OAT: Sell-Side Remain Cautious On OATs

Aug-28 08:54

The latest round of sell-side commentary remains cautious when it comes to the outlook for OATS:

- Commerzbank warn that “OAT/Bunds is likely to test last year's highs near 90bp as the political stalemate could lead to further slippage in the budget consolidation amid pressure to cut the deficit while increasing defence spending, ultimately resulting in downward rating pressure”.

- The Autumn run of French sovereign rating reviews starts on September 12.

- Citi suggest that the toppling of the Bayrou government seems fully priced into OAT/Bunds but warn “a snap legislative election might be needed, which would increase the likelihood of centrists losing control of the government and pension reform reversal. We believe this is partly in the price but would still lead to a widening towards 90-95bp. The key tail risk is a resignation by President Macron, which our economists believe is unlikely but could increase the institutional risk for France and broadly for euro area. This is also the only scenario in which we expect BTP-Bund spread to widen meaningfully from here. Further, these two scenarios could see BTPs trade through OATs”.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: FX OPTION EXPIRY

Jul-29 08:38

Of note:

EURUSD 1.65bn at 1.1650 (a bit far).

USDJPY 1.24bn at 149.00 (wed).

USDCAD 1.7bn at 1.3770/1.3775 (wed).

AUDUSD 1.01bn at 0.6550 (wed).

EURUSD 1.81bn at 1.1600 (thu).

AUDUSD 1.38bn at 0.6600 (thu).

- EURUSD: 1.1500 (629mln), 1.1550 (680mln), 1.1600 (862mln), 1.1650 (1.65bn).

- USDJPY: 148.00 (430mln), 148.50 (317mln), 148.75 (277mln), 149.00 (322mln).

- USDCAD: 1.3715 (365mln), 1.3770 (540mln).

- AUDUSD: 0.6600 (966mln).

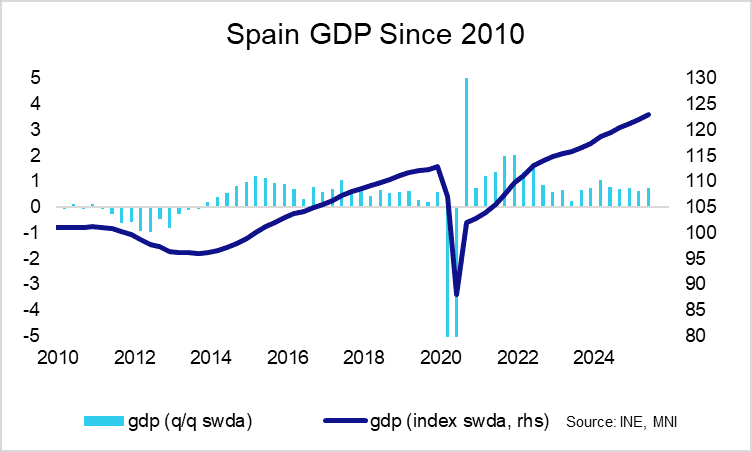

SPAIN DATA: Domestic Demand Fuels Another Strong GDP Print

Jul-29 08:32

Spain continues to cement itself as the post-covid Eurozone growth engine, with Q2 flash GDP growing 0.7% Q/Q (vs 0.6% cons and prior). Sequential growth has been above 0.6% for the last eight quarters.

- Domestic demand was solid in Q1, contributing 0.9pp. External demand was a modest drag to the tune of 0.1pp.

- Household consumption rose 0.8% Q/Q, after slowing a little to 0.5% in Q1. This is consistent with the solid growth in retail sales and improvement in consumer confidence seen through Q2. Meanwhile, Spain’s record low unemployment rate will also be providing a tailwind to consumption.

- Gross fixed capital formation rose 1.6% Q/Q (vs 1.9% prior), while Government consumption was -0.1% Q/Q (vs -0.5% prior). Exports rose 1.1% Q/Q (vs 1.7% prior) while imports grew 1.7% Q/Q (vs 1.5% prior).

- On the production side, industry grew 0.8% Q/Q, while services saw more impressive 1.2% Q/Q growth. The services PMI was in expansionary territory through Q2.

- Hours worked rose 0.3% Q/Q, while real productivity per hour was 0.5% Q/Q. We wrote last week that Increased employment rates, and by extension hours worked, has been a key driver of Spain's economic outperformance post-covid. Importantly, this has also come alongside improving real productivity metrics.

MNI: UK JUN M4 MONEY SUPPLY +0.3% M/M, +3.3% Y/Y

Jul-29 08:30

- MNI: UK JUN M4 MONEY SUPPLY +0.3% M/M, +3.3% Y/Y