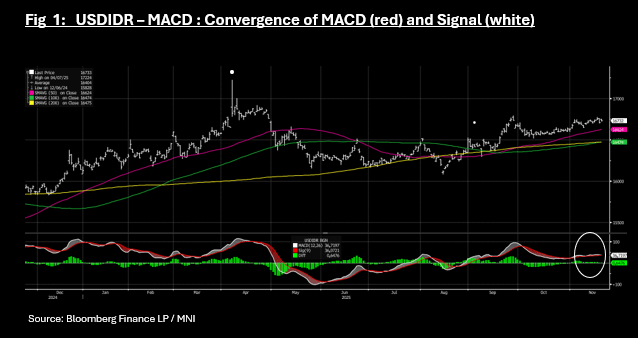

IDR: Rupiah Weakens, Momentum Indicators Suggest No Real Trend

- USDIDR has lost ground today by -0.16% failing to hold onto the modest gains of yesterday.

- The Moving Average Convergence/Divergence indicator (MACD) sees the MACD line and the Signal line has converged over the last 10-days, implying that momentum for the currency pair is limited as it awaits it's next catalyst.

- There appears limited evidence that the BI is intervening in the currency and the decision by the Central Bank to Hold yesterday saw the BI flag currency concerns by global interest rate differentials driving capital flows. This may suggest that the BI has limited room to move for now and may be seen back in the market again soon to help improve the currencies fortunes.

- The Jakarta Composite is up strongly today by +0.84% at 8,480 a new high as bond yields rise modestly.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSTRALIA: Improved Q3 Job Ads May Signal Better Q4 Labour Market

SEEK data show that labour demand improved over Q3 while supply remains positive it slowed. With Q3 employment rising only 0.2% q/q down from Q2’s 0.6%, SEEK job ads may be signalling some possible improvement over Q4. A stabilisation of the labour market would be helpful for monetary policy decision makers if inflation prints to the upside.

Australia SEEK job ads %

- September SEEK new job ads rose 1.1% m/m, the third straight monthly increase. Ads increased 1.7% q/q in Q3 a clear pick up after Q2’s 0.6% q/q contraction. They are still down 2.4% y/y in September but that follows -12.6% y/y in March and is the best result in almost three years.

- Applicants per job were little changed in August rising 0.1% m/m and 10.9% y/y following July’s 2.8% m/m & 11.7% y/y. It seems that growth in labour supply slowed in Q3 after rising 4% q/q in Q2. In Q3, the labour force grew 1.8% y/y while employment was up 1.5% y/y.

- SEEK noted that a number of large industries had increased job ads including trades & services, manufacturing and transport & logistics. Professional and financial services continue to decline.

Australia SEEK applicants per job 2013=100

Source: MNI - Market News/SEEK

JGBS: Modestly Richer, Oct 30 BOJ Hike At 25% Chance

JGB futures are stronger, +16 compared to the settlement levels, but off session bests.

- Cash US tsys are slightly mixed, with a flattening bias, in today’s Asia-Pac session after yesterday's gains.

- Cash JGBs are slightly richer across benchmarks, with yields 1-2bps lower. The benchmark 10-year yield is 1.0bp lower at 1.664%, outperforming the futures-linked 7-year. This continued the recent trend, which has unwound the relative cheapening of the 10-year earlier in the year.

- Japan sold ¥300bn of 10-year climate transition notes at a cut-off yield that was lower than expectations, signalling lacklustre investor demand. The cut-off yield was 1.680%, compared with 1.695% estimated by traders in a Bloomberg survey. The bid-to-cover ratio was 3.56x, compared with 3.31x in October 2024, the last time the government sold the bonds.

- Swap rates are little changed.

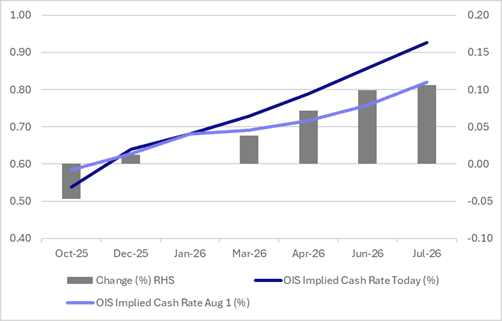

- BOJ-dated OIS pricing is little changed across 2025 meetings compared to early August levels. Pricing is, however, firmer for 2026 meetings out to July. Current OIS pricing implies just a 24% probability of a 25bp hike in October, rising to 65% by December and 82% by January. A full 25bps hike is not fully priced until March 2026. (see chart)

- Tomorrow, the local calendar will see Trade Balance data.

Figure 1: BOJ-Dated OIS – Today Vs. August 1

Source: Bloomberg Finance LP / MNI

US TSYS: Treasuries Trend Sideways in Lacklustre Trading Day

Having finished the overnight US session modestly higher, US Treasury futures failed to follow on with TYZ5 remaining where it opened at 113-19 and USTs moves modest at best.

- The US 2-Yr did very little during the Asian trading day, trending marginally higher to 3.46%

- The US 5-Yr had finished -2bps lower at 3.57% during the US trading day where it remained.

- The US 10-Yr slipped back below the 4.00% overnight, finishing at 3.98% where it has held during the day today with eyes on it overnight to see if it can consolidate below 4.00%.

- The USD 30-Yr was strong overnight rallying 3bps to 4.57%, and continued on in Asia down again to 4.56% The 30-Yr is now back at levels of April.

The key data releases tonight are the Philadelphia Fed Non-Manufacturing Activity, Redbook retail sales and MBA Mortgage Applications.