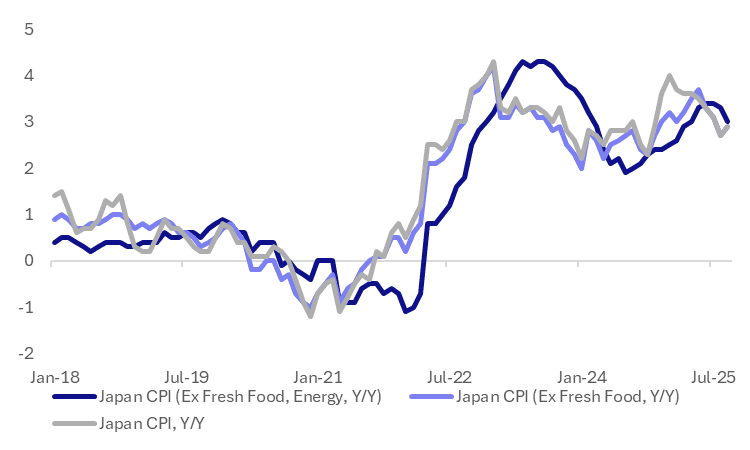

JAPAN DATA: Sep CPI Near Forecasts, Lower Services CPI To Reinforce Steady BOJ

Oct-23 23:55

The Sep Nationwide CPI printed close to market forecasts, while services y/y momentum moderated a touch (to 1.4%y/y, from 1.5%). It's unlikely to change near term BoJ thinking, with next week's policy outcome seen firmly on hold by the sell-side consensus and market pricing. Some BoJ board members continue to argue for a hike but this isn't the core board viewpoint at this stage.

- We were 2.9%y/y for headline and core, which was the consensus estimate. The core measure which excludes fresh food and energy printed at 3.0% (against a 3.1% forecast, with 3.3% prior for this print).

- On m/m terms we were +0.1%, same as Aug, while core m/m outcomes were around flat. Goods prices rose 0.1%m/m, while services were flat. In non-seasonally adjusted terms all headline and core measures were down in m/m terms, the ex food and energy measure off 0.3%.

- By sub-sector, inflation points were evident for fresh food, up 3.2%m/m (after the Aug 3.3% rise), while clothing, footwear surged 2.9%m/m. Negatives were evident though for utilities (-1.3%m/m), entertainment (-2.1%m/m, after a 1.8% gain in Aug), household goods (-0.7%m/m) and transport (-0.2%m/m).

- In y/y terms, only food (+6.7%y/y), transport (+3.0%y/y) and clothing (+2.5%y/y) are above the 2% y/y rate.

- Services prices, which BOJ officials are monitoring closely to assess the strength of the virtuous cycle between wages and prices, rose 1.4% y/y in September after a 1.5% increase in August, per the Tokyo MNI policy team. This reinforces the BoJ's wait and see approach.

Fig 1: Japan CPI - Y/Y, Converging Trends Close to 3%

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Trading To Resume After Yesterday's Holiday

Sep-23 23:20

In post-Tokyo trade on Monday, JGB futures closed stronger, +8 compared to settlement levels.

- US tsys broke a four-day losing streak after Chair Powell did not really throw cold water on rate cut expectations and after Wall Street's winning streak came to an end.

- Fed speak elicited muted reactions. Even Chair Powell's outlook didn't deviate much, if at all, from last week's FOMC press conference, as "two-sided risks mean that there is no risk-free path."

- MNI JAPAN: LDP Candidates Support New Parties In Coalition, No Signal Of Which Ones. Speaking at a joint press conference earlier today, all five candidates for the presidency of the governing Liberal Democratic Party (LDP) voiced their support for the prospect of expanding the governing coalition beyond the LDP and its long-term partner, the centrist social-conservative Komeito party.

- * Bloomberg - "Japan's Takaichi Says More Bond Issuance May Become Unavoidable. Japan will need to rely on excess tax revenue to fight back against rising consumer prices, but issuing government bonds "could become unavoidable if the situation calls for it," said Sanae Takaichi, a frontrunner in the ruling Liberal Democratic Party's leadership race."

- Today, the local calendar will see S&P Global PMIs.

AUSSIE BONDS: Little Changed Ahead Of Aug CPI Due

Sep-23 23:12

ACGBs (YM flat & XM +1.5) are slightly richer.

- US tsys finished modestly richer and near late-session bests, gaining around Chairman Powell's speech as a block buy over 10k TYZ5 added impetus to move.

- Bloomberg - "Australia's Albanese to Meet With Trump in Washington on Oct. 20. "President Trump agreed to a meeting some time ago, we had another chat about it on the phone and we'll have a meeting in Washington DC on Oct. 20," Australian Prime Minister Anthony Albanese said at a press conference in New York."

- Cash ACGBs are ~1bp richer with the AU-US 10-year yield differential at +14bps.

- The bills strip little changed.

- RBA-dated OIS pricing is little changed across meetings today. A 25bp rate cut in September is given a 4% probability, with a cumulative 25bps of easing priced by year-end.

- Today, the local calendar will see August CPI data.

- (Bloomberg Economics) "Australia's August CPI 1-2bps richer report is likely to show inflation holding firm near the top of the Reserve Bank of Australia's 2%-3% target band. We estimate annual CPI growth stayed at 2.8%, unchanged from July. The annual electricity price increase boosted the July reading, but this will be partially unwound by the federal government's subsidy in August."

MNI: UK JUN-AUG BRIGHTMINE MEDIAN PAY AWARDS +3.0% (VS +3.0% MAY-JUL)

Sep-23 23:01

- MNI: UK JUN-AUG BRIGHTMINE MEDIAN PAY AWARDS +3.0% (VS +3.0% MAY-JUL)