MNI US Employment Insight: Strong NFP Report Delays Rate Cuts

Feb-12 17:24By: Chris Harrison and 1 more...

Employment+ 4

Download Full Report Here

The BLS nonfarm payrolls report for January was far stronger than expected, going against various alternative indicators that either surprised lower or were outright soft in the past two weeks.

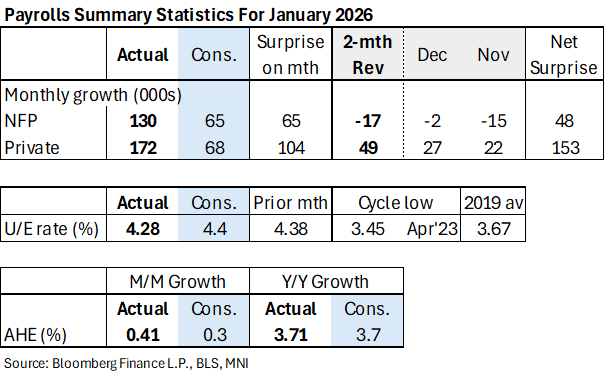

- Nonfarm payrolls rose 130k (sa, cons 65k) after negligible two-month revisions of -17k (mainly in Nov).

- Private payrolls saw a larger beat at 172k (sa, 68k cons) and a two-month revision of +49k. A little of that gloss was taken off by particularly strong 124k rise from health & social assistance, a cyclically insensitive category that has been a lifeline for private sector job creation.

- The benchmark revision saw cumulative payrolls growth revised down by -862k in NSA terms (-898k SA) over the twelve months to March 2025, its largest downward and absolute revision in recent history.

- That was towards the more negative end of expectations but within a margin of error. Still, private sector ex health & social assistance payrolls are now estimated to have declined by a heavy -326k across 2025 (and that’s with the benchmark revision only going to March) vs an already tepid 20k increase previously.

- Sticking with NSA details, nonfarm payrolls ‘only’ fell by -2.65mln in January after -2.91mln in Jan 2025 (revised from -2.83mln due to the benchmark revision) and -2.89mln in Jan 2024.

- The Household Survey was anticipated to provide a cleaner read on current labor market conditions in January than the much-revised Establishment Survey, but whether it accomplished that is questionable.

- There were clearly strong signs, such as the unemployment rate of 4.283% not just below the consensus of 4.4% and 4.375% prior, but also the lowest since July. However, a response rate of 64.3% is the 3rd lowest in history, with only the prior 2 surveys having been lower. Unlike the Establishment survey, the BLS notes, "The severe weather did impact the collection of household survey data", and that is reason enough to take the results with a grain of salt.

- The release drove a sizeable front-loaded hawkish reaction after a firmly dovish build-up following the previous week’s slew of weak labor indicators (all reviewed below) and more recently Trump administration comments ahead of the release plus weak retail sales data.

- A next Fed 25bp cut has tilted back to being fully priced for July rather than June whilst a second 25bp cut is still fully priced for December.

- It also spurred multiple analyst view changes, eyeing later cuts or none at all, including from CIBC, Citi, Commerzbank, ING, Natixis, TD Securities and Wells Fargo.

- Initial Fedspeak has stuck to previously drawn lines: hawks Hammack and Schmid welcomed the report and don’t support near-term rate cuts whilst outright dove Governor Miran still sees many reasons to cut.

- Market attention immediately turns to January CPI on Friday but with another round of February NFP and CPI reports due before the next FOMC meeting on March 17-18.