CANADA DATA: Retail Sales Rebound In November, But Set To Post A Flat 2025

Jan-23 14:23

Retail sales look to have ended 2025 on a mixed-at-best note, with Canadian retail consumer activity...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SOFR OPTIONS: Early Midcurves

Dec-24 14:06

- +2,000 0QH6 96.62/96.75/96.87 call flys, 2.0 ref 96.83

- +1,000 0QF6 96.62/97.06 strangles, 2.75

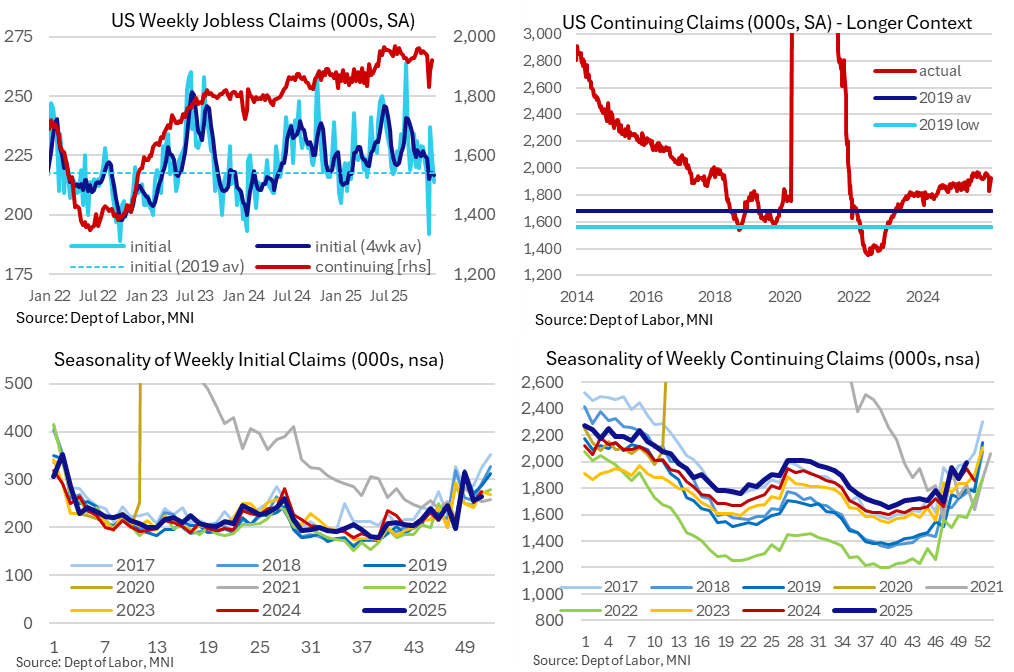

US DATA: Jobless Claims See Decent NFP Reference Period Comparisons

Dec-24 13:49

Initial claims surprised lower, leaving the four-week average on par with 2019 levels when the u/e rate averaged 3.7%. Of course, re-hiring is slower now with continuing claims more consistent with a period when the u/e rate averaged 4.4%. That’s a little better than the 4.56% in latest data for November although the two are closer when considering NY Fed’s Williams estimates the latter was lifted by ~0.1pp on technical distortions. On balance, the claims data go against consumer surveys pointing to a further deterioration in the labor market.

- Initial claims were lower than expected at 214k (sa, cons 224k) in the week to Dec 20 after an unrevised 224k (initial 224k).

- The four-week moving average dipped 1k to 217k, including the exceptionally low 192k in late Nov but also the subsequent bounce to 237k as it struggled with the seasonal adjustment around Thanksgiving (the Christmas period can also see distortions but they tend to be less severe).

- This is a very low rolling level, on par with the 218k averaged in 2019, a period when the u/e rate averaged 3.7% as opposed to the 4.56% in Nov 2025 although hiring is also much slower so this isn’t a fair comparison – see below.

- The 224k in the December reference period compares with 222k for Nov, 231k for Oct, 232k for Sep and 234k for Aug.

- Continuing claims meanwhile were higher than expected at 1923k (sa, cons 1900k) in the week to Dec 13 after a downward revised 18885k (initial 1897k), but with the upside likely to be reduced after presumably yet another downward revision next week.

- For now, this 1923k still compares favorably to the 1944k in Nov, 1957k in Oct, 1916k in Sep and 1944k in Aug.

- Continuing claims have seen cycle highs of in the 1960k’s in June, July, Aug and late Oct but haven’t broken above this (again, after revisions), implying a deterioration hiring conditions ahead of the summer but one that has since stabilized.

- Whilst initial claims are running at a level previously consistent with an u/e rate in the 3s, continuing claims are running closer to the 2017 average when the u/e rate averaged 4.36% (in a year when it started at 4.7% and ended at 4.1%).

SOFR OPTIONS: Jun'26 SOFR Call Spread Sale

Dec-24 13:46

- -5,000 SFRM6 96.62/97.00 call spds, 9.5 vs. 96.655/0.30%