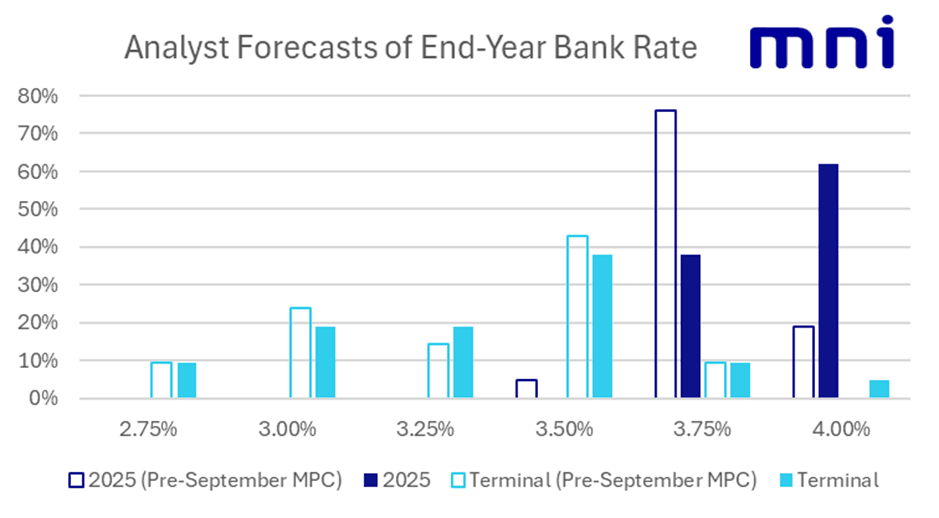

BOE: Analysts Push Back Cut Expectations Post-MPC; Still Less Dovish than Priced

Sep-22 09:52

- There has been a change in analyst views since the September MPC meeting, with the median and modal expectation of the next cut pushed back to February (from November). Note that this is more in line with market pricing (which prices cumulatively 17bp for the February meeting and less than 2bp for November).

- Almost half (10/21) of the analyst views that we tracked have pushed back their estimate of the next cut since the meeting.

- 6/21 look for the next cut in November, 2/21 in December, 11/21 look for February, 2/21 look for April and Santander looks for Bank Rate to end 2026 at 4.00%.

- There have been some tweaks to terminal rate expectations – but these have been much more limited with most analysts pushing cuts later rather than removing them from their forecasts altogether.

- 8/21 look for a terminal rate of 3.50% (the median and modal expectation). Almost half of analysts look for a lower terminal rate, however, with 4/21 looking for 3.25%, 4/21 looking for 3.00% while Citi and Morgan Stanley both look for a terminal 2.75%. NatWest Markets and RBC both see one final 25bp cut as their base case while Santander sees no more cuts through 2026.

- The downside skew to the terminal rate expectations from analysts is in contrast to markets which still don’t fully price 50bp of cuts to 3.50% from here.

- For a full summary of sellside views post-MPC meeting see page 7 of the MNI BOE Review here.