USDJPY TECHS: Slips Off Highs, But Uptrend Intact

- RES 4: 154.80 High Feb 12

- RES 3: 154.39 76.4% retracement of the Jan 10 - Apr 22 bear leg

- RES 2: 153.82 1.618 proj of the Sep 17 - 26 - Oct 1 price swing

- RES 1: 153.27 High Oct 10

- PRICE: 151.89 @ 16:48 BST Oct 10

- SUP 1: 150.92 High Sep 26

- SUP 2: 149.96 High

- SUP 3: 149.26 20-day EMA

- SUP 4: 148.23 50-day EMA

Prices were offered sharply into the Friday close, however the underlying bullish trend condition in USDJPY remains intact. This week’s gains reinforce current trend conditions. Price has breached key medium-term resistance at 150.92, the Aug 1 high. The clear break of it confirms a resumption of the bull leg that started Apr 22. Sights are on 154.39, a Fibonacci retracement point. Initial support to watch lies at 150.92, the Aug 1 high.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US PREVIEW: August CPI: Analyst Unrounded Core CPI Range: 0.29-0.36% (3/4)

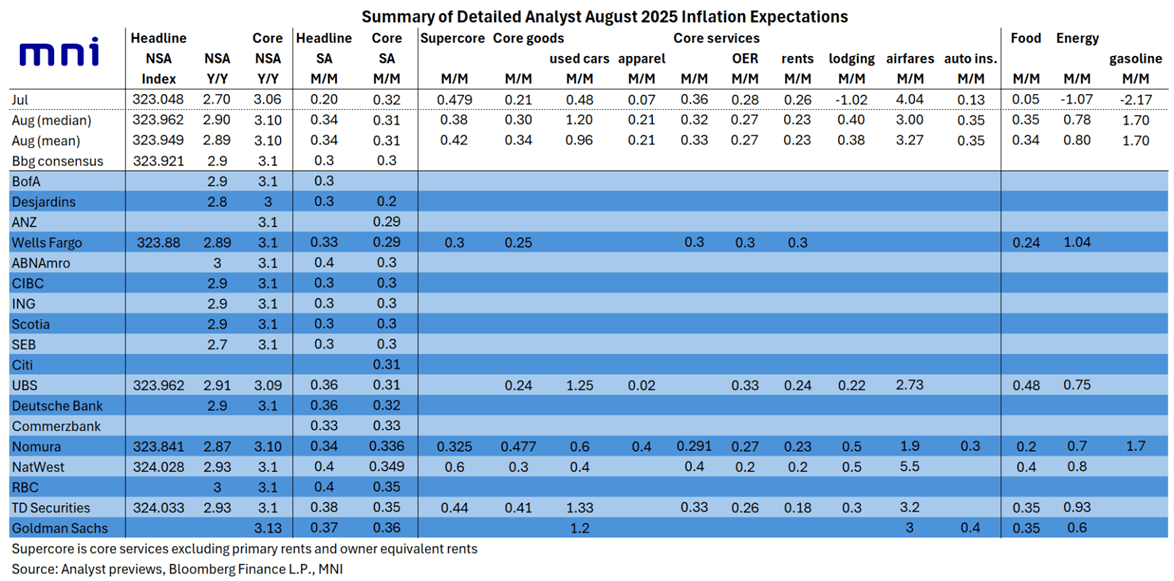

Below is our collation of detailed analyst expectations for the August CPI report, ordered from lowest-to-highest core CPI % M/M expectation.

US PREVIEW: August CPI: Supercore Seen Cooling From July (2/4)

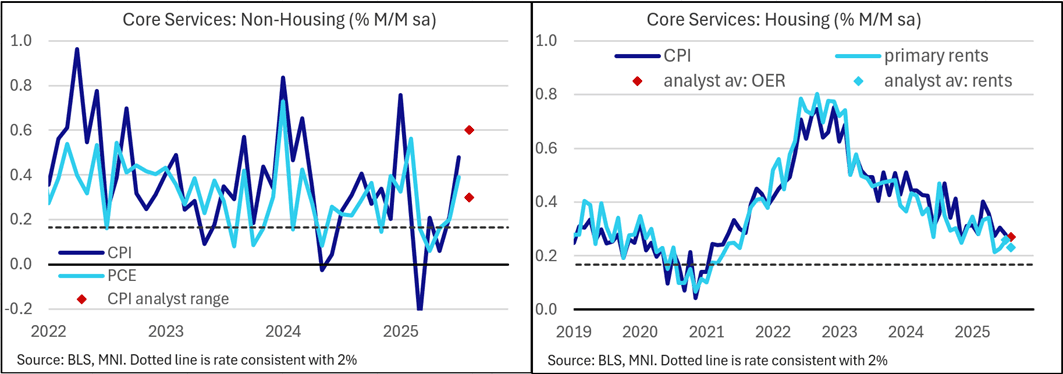

In terms of the category-by-category breakdown, supercore CPI is seen slowing from July's 0.48% (albeit there is a very wide range of views) to around 0.40% with housing CPI seen relatively steady but upside pressure vs July in services areas such as lodging and car insurance (airfares are also seen remaining strong). Outside of the categories below - Medical care printed 0.8% M/M in July, a 34-month high, but this is seen moderating at least somewhat in August.

- And core goods prices are roundly seen higher (had printed a below-expected 0.21% in Jul), with vehicle prices seen driving much of the upside, and tariff-impacted categories like apparel seen by many to accelerate.

- Analyst Expectations Of Key Sequential Drivers:

- Lodging away from home (+ve): After a 5th consecutive monthly contraction (1% M/M decline in July), lodging prices are seen rebounding somewhat (0.4% median).

- Used cars (+ve): Prices here are seen picking up from July’s 0.5% M/M, with some estimates above 1% for the highest print since January. While industry data suggests flat M/M prices, the seasonal adjustment is seen pushing SA CPI higher.

- Airfares* (small -ve): While airfare inflation is seen moderating in August, that’s to a still-robust pace (3%, ranges between 1.9 and 5.5%) from 4.0% in July.

- Apparel (neutral): Limited forecasts for this tariff-sensitive category suggest something similar or slightly higher than the 0.07% M/M seen in July.

- Vehicle insurance* (small +ve): Again, a very slight acceleration is seen for auto insurance (0.3-0.4% from 0.1%).

- Rents (neutral to slight -ve): OER and rents are seen steady or perhaps a little softer in August vs July, with risks seen as largely to the downside amid a perceived secular decline in market rents. OER is seen at around the same 0.28% M/M in August, with rents a few basis points lower from July’s 0.26%.

- Non-core: Food (+ve): Food prices surprised to the downside in July at under 0.1% M/M, but are seen bouncing in June with around 0.3-0.4% M/M gains expected.

- Energy (+ve): A resurgence in gasoline prices in August on a seasonally-adjusted basis is expected to help July’s -1.1% M/M in this category largely reverse, with estimates centering around +0.8% M/M.

US PREVIEW: August CPI: Risks Seen Skewed To Core Tickup To 0.4% M/M (1/4)

Despite coming in softer than expected on the headline reading, the PPI release doesn't appear to have a significant impact on expectations for Thursday's CPI (0830ET) compared with our preview out yesterday - Download PDF Here.

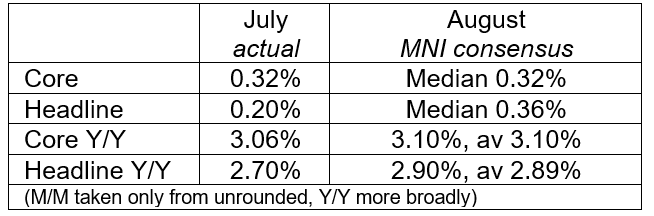

- Consensus (Bloomberg median) is for core CPI to come in at 0.3% M/M rounded in August, same as July (0.32% unrounded).

- Unrounded core CPI expectations suggest a slight skew toward risks of a rounded-up 0.4%, with an unrounded MNI median of 0.32% and range of estimated of 0.29% to 0.36%. That would be steady from 0.32% in July for the joint-highest M/M since January.

- Headline inflation is seen picking up more forcefully, to 0.36% M/M (also would be a post-January high) from 0.20%. The food and energy headline categories are both seen accelerating sharply vs July, resulting in the divergence with the core metric.

- We haven't seen much of a discernable impact on core or headline CPI expectations from the PPI data, whose downside surprise mainly stemmed from weakness in trade services prices (which aren't reflected in CPI).

- Those monthly readings would bring Y/Y core to 3.1% (unch from Jul rounded though a little higher unrounded for a 6-month high), and headline at 2.9% (up from 2.7% prior).

- Recall that the July CPI report saw further acceleration in monthly core inflation but the details defied expectations. The rise was driven by volatile services categories and - in a counter-intuitive finding amid continued tariff concerns - core goods were surprisingly soft (and inflation breadth appeared to moderate). But very strong July PPI data released subsequently, with undertones of businesses passing along higher tariff-related costs to consumers, reversed those dovish cues.