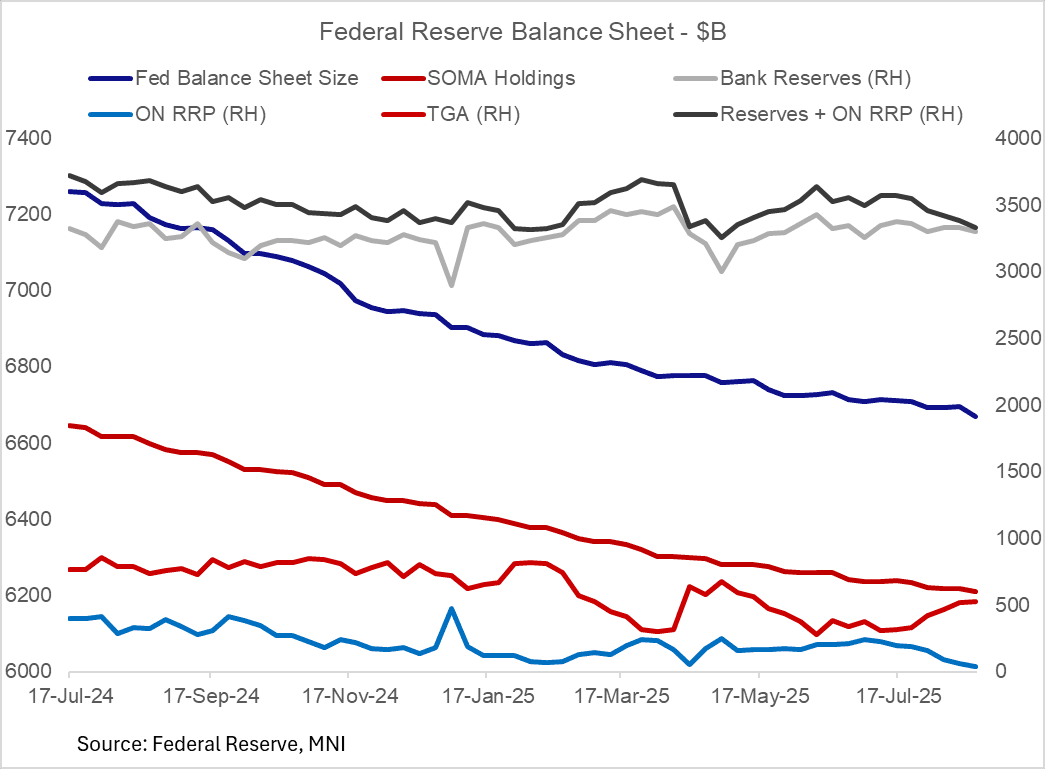

FED: Reserves + ON RRP Fall To Late April Levels As Treasury Cash Builds (1/2)

Aug-21 20:39

Reserves fell slightly in the week to Wednesday Aug 20, per the Federal Reserve's latest H.4.1. release.

- At $3.30T (vs $3.33T prior), reserves fell to the lowest weekly level since July 2. Meanwhile, takeup of the overnight reverse repo facility fell to $35B from $57B (in the week it fell to the lowest levels since April 2021). Over the last 4 weeks, reserves and dealer ON RRP have fallen by a combined $211B to the lowest combined level since late April - while the US Treasury General Account has risen by $193B.

- This dynamic is expected to continue into September as the TGA target is another $330B higher, implying reserves could fall to below $3T.

- The minutes to the July FOMC meeting showed the Committee discussed the likely reserve drawdown ahead as the Treasury rebuilt its cash pile after the debt limit was lifted in early July. The minutes suggested that the FOMC was comfortable with the situation even if reserves could be headed into "ample" from the current "abundant" territory. The minutes suggest that while there may be some temporary acute liquidity issues, particularly around quarter-end, they can be resolved by takeup of the standing repo facility (SRF), as opposed to warranting more major changes (such as slowing/halting balance sheet runoff).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ECB: HSBC See ECB Reserving Rate Action For Significant Shocks

Jul-22 20:17

- HSBC think the ECB is unlikely to change its deposit rate of 2.0% at the July 24 meeting, aligning with its strategy to reserve action for significant economic shocks.

- “There shouldn’t be any change in July, with no need to head back from the beach (if you left early).”

- Recent euro appreciation and potential US tariffs on EU goods could lower inflation forecasts, but the ECB is expected to wait until September to assess their impact.

- Policymakers are cautious about overreacting to currency volatility, focusing instead on domestic risks like sticky services inflation and corporate margin pressures.

- The ECB's current stance reflects confidence in the eurozone's resilience, supported by fiscal policy and stable consumption trends.

- HSBC are one of the five analysts amongst the twenty nine reviewed in the MNI ECB Preview who look for no further cuts from the current deposit rate of 2.00% (see in full here).

USDCAD TECHS: Key Short-Term Resistance Intact For Now

Jul-22 20:00

- RES 4: 1.3920 High May 21

- RES 3: 1.3862 High May 29

- RES 2: 1.3798 High Jun 23

- RES 1: 1.3744/74 50-day EMA / High Jul 17

- PRICE: 1.3640 @ 16:03 BST Jul 22

- SUP 1: 1.3631/3557 Low Jul 22 / 03

- SUP 2: 1.3540 Low Jun 16 and the bear trigger

- SUP 3: 1.3503 1.618 proj of the Feb 3 - 14 - Mar 4 price swing

- SUP 4: 1.3473 Low Oct 2 2024

Resistance in USDCAD at 1.3744, the 50-day EMA, remains intact for now. It has been pierced, however, a clear break of it is required to highlight a possible stronger short-term reversal. This would open 1.3798 initially, the Jun 23 high. For now, a bear trend remains in place. A resumption of weakness would refocus attention on key support at 1.3540, the Jun 16 low. Clearance of this level would confirm a resumption of the downtrend.

US TSYS: Tsys Back at July 10 Lvls, Philly Fed Non-Mfg Improves, Costs Elevated

Jul-22 19:57

- Treasuries bounced off early Tuesday lows, initially tracking a similar move in German Bunds - before settling into a narrow range near session highs since midmorning.

- The US$ resumed its weakening trend on Tuesday, extending the pullback from last week’s highs to ~1.6% in recent trade, further eroding the cautious recovery that had been seen across the first half of July.

- Tsy Sep'25 10Y futures are +7 at 111-13 after the bell vs. -14.5 high, briefly through resistance at 111-13+, the Jul 10 high. A clear break of this hurdle would highlight a stronger reversal. Key support lies at 110-08+, the low on Jul 14 and 16. A move through this support would reinstate the recent bearish theme.

- The Philadelphia Fed's Nonmanufacturing Business Outlook Survey continued to show improvement in July, though cost pressures remained elevated. The regional current general activity index rose to a 6-month high -10.3 from -25.0 prior. This was the 3rd consecutive improvement since bottoming at -42.7 in April amid tariff policy concerns.

- The Johnson Redbook Retail Sales Index continues to post solid gains, rising 5.1% Y/Y in the week ending Jul 19, fairly steady compared with 5.2% the prior week.

- Look ahead: Wednesday's data limited to MBA Mortgage Applications at 0700ET, Existing Home Sales follow at 1000ET.

Trending Top

Jan-30 21:43

Jan-30 21:11