STIR: SNB Expectations Unfazed By Tariff Threat Ahead Of Swiss CPI

Market expectations for near-term SNB policy were materially unchanged following yesterday's 39% tariff threat by the US administration (as well as today's weak US data), with OIS markets continuing to price in around a 20% of a cut into negative territory at the next September meeting, and cumulatively around 16bp of easing from current rates through the March 2026 meeting.

- The lack of STIR market reaction comes despite first domestic commentary seriously cautioning against a scenario of the announced tariffs actually materializing (KOF Sees 0.3% - 0.6% Negative GDP Impact Of Announced US Tariffs ). Drivers for the lack of price action could include the following:

- i) The potential for the tariff announcement to be a last-minute negotiation tactic - (recall quotes last Thursday (Roche CEO Sees US Trade Deal in "Matter of Days, If Not Hours") which would imply some delays might have happened in coming to a final agreement. However, against that backdrop, note the Swiss government's reaction here (US Off-Switzerland Refused To Make Concessions On Trade Barriers), flagging it would be "very difficult for Switzerland to offer more concessions to the US" - which would complicate any easing from here.

- ii) The SNB policy rate is already at 0%, raising the bar for further easing, as stressed in detail by SNB Chairman Schlegel in their last post-meeting press conference. Judging by SNB rhetoric, this bar will only be met through a material threat to Swiss inflation leaving the SNB's target range mid-term. The question here would be how firm the secondary effects of an economic downturn induced by the external sector could be.

- This leaves a key focus for SNB expectations ahead on CPI developments in Switzerland - with the July release to be published Monday.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GBPUSD TECHS: Monitoring Support

- RES 4: 1.3852 1.764 proj of the Feb 28 - Apr 3 - 7 price swing

- RES 3: 1.3835 High Oct 20 2021

- RES 2: 1.3800 Round number resistance

- RES 1: 1.3789 High Jul 01

- PRICE: 1.3599 @ 16:10 BST Jul 2

- SUP 1: 1.3586/63 20-day EMA / Low Jul 02

- SUP 2: 1.3439 50-day EMA

- SUP 3: 1.3338 Trendline support drawn from the Jan 13 low

- SUP 4: 1.3140 Low May 12 and key support

A bull cycle in GBPUSD remains in play and a fresh cycle high Tuesday reinforces bullish conditions. This maintains the price sequence of higher highs and higher lows. Note too that moving average studies are in a bull-mode position, highlighting a dominant medium-term uptrend. Today’s move lower appears to be a correction. Support to watch lies at 1.3586, the 20-day EMA. A break would signal scope for a deeper corrective pullback.

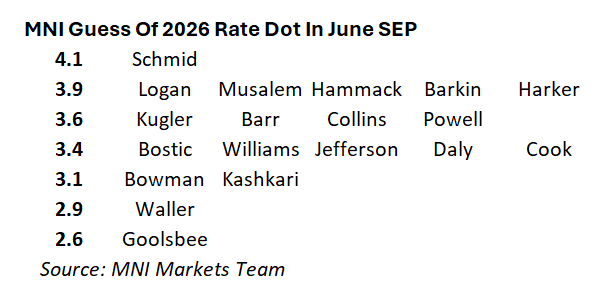

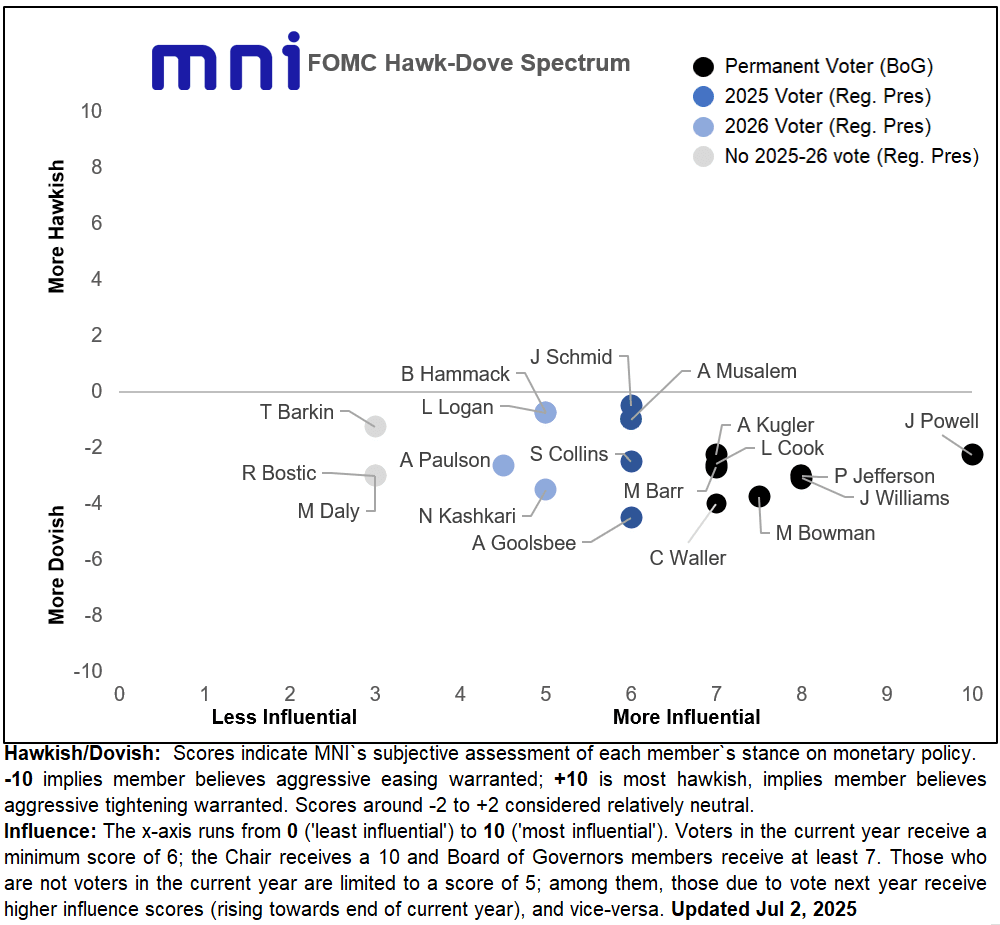

FED: MNI Hawk-Dove Spectrum Eyes End-2026 Rate Views (3/3)

Our FOMC Hawk-Dove Spectrum has shifted since pre-June FOMC to reflect some of the latest commentary on future easing. This is based in part on where we think (or in the case of Bostic and Kashkari, we know) they penciled in end-2026 rates in the June SEP (recall the median was 3.6%).

- We had to pick a "1 cut through end-2026" candidate and that is probably Logan, Hammack or Schmid - we guess the latter.

- Likewise despite Goolsbee not being the biggest dove for 2025, we think he probably continues to have the most dovish rate profile overall, with Bowman and Waller conversely front-loading their cuts.

- The Board is likely split largely between 3.4% and 3.6% end-2026, implying that most are eyeing 1-2 cuts in 2026 on top of 2 cuts by end-2025.

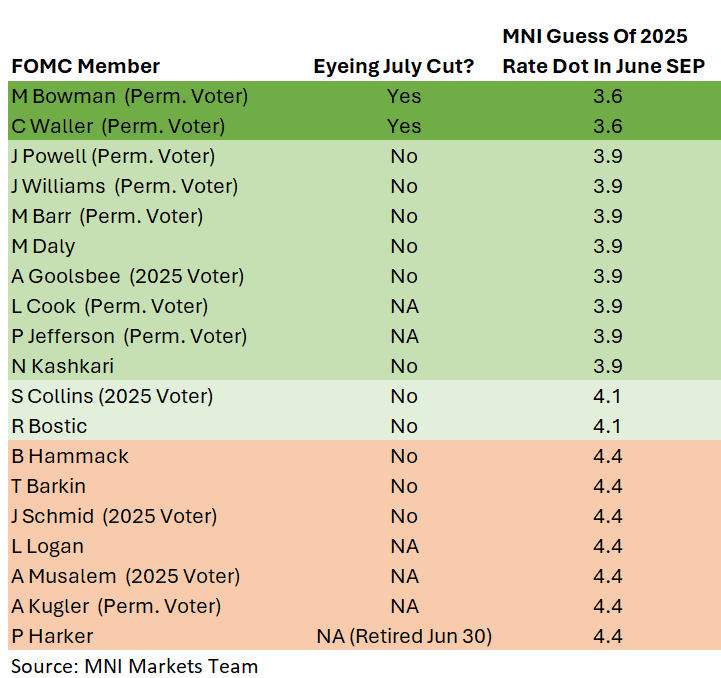

FED: Educated Guess On 2025 Dots Has Board Clustered At Median (2/3)

The MNI Markets Team's educated "guess" as to the June SEP submissions for the 2025 end-year dot is below. Note the median for end-2025 is 3.9% (2 cuts).

- Kashkari and Bostic have publicly revealed their "dots" for 2025 (and the case of the latter two, 2026), while Daly and Collins have implied theirs.

- Most of the Board are in the 2-cut median camp. Governors Cook and Jefferson haven't commented on monetary policy since the June FOMC meeting. At a guess, Gov Kugler is only board member who doesn't eye cuts this year, though that could also be Gov Barr, or Gov Cook who said pre-June FOMC that all possibilities, including hikes, were possible.

- Two of the more hawkish members, St Louis's Musalem (2025 voter) and Dallas's Logan (2026 voter) also haven't spoken on current monetary policy since the June meeting, though are scheduled to make relevant commentary on July 10 and July 15, respectively. We assume they are "no-cutters" for this year.

- We also haven't heard from new Philadelphia Fed President Anna Paulson (2026 voter) yet, though her predecessor Patrick Harker could easily have been any of 1, 2, or 3 cuts for 2025. We have him here as a rate-cut skeptic (in his last public appearance he suggested that the direction of the next move rates itself was a question).