EGBS: SocGen Constructive Periphery In ’26, Eye Short-Term BTP & SPGB Steepening

While peripheral spreads vs. Bunds operate at the tighter end of multi-year (or longer) ranges, Societe Generale remain constructive on the periphery, suggesting that “spread convergence will likely remain the dominant theme in 2026”.

- This is based on “stronger fundamentals, improving ratings and sustained demand from both domestic and foreign investors. Conversely, core and semi-core countries will likely face headwinds from political uncertainty and heavier supply, particularly France and Germany”.

- They highlight “political risk will likely drive volatility in OATs, while BTPs and SPGBs should stay supported”.

- Still, Societe Generale don’t expect further outperformance for the periphery to come in a straight line, warning that “January could be volatile due to the Dutch pension fund transition”. They also look at seasonals, noting that 10–/30-Year EGB curves “typically steepen from mid-December to early/mid-January as markets anticipate the return of duration supply in January/Q1. This is especially true for BTPs and SPGBs, and we think it could happen again”.

- They therefore recommend tactical BTP and SPGB 10-/30-Year steepeners from mid-December through early to mid-January.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

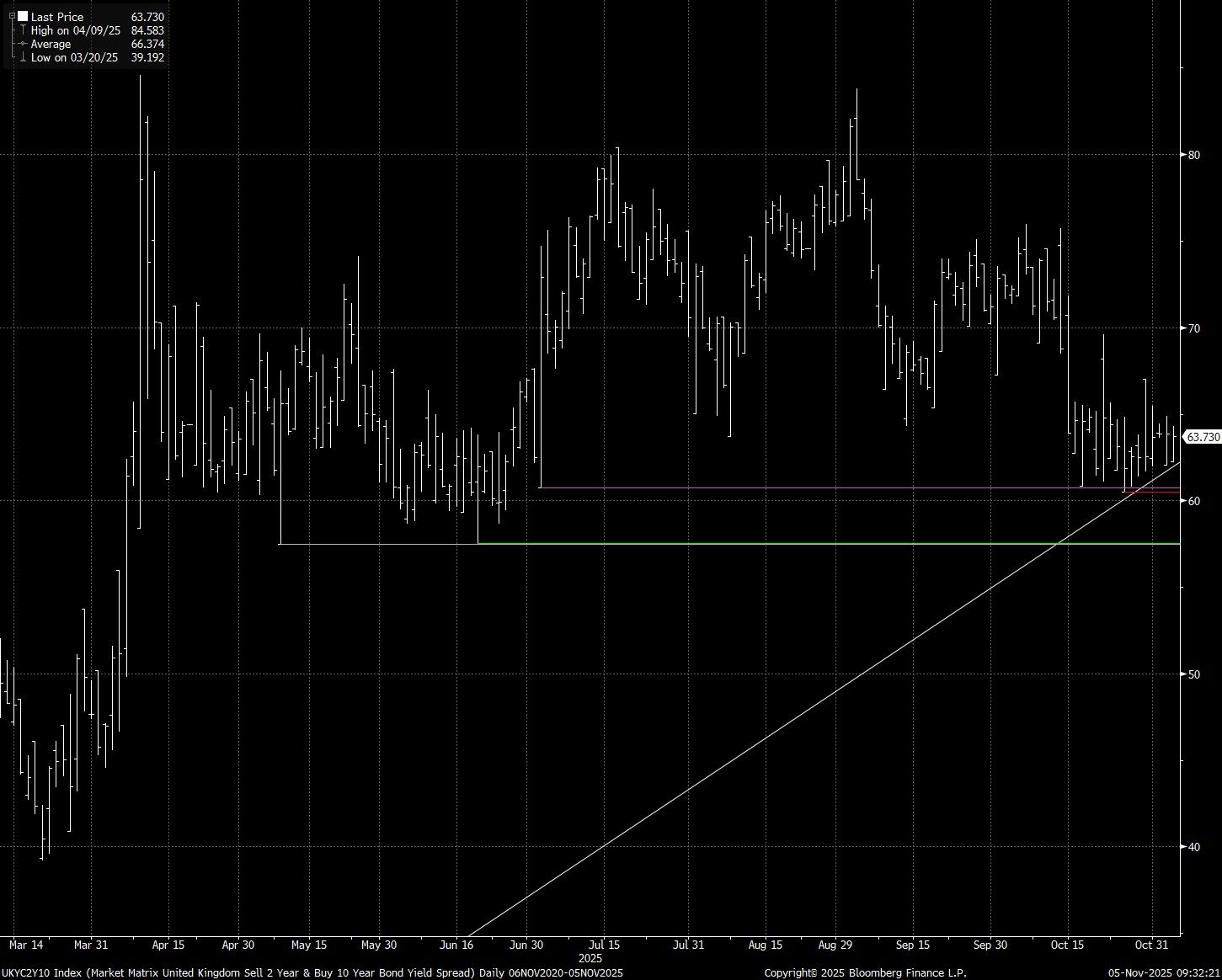

GILTS: Dovish BoE Outcome Could Drive Curve Steepening

Those looking for a dovish BoE outcome tomorrow may engage in 2s10s steepeners.

- The short end prices ~7bp of easing for tomorrow’s decision, which leaves the curve vulnerable to steepening if the decision comes in on the dovish side.

- We see a 50/50 risk of cut vs. hold, much more finely balanced than market pricing suggests. We would have more confidence in a cut if the Budget was not coming into view, particularly given the soft food CPI reading in the latest monthly inflation release.

- The curve has stabilised off of October’s low (60.5bp). Medium-term uptrend support drawn off the August ’23 low is holding at this stage (see chart below).

- Any further increase in confidence in the Chancellor’s ability to deliver meaningful fiscal tightening would present a risk to steepeners.

Fig. 1: 2-/10-Year Gilt Curve (bp)

Source: MNI - Market News/Bloomberg Finance L.P.

EUROZONE DATA: Oct PMIs: Growth Momentum Improving Everywhere Except France

The October PMI round signalled a positive start to Eurozone growth momentum in Q4. With Q3 flash GDP having already printed above the ECB's September projections, the case for unchanged policy rates going forward is growing. However, some ECB officials remain cognisant of downside risks heading into 2026.

Following upward revisions in France and Germany, and stronger-than-expected readings in Italy and Spain, the Eurozone services PMI was revised up to 53.0 (vs 52.6 flash, 51.3 prior). With the manufacturing PMI confirming flash estimates at 50.0 on Monday, this left the composite reading at a 29-month high of 52.5.

At a country level, France's underperformance amid ongoing political uncertainty remains stark.

Summary from the final October composite PMI release:

- "The euro area economy saw its strongest expansion since May 2023 during October, with growth accelerating and tentatively pointing to a breakout from the subdued trend seen in the first nine months of the year. This sharper upturn was supported by improved demand conditions as new business rose at the steepest pace for two-and-a-half years. Employment growth meanwhile quickened to a 16-month high, despite a slight weakening of businesses’ year-ahead activity expectations".

- "As for prices, input cost inflation eased for a second month running, taking it further below its historic average. Euro area companies were more aggressive with their price setting, however, lifting their charges to the greatest extent in seven months"

UK DATA: Upward Revision To Oct Services PMI, But Fall In Employment Still Noted

Momentum in UK services activity remains positive, though October’s 52.3 final read remains below August’s 54.2. While stronger new orders supported the aggregate index, another reduction in employment numbers and easing output charge inflation will be noted by the BOE.

Key notes from the UK services PMI release:

- “Survey respondents cited a gradual turnaround in new work and sales opportunities, despite elevated business uncertainty and delayed decision-making among clients”

- “Anecdotal evidence suggested that a rebound in order books and successful new product launches had helped to boost business activity in October.”…“Stronger order books appeared to reflect rising domestic demand, with service providers noting increased marketing spending and greater sales enquiries. In contrast, new work from abroad decreased for the second month running”

- “October data pointed to only a slight reduction in employment numbers across the service economy” … “Where a reduction in headcount was reported, this mainly reflected efforts to offset higher payroll costs through the non-replacement of voluntary leavers.”

- “Input cost inflation remained historically strong , but moderated for the second month running to its lowest since November 2024. Higher salary payments were commonly reported”

- “ Average prices charged by service providers meanwhile increased at the slowest pace since June,”