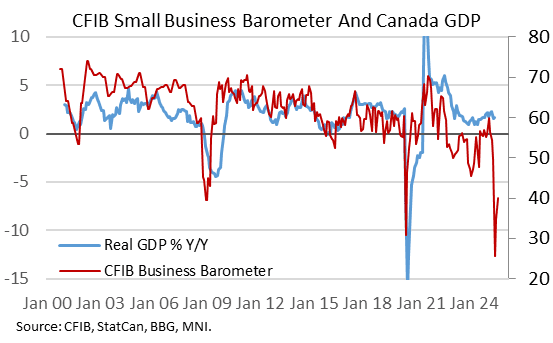

CANADA DATA: Small Business Confidence Rebounding, But Still Recessionary

May's CFIB Small Business Barometer showed a continued recovery in small firms' sentiment after an apparent trough in March. But at 40.0 in May (34.7 Apr, 25.5 Mar), the 12-month indicator remains in severely recessionary territory (compare these figures to a Global Financial Crisis low of 39.4 in 2008, and pandemic low 30.8 in 2020, both recessionary periods). The CFIB's chief economist characterised this as "just timid beginnings of a rebound...the optimism glass is not even half-full, it’s still fairly empty.”

- Tariffs are of course top of mind: "Half of small business owners are concerned that the U.S.-Canada trade dispute will have an impact on the summer tourism season, with businesses in recreation and information, retail, and hospitality being most concerned.

- In a benign development on the inflation front, "Inflation pressure indicators have eased, with small businesses planning to raise prices by an average of 2.9%, down from 3.5% in April. Wage plans remained unchanged at 2.1%."

- The report also noted: "All provinces have their confidence levels below 50. Weak demand remains the top barrier to growth for 59% of businesses, while over two-thirds (68%) of firms are constrained by tax and regulatory costs. Hiring intentions are far below seasonal levels, with 14% of businesses looking to hire full-time in the next few months and 16% planning to lay off."

- The "soft" data overall remain weak though perhaps less negative than in March/April at the extremes of negative sentiment over the US-Canada trade dispute.

- With April's CPI report showing more elevated core price pressures than expected, the case for a BOC cut on June 4 (now around one-in-three probability, market-implied) would appear to hinge on clearer evidence in the "hard" data that tariff uncertainty is translating through to activity to a degree that warrants accommodation. In that regard, Q1 GDP (May 30) could play a role.

- Consensus (per BBG) is for a +1.8% Q/Q annualized GDP reading in Q1 (in line with the BoC's April estimate, and vs +1.5% flash), swiftly followed by -0.5% in Q2 and 0.0% in Q3, effectively teetering on the edge of technical recession - the monthly March figure will be closely eyed for momentum (flash was 0.1% growth after -0.2% Feb and +0.4% Jan)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

PIPELINE: Corporate Bond Update: $5.7B to Price Tuesday

- Date $MM Issuer (Priced *, Launch #)

- 04/22 $2B #State Street $700M 3NC2 +73, $300M 3NC2 SOFR+95, $1B 5Y +85

- 04/22 $1.85B #Kinder Morgan $1.1B 5Y +120, $750M 10Y +150

- 04/22 $1.1B #NY Life Global $700M 3Y +60, $400M 3Y SOFR+88

- 04/22 $750M #Brookfield Asset Management 10Y +140

- 04/22 $Benchmark OCP 5Y, +10Y investor calls

- 04/22 $Benchmark Rentokil investor calls

US: FED Reverse Repo Operation

RRP usage climbs to $137.951B this afternoon from $114.114B yesterday. Usage had fallen to $54.772B last Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B. The number of counterparties at 42.

STIR: Fed Rate Path Climb Tempered By Trade Headlines

- Fed Funds implied rates have pared some of their sharp shift higher when Bloomberg first reported that US Tsy Sec Bessent said at a closed-door investor summit that he sees de-escalation with China whilst the current situation is unsustainable.

- The trimming of the day’s increase has come with subsequent headlines from Reuters re it likely to be a “slog” and Politico reporting the US is close on Japan and India trade agreements but with details suggesting less progress.

- Going against the trimming somewhat, a modest tail in the 2Y Tsy auction at 1300ET.

- Cumulative cuts from 4.33% effective: 3bp May, 18bp Jun, 39bp Jul, 58bp Sep and 89bp Dec.

- SOFR implied yields currently see largest increases in the M6 (+8bp), whilst the terminal remains in the U6 as it climbs to 3.15% (+7.5bp) for almost one additional 25bp cut priced vs pre-Liberation Day levels.

- Today’s Fedspeak from Vice Chair Jefferson (permanent voter) and Harker (retiring June) hasn’t moved markets, seemingly taking a deliberately non-confrontational approach amidst Trump’s latest demands for lower rates. Still to come today:

- 1340ET - Kashkari ('26 voter) at Chamber of Commerce Global Summit (Q&A only)

- 1430ET - Barkin (non-voter) fireside chat at innovation summit (Q&A only)

- 1800ET - Gov. Kugler (permanent voter) on monetary policy transmission (text + Q&A). She said Apr 7 that inflation was now the more pressing issue with regards to tariffs and that the Fed needs to make sure it doesn't rise. She warned the tariff impact should be consequential.