BOJ: Rinban Purchase Offer

The BoJ offers to buy a total of Y1135bn of JGBs from the market:

- Y325bn worth of JGBs with 1-3 Years until maturity

- Y325bn worth of JGBs with 3-5 Years until maturity

- Y350bn worth of JGBs with 5-10 Years until maturity

- Y135bn worth of JGBs with 10-25 Years until maturity

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Cash Bonds Little Changed

In Tokyo morning trade, JGB futures are little changed, -1 compared to settlement levels, after giving up Friday’s overnight gains.

- (Bloomberg) -- Bank of Japan Governor Kazuo Ueda said he expects a tight labor market to keep upward pressure on wages, reflecting his view that stable inflation is set to take hold.

- “Wage growth is spreading from large enterprises to small and medium enterprises,” Ueda said Saturday in remarks at the Federal Reserve’s annual symposium in Jackson Hole, Wyoming. “Barring a major negative demand shock, the labor market is expected to remain tight and continue to exert upward pressure on wages.”

- Cash US tsys are ~1bp cheaper in today’s Asia-Pac session after Friday’s strong rally.

- Cash JGBs are little changed across benchmarks. The benchmark 10-year yield is 0.6bp lower at 1.618% versus the cycle high of 1.627%, set last week.

- Swap rates are 1-2bps higher. Swap spreads are wider.

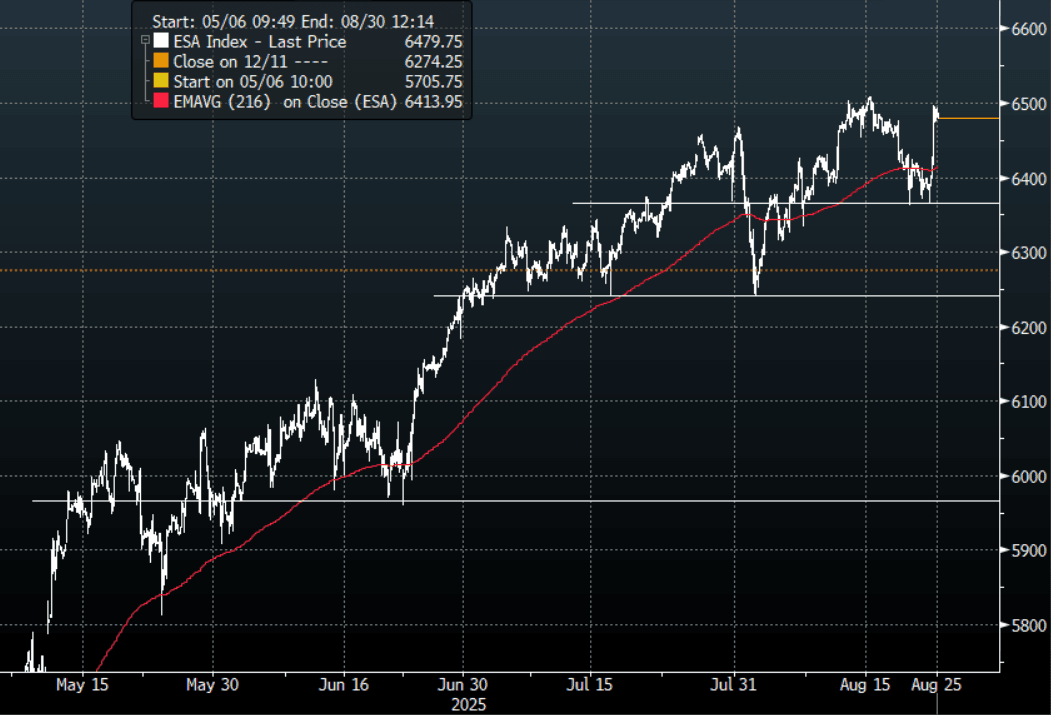

US STOCKS: A Dovish Interpretation Of Powell Speech Sees Stocks Surge Higher

The ESU5 overnight range was 6364.00 - 6496.25 closing +1.52%, Asia is currently trading around 6480. The ESU5 contract exploded higher in the Friday N/Y session as the market reacted to what it interpreted to be a very dovish speech. The sectors of the market most sensitive to rate changes had huge reactions Russell Index +3.86%, Regional Banks +4.81%. There is some debate regarding whether 2% inflation is still the Fed’s target or are they abandoning the idea of ever reaching that to run the economy hot. Regardless the market quickly reversed course from looking about to correct lower to testing all-time highs once more.

- Ben Hunt on X: “Powell explicitly abandoned the idea of *achieving* a 2% inflation rate in this cycle and “reaffirmed” 2% only as a long-term aspirational goal as measured by long-term inflation expectations anchored (whatever that means) at 2%. This is PROFOUNDLY dovish and is ABSOLUTELY a verbal abandonment of the 2% target. For the past 3 years, Powell has said that 2% inflation was not aspirational and not something to get close to, but something to actually achieve. That language is now gone. We will not see 2% in this cycle. This is profoundly dovish.”

- Lance Roberts on X: “Economic Slowdown Poses A Risk To Earnings. As noted by Jerome Powell this morning, the economic backdrop continues to weaken. While it increases the likelihood of a rate cut, the risk to ebullient earnings forecasts are a more significant concern.”

- (Bloomberg) - Nvidia earnings will take center stage in the coming week after a slew of Wall Street analysts lifted their expectations for the chipmaker’s stock.

Fig 1: SPX(ESU5) 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

CHINA: Week Ahead: Macro, Valuations, Technicals, Sentiment, Politics

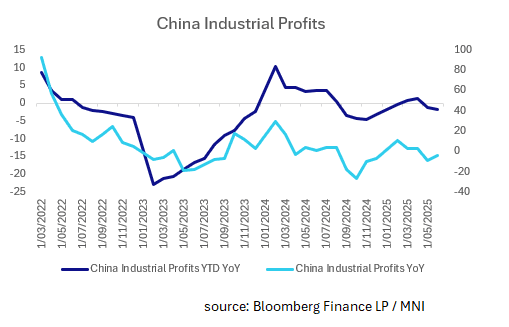

Macro: Last week was a data light week in China with the Loan Prime Rates a non-event with no change as expected, as Chinese banks face sustained pressure on net interest margin and return on equity that could last beyond 2026. FDI reported late Friday and was again very weak. This week on the data front will be Industrial Profits on Wednesday, followed by Official PMIs over the weekend. Official Manufacturing PMIs have contracted the last for the last four months whilst the Services PMI has barely kept expanding. Trends are likely to remain the same with the July release. Industrial Profits since mid-2024 has struggled with contraction. Industrial profits are weighed down by slow demand, poor consumer and investor confidence and ongoing deflationary pressures all of which are expected to continue.

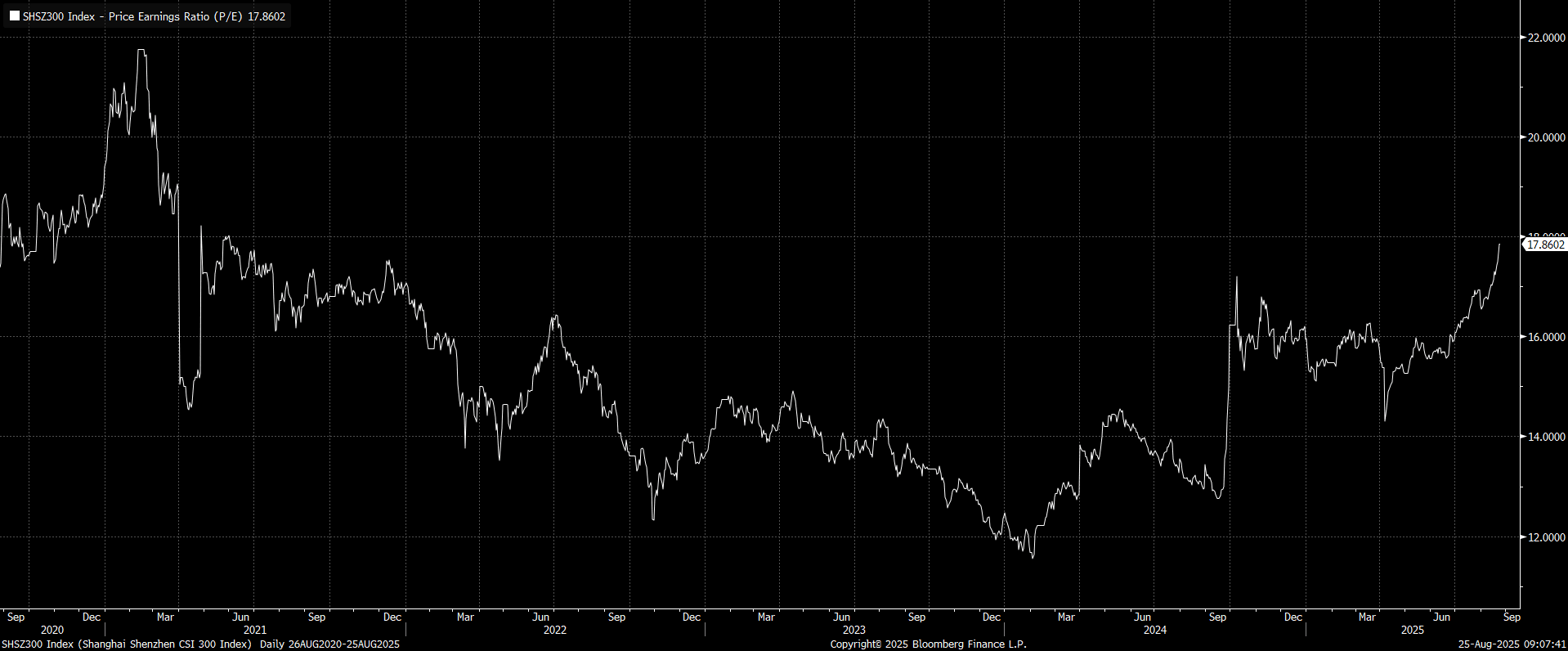

Valuations: USD/CNY versus the USD/CNY fixing shows the fixing is at fresh lows back to Nov last year, but USD/CNY spot is still comfortably above 2025 lows (near 7.1490). Likewise USD/CNH remains comfortably above 2025 YTD lows, tracking familiar ranges above 7.1700 in latest dealings. The CSI 300 P/E has run up over the last few weeks. If you take out the post COVID jump / stimulatory led jump of early 2021, the current P/E on the CSI 300 is nearing the highs.

Fig1: CSI 300 Price to Earnings Last Five Years

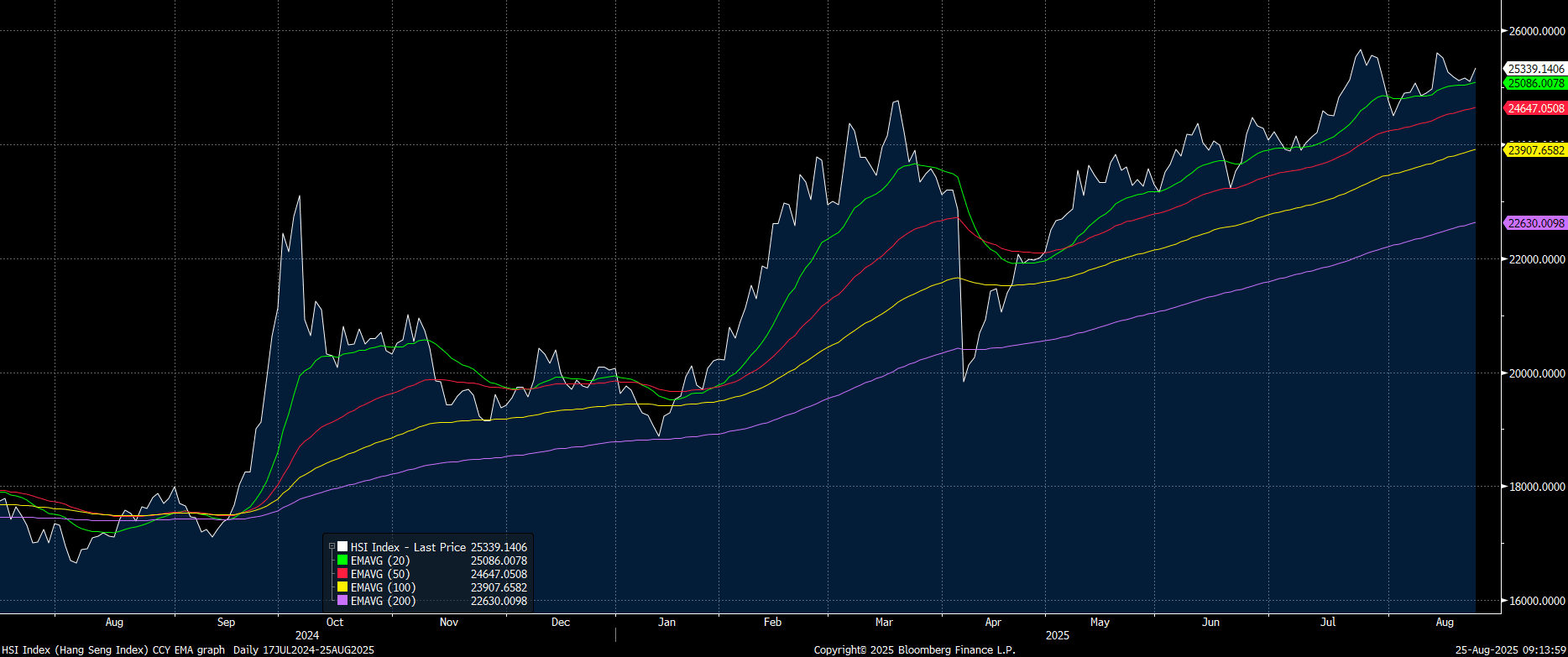

Technicals: The technicals for local bonds remains very strong. Last week's daily OMO resulted in over CNY1.3bn of liquidity injection which our analysis suggests remains a strong technical for bond demand. For the major bourses, they are all trading above major moving averages. The laggard is the Hang Seng which with Friday's gains, bounced off the 20-day EMA. Relative to the other major bourses (which trade materially higher than the 20-day EMA), this suggests that the Hang Seng could play catch up should the week ahead be positive for equities.

Figure 2: Hang Seng Index vs 20, 50, 100 and 200 Daily Moving Averages

Sentiment: Whilst the economic data shows a sluggish economy, the stock market says otherwise as investors, with little alternative, buy equities. Earnings have been eroded by deflationary pressures, poor consumer sentiment yet the belief that further stimulatory measures may be forthcoming and that the economy has potentially upside potential, has over ridden this.

Geopolitics: Russian, Indian and China's leaders will converge in Tianjin for the Shanghai Cooperation Organization summit this week, among leaders from over 20 countries and heads of 10 international organizations coming together to address urgent regional and global issues. The Kremlin is pressing for a long-awaited trilateral meeting in an attempt to revive the Russia/India/China alliance as a counter to the US Trade War. If it did find new life, it would send a powerful signal that the geopolitical heavyweights are aligning in the face of US pressure. However, long held tensions between India and China, and economic differences between the three, make that outcome unlikely.