GERMAN DATA: September IP Disappoints Against Expectations

Nov-06 07:22

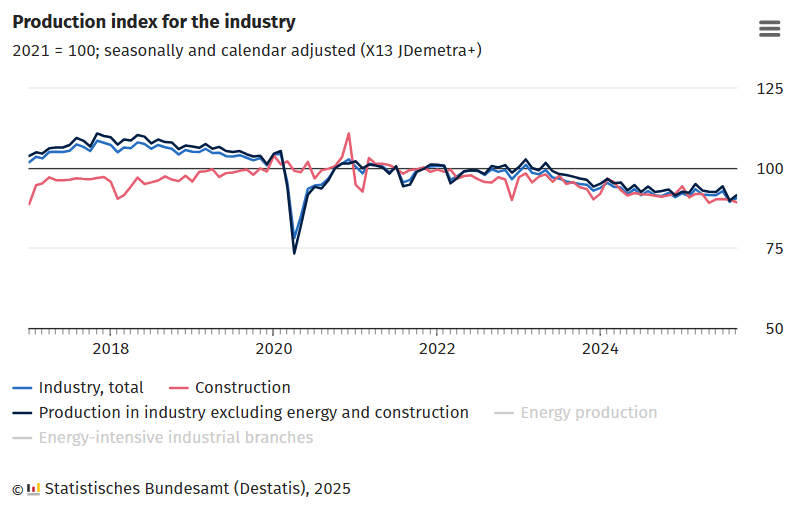

- German industrial production was weaker than expected in September, also when considering an August upward revision, after MNI flagged downside risks to consensus yesterday. "The less volatile three-month on three-month comparison showed that production was 0.8% lower in the 3rd quarter of 2025 than in the 2nd quarter" … "production in industry excluding energy and construction was up 1.9% [M/M]" This means that IP was not able to recover fully from the very weak month of August, with its index continuing to sit close to cycle lows.

- On drivers: A sharp increase was "seen in the automotive industry, Germany's largest industrial branch. Production in this sector was up 12.3% compared with the previous month, following a decline of 16.7% in August 2025 due, for example, to annual plant closures for holidays and production changeovers [note that seasonal factors should have picked up on typical seasonal closures, meaning they will have been more severe than usual]. Production growth in the "manufacture of computer, electronic and optical products" sector (+5.1%) also had a positive effect on overall performance. By contrast, the decrease in the manufacture of machinery and equipment (-1.1%) had a negative impact.", Destatis comments.

- Sentiment in German industry is a little unclear at the moment, with the IFO manufacturing sectoral balance seeing their lowest print since March looking at the current conditions component, while the expectations component of the balance continued trending upwards, almost reaching neutral territory. Expectations improvements have been going on across sectors for a couple of months now, pointing towards a brighter picture ahead, but have not filtered through to the hard data yet. Subdued current conditions indices would suggest that that is not to change imminently.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CROSS ASSET: Higher Yields boost the USDJPY

Oct-07 07:16

- The Push lower in Bonds futures will be supportive of the Dollar and especially the USDJPY, now probing a new intraday high, and eyeing the next big level noted earlier at 150.92.

- There's continued selling interest in Core Bonds and while the Volumes haven't picked up, the lower liquidity means that it takes little order size to move markets.

- US TYZ5 printed a 112.11 low Yesterday, some desks might look for support at 112.06, but better will be seen around 112.03 (4.20% in Yield).

EU-BOND SYNDICATION: 2.75% Dec-32 / New 15-year Dec-40 EU-bond: Books open

Oct-07 07:10

2.75% Dec-32 EU-bond

- Guidance: MS + 36bps area

- Size: E5bln (MNI expected E4-5bln)

New 15-year Dec-2040

- Guidance: MS + 77bps area

- Size: E5bln (MNI expects E5-6bln)

- ISIN: TBC

- Coupon: Long first

- Maturity: 12 December 2040

For both:

- JLMs: BNP Paribas, Citi, Deutsche Bank, DZ BANK and Santander

- Settlement: 14 October 2025 (T+5)

- Timing: Books open, pricing later today

From market source / MNI colour

GOLD: Another Fresh All-Time High Before A Pullback To Little Changed

Oct-07 07:09

Gold has registered another fresh all-time high at $3,977.4/oz today, before a pullback to trade -$5/oz at $3,955/oz at typing.

- Fresh extension higher would target projection resistance ($3,987.3/oz), which protects psychological resistance at $4,000/oz

- Our technical analyst stresses that moving average studies are in a bull-mode setup and price continues to appreciate despite RSI operating in overbought territory since early September. Furthermore, the metal shows little sign of weakness during any pullbacks in spot, underscoring the bullish narrative.

- Geopolitical worry, Fed independence risk, expectations for further Fed easing, ETF & official account demand and broader concerns re: the potential for further USD weakness continue to present the central pillars of the bullish narrative.

- Goldman Sachs have lifted their December ‘26 gold price forecast to $4,900/oz ($4,300/oz prior), suggesting that “inflows driving the 17% rally since August 26 - Western ETF inflows and likely central bank buying - are sticky” in their pricing framework, “in contrast, noisier speculative positioning has remained broadly stable”.

- They also see the risks to their “upgraded gold price forecast as still skewed to the upside on net, because private sector diversification into the relatively small gold market may boost ETF holdings above rates-implied estimates”.

- We will update on broader positioning in the gold market later today.