CANADA DATA: Sales Figures Point To Softer Activity In August, Led By Autos

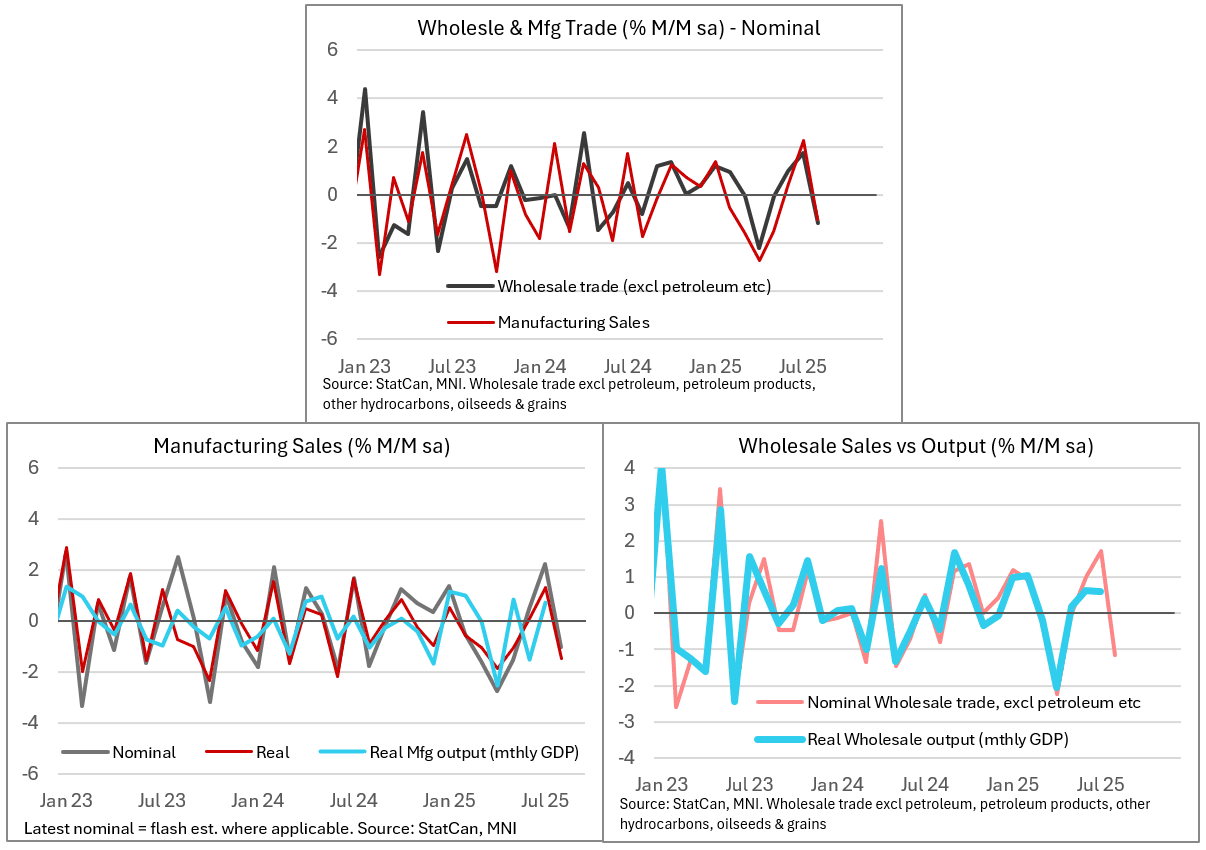

Canadian manufacturing and wholesale sales (Ex-petroleum, products, other hydrocarbons, oilseed & grains) came in slightly better than expected in September, at -1.0% / -1.2% M/M respectively. This compares to the advance estimates of -1.5% for manufacturing (prior rev to 2.2% from 2.5%) and -1.3% for wholesale sales (1.7% prior rev from 1.2%) and despite is suggestive of a drag on August GDP from wholesale and manufacturing output (the August GDP advance estimate is for flat growth M/M overall).

- From a momentum perspective both sales categories appear to be past the worst - but the auto industry appears to remain under duress, with the trade conflict with the US continuing to pose headwinds.

- Looking first at manufacturing sales, the decline nonetheless pared the contraction in the 3M/3M annualized pace to -1.3%, which was a 5th consecutive drop but far better than the -17.6% posted in June that helped drag on Q2 GDP. In volume terms, higher prices meant that the picture was less positive: they fell 1.5% in August, worst in 4 months and erasing the 1.3% rise prior. They're contracting at a 3.4% quarterly pace, with the level of shipments at the lowest since September 2021. Year-to-date through the first 8 months of the year, sales are down 1.0% Y/Y.

- Manufacturing inventories ticked up 0.3% to the highest since November 2023, with the inventories-to-sales ratio remaining relatively steady over the last 4 months at a relatively high 1.75x. StatCan noted lower sales in 12 of 21 subsectors, with the biggest drops coming in the transportation equipment (-5.7%, with motor vehicle parts falling 5.2% and vehicles 3.3% amid "lower than typical seasonal sales of motor vehicle parts as well as production slowdown at a major auto assembly plant in Ontario") and food (-1.9%) subsectors, while primary metal sales increased the most (+3.6%).

- And as for the wholesale data, sales fell in 3 of 7 subsectors, led by motor vehicle parts/accessories (-8.8%). Ex-petroleum, products, other hydrocarbons, oilseed & grains sales rose for the 3rd consecutive month (1.3%) and is rising at a solid 3.9% 3M/3M pace which is a post-April best. In volume terms, gains were firmly negative in the month however (-2.7% M/M), the first drop in 3 months, though the 3M/3M ann rate was still elevated at 6.8%. Overall wholesale sales jumped 7.4% on a 3M/3M annualized basis, which would be the fastest since February, though again that's in nominal terms.

- Inventories-to-sales for ex-petroleum etc picked up to 1.58x from 1.55x prior, which excluding the first 2 months of the pandemic was the highest since at least 2000 - suggesting a building overhand that could depress future activity.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGBS: 10-year BTP/Bund Spread Testing 78bps

The 10-year BTP/Bund spread is testing the 78bps handle, with today’s 2.5bp tightening supported by positive risk sentiment (the S&P 500 index marked a fresh all-time high today, with EStoxx 50 index also up almost 1% intraday).

- The immediate downside target in the spread will be the August 13 close at 76.7bps, after which the 70bp handle will be in focus.

- Alongside the solid risk backdrop, September’s BTP/Bund narrowing has been supported by an ongoing pullback in EUR rates vol and relative political stability in Italy compared to the likes of France.

NORGES BANK: MNI Norges Bank Preview - Sep 2025: Another Close Call

FOR THE FULL PUBLICATION PLEASE USE THE FOLLOWING LINK

EXECUTIVE SUMMARY:

- At the start of the month, analyst and market expectations were fairly comfortably in favour of a 25bp Norges Bank cut on September 18th. However, domestic data released over the past two weeks have made the decision a much closer call.

- We currently lean against consensus in favour of a hold at 4.25% - a risk we thought markets were underappreciating even before the recent run of domestic data.

- If rates are held on Thursday, we expect soft guidance for a 25bp cut in December.

- Whatever the rate decision, the September MPR rate path is expected to be revised higher relative to June, pointing to a higher terminal rate landing zone than the 3.00-3.25% currently implied.

- Although market pricing still tilts in favour of a cut, price action over the past two weeks has clearly been in a hawkish direction. Recent moves, alongside the split analyst consensus, opens the door to a material knee-jerk reaction under any rate decision scenario on Thursday.

AUD: More FX Exchange traded upside Option

AUDUSD (7th Nov) 68.50c, bought for 0.25 in ~3.1k total (multiple clips).