AUSSIE BONDS: Risk-Off Buoys Bonds Ahead Of US CPI Today, May-30 Supply Due

ACGBs (YM +6.5 & XM +8.0) are stronger after US tsy yields finished 5-8bps lower, indeed the best le...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

NEW ZEALAND: Filled Jobs Best M/M Rise Since Late 2023, But Still Down Y/Y

New Zealand filled jobs rose 0.3%m/m in Nov last year after a revised -0.1% outcome for Oct (originally reported as flat). Nov's rise was the best m/m gain since Oct 2023. This signifies some progress in better jobs growth momentum, although it follows a long period of softer momentum through much of 2024 and 2025. In y/y terns, jobs filled were still down 0.4%. The data, along with a rise in building permits, should add to the sense of improved economic momentum for NZ in 2026, suggesting an early wait and see approach for the RBNZ. Note we get Q4 2025 inflation next week on Friday.

- By industry, Stats NZ noted the following outcomes in y/y terms - "construction – down 3.6 percent, health care and social assistance – up 1.8 percent, professional, scientific, and technical services – down 2.2 percent, manufacturing – down 1.6 percent, public administration and safety – up 2.1 percent."

- Hence a lot of the job creation is in the services side rather than goods producing/manufacturing.

- Earlier, Westpac noted: "Employment confidence rose by 3.9 points to 93.8 in the December quarter. Jobs are still seen as hard to come by, but current readings are consistent with a peak in the unemployment rate."

- Other data showed a 2.8%m/m in building permits for Nov. This comes after a revised 0.7%m/m fall for Oct. We up 7% in y/y terms, but in levels terms we are still comfortably under 2022 highs.

BONDS: NZGBS: This Week's Sell-Off Extends After Constructive Data

NZGBs are 2-3bps cheaper, extending this week’s weakness, despite US tsys finishing little changed. Today’s data has had a positive tone, building on yesterday’s constructive Q4 QSBO survey results.

- NZ’s home-building approvals rose 2.8% m/m in November versus revised -0.7% in October. NZ filled jobs rose by 6,569 or 0.3% m/m in November from October.

- (Bloomberg) “NZ Employment confidence index rose 3.9 points to 93.8 in 4q, Westpac Banking Corp. and McDermott Miller Ltd. say in emailed statement. Highest since early 2024 but remains below 100 which indicates households have a pessimistic view of the labour market.”

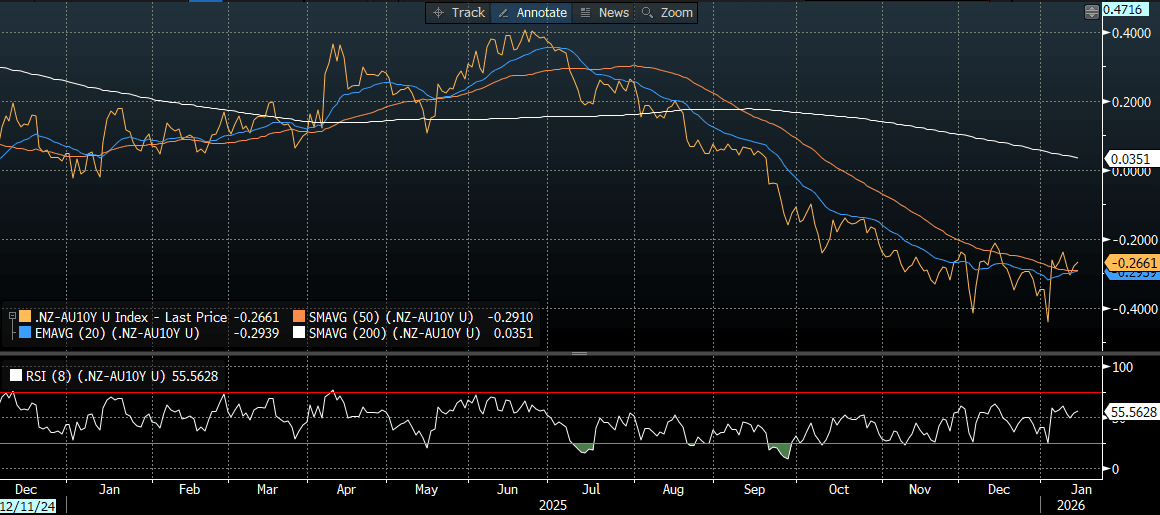

- NZGBS are underperforming the $-bloc, with the NZ-US and NZ-AU 10-year yield differentials 2-3bps wider (see chart).

- Notably, OIS markets are now pricing no change in the NZ-AU official cash rate differential by year-end. This is consistent with our Economics team's central view. As a result, the near-term outlook for the NZ-AU 10-year yield differential points to relative stability rather than further material moves.

- RBNZ-dated OIS pricing is little changed across meetings. No tightening is priced for February, while October 2026 assigns 23bps.

- Swap rates are 1-2bps higher.

- On Thursday, the NZ Treasury plans to sell NZ$250 Million 4.5% 2035 bond, NZ$200 Million 4.5% 2030 bond and NZ$25 Million 3.25% 2050 Linkers.

Bloomberg Finance LP

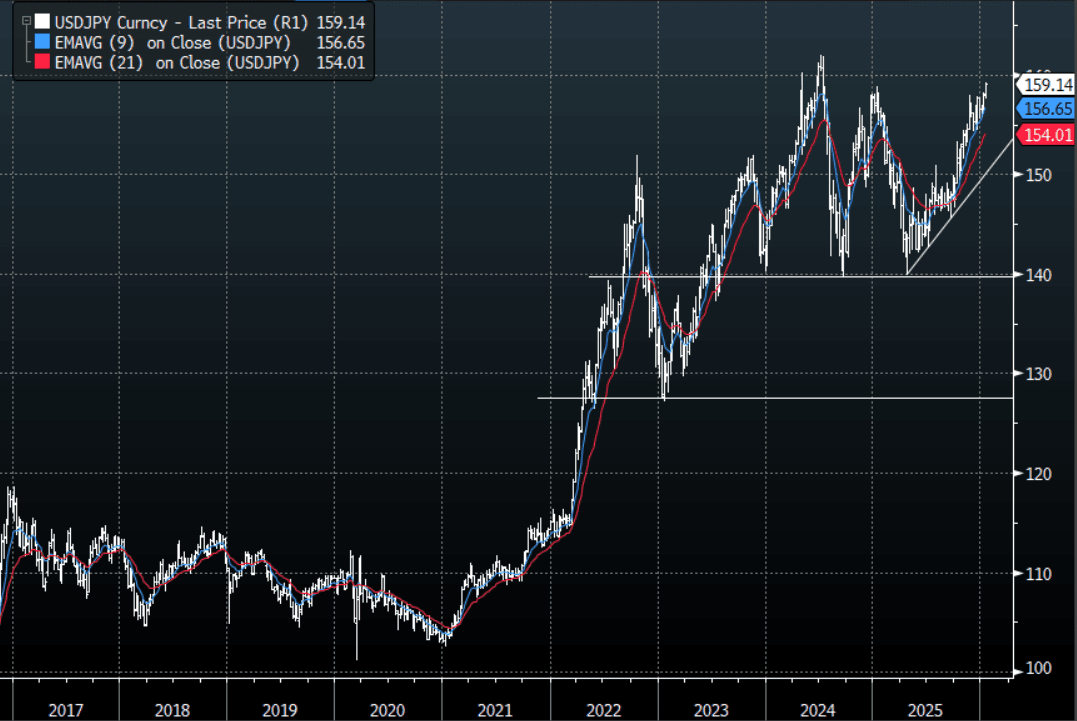

JPY: USD/JPY - Marches On Toward 160.00, Decent Optionality Ahead

The overnight range was 158.60 - 159.19, Asia is currently trading around {USDJPY Curncy}. USD/JPY continues its relentless march higher. The BOJ is in a tough spot, and they are going to need to do something significant to turn around the market's perception of a weak Yen. A test of the BOJ/MOF resolve looks inevitable at the moment as the market moves its focus toward the important 160.00 area. In today's Asian session, first support is back toward 158.50 and then the 157.50-158.00 area as dips continue to be supported. It's almost a case of when not if we get intervention now. In my experience though they tend to come in a lot later than most expect so would not be surprised to see new highs above 162.00 before we start seeing them get involved. Until then it's tough to see what turns this ship around, looks like some decent optionality around 160.00 coming up which might see it chop some wood first.

- MNI INTERVIEW: Musalem Warns Easy Fed Policy 'Unadvisable'. Further U.S. interest rate cuts would bring monetary policy to an "unnecessary and unadvisable" accommodative stance given strong consumer demand, rising non-labor costs and the impact of tariffs and energy prices, Federal Reserve Bank of St. Louis President Alberto Musalem told MNI on Tuesday. {NSN T8T8X66QRTHD <GO>}

- Bloomberg - “It’s Hard to Know How Seriously to Take the CPI Report. At this point it’s kind of hard to know what to make of all of this, and of course the y/y readings are hopelessly compromised by the absence of detailed figures for November. On reflection the market seems to be coming around to the notion that insights from this report are relatively limited.” - Cameron Crise.

- Options : Close significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 158.00($1.9b Jan 16), 160.00($4.25b Jan 16) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 89 Points

- Data/Event : Money Stock M2/M3, Machine Tool Orders YoY

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P