CANADA: Q2 GDP Widely Seen Contracting, July Flash Estimates Eyed (1/2)

Friday's GDP release (0830ET) is expected to show a sharp contraction in Q2, albeit with a modest uptick in June GDP (by industry). Current Bloomberg analyst consensus shows Q2 is expected to show a 0.7% Q/Q annualized contraction, versus +2.2% in Q1, with our collation of sell-side views showing a -0.8% to 0.0% range; June GDP is seen roughly confirming the flash estimate at +0.1% M/M (after -0.1% in May). Flash estimates for July will be a key focus.

- The private sector consensus for Q2 is more optimistic than the Bank of Canada's -1.5% estimate in its July Monetary Policy Report, and indeed the data we've seen so far for the quarter suggests that the BoC is too pessimistic. Nonetheless, looking at the component-by-component breakdown, both the monthly data, most analysts, and the BOC itself have the same expectation for direction if not magnitude:

- On the negative side: expectations are for a softening in household consumption growth (+1.2% in Q1); continued weakness in fixed investment (-3.0% in Q1) though with residential outperforming business capital formation.

- On the positive side: expectations are for a pickup in government spending, and more importantly, a reversal of Q2's positive contribution from net exports.

- In short, the data are expected to confirm that trade activity was brought forward to Q1 ahead of tariffs, with the effects reversing in Q2.

- Going forward, the BOC envisages growth resuming in Q3 (+1.0% in its "current tariff" scenario). In the meantime, a weak Q2 reading could provide Governing Council with more conviction to resume easing rates in September, with the July meeting decision noting "If a weakening economy puts further downward pressure on inflation and the upward price pressures from the trade disruptions are contained, there may be a need for a reduction in the policy interest rate".

Some sell-side views in order of most negative to most positive on Q2 GDP, including any mention of July flash GDP (most analysts eye the 0.1% flash estimate being confirmed for June, or 0.2%):

- CIBC (-0.8% Q/Q): "The economy likely contracted modestly in Q2, with exports slumping due to US tariffs and following the frontrunning activity that bolstered trade in the first quarter of the year. However, final domestic demand may have returned to growth following a flat reading in the first quarter, probably led by government spending...The contraction in GDP during Q2 may not be quite as bad as forecast by the Bank of Canada ... but it would still be consistent with slack building up in the economy. That, combined with recent tamer readings for Canadian inflation recently, should provide policymakers enough comfort to restart interest rate cuts at the September meeting. "

- TD (-0.8% in Q2): "large drag from net exports, unwinding some of their positive contributions from Q1. Domestic demand should remain downbeat even with goods consumption offering a source of strength, as residential and non-residential investment are set to contract further on heightened trade uncertainty and softer construction/resale activity. Government spending will provide another key source of strength, helping to offset the drag from investment and net exports.... We also look for new flash estimates to land on the softer side with GDP projected to remain unchanged in July, which pour some cold water on any discussions of a Q3 rebound"

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Pierces The 50-Day EMA

- RES 4: 1.4016 High May 12 / 13

- RES 3: 1.3920 High May 21

- RES 2: 1.3862 High May 29

- RES 1: 1.3798 High Jun 23 and a key near-term resistance

- PRICE: 1.3771 @ 19:05 BST Jul 29

- SUP 1: 1.3679/3557 20-day EMA / Low Jul 03

- SUP 2: 1.3540 Low Jun 16 and the bear trigger

- SUP 3: 1.3503 1.618 proj of the Feb 3 - 14 - Mar 4 price swing

- SUP 4: 1.3473 Low Oct 2 2024

A short-term correction in USDCAD remains in play. However, note that price has traded through the 50-day EMA at 1.3728. A clear breach of this average would highlight a stronger short-term reversal, exposing 1.3798, the Jun 23 high. Clearance of 1.3798 would strengthen a bullish condition. On the downside, 1.3540, the Jun 16 low, marks key support. A break of this level would resume the downtrend.

US TSYS: Treasuries Bid Ahead FOMC, Strong 7Y Sale, JOLTS Jobs Recede

- Treasuries look to finish near late session highs, TYU futures back at last week's highs on July 22 as markets consolidate ahead of tomorrow's FOMC rate annc.

- A strong 7Y note auction helped rates extend highs after the $44B note sale (91282CNR8) stopped through again: 4.092% high yield vs. WI of 4.120%; bid-to-cover 2.79x from 2.46x prior. Peripheral stats: Indirect take-up retreats to 62.26% vs. 76.74% prior; Direct take-up climbed to new high at 33.68% vs. 11.62% prior; Dealers fell to new low of 4.06% vs. 11.64% prior.

- First half support: Tsys extended highs briefly after lower than expected JOLTS openings, quits level lower (prior down-revised), layoffs broadly lower than expected. Prior to JOLTS, little react to Advance Goods Trade Balance, import decline and less negative goods export. Wholesale inventories slightly higher than expected, retail inventories in-line.

- Tsy Sep'25 10Y contract trades +19 at 111-11.5 vs. 111-12.5 high; nearing initial technical resistance at 111-14.5 (High Jul 22). A clear break would highlight a stronger reversal and open 111-28, the Jul 3 high. Key support remains intact at 110-08+, the Jul 14 and 16 low. A move through this support would reinstate a bearish theme.

- Curves bull flatten: 2s10s -3.051 at 44.734, 5s30s -3.148 at 95.557.

- Cross asset: Bbg US$ index firmer but off highs: BBDXY +1.65 at 1209.76 (1212.47 high); stocks moderately lower (SPX eminis -19.75 at 6403.0); gold firmer +9.30 at 3323.91.

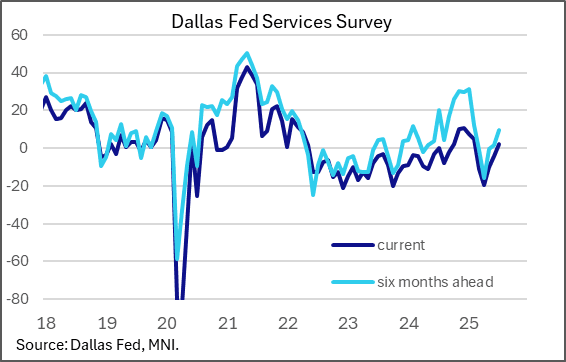

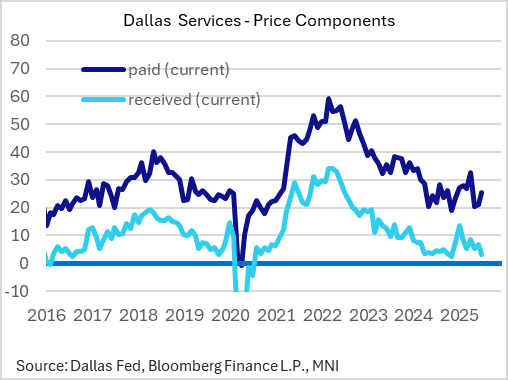

US DATA: Dallas Fed Regional Services Sentiment And Prices Pick Up

The Dallas Fed's Texas Service Sector Outlook Survey has bounced from weak readings in Q2, suggesting a pickup in regional activity to more normal levels after a tariff-related fall in sentiment albeit amid stubborn price pressures.

- General Business activity rose to 2.0 in July from -4.4 prior, marking the first positive reading since February. In tandem, the 6-month outlook rose to 9.8 from 1.5, for the highest reading also since February. Various key metrics improved including revenue, employment, and hours worked, with uncertainty falling to around the longer-term average.

- This echoes improvement in July's Philadelphia, NY, and Richmond services/non-manufacturing surveys (Kansas City was an outlier), as well as the rise in the July flash S&P Global PMI index.

- One area of concern was a renewed pickup in current prices paid, to 25.3 from 21.3 prior for a 3-month high, even as prices received dropped to 3.3 from 6.8 prior, marking an 8-month low. That potentially points to margin pressures for regional services firms.

- Overall services prices paid looked to have steadied/risen in July based on regional Fed surveys - we will preview the ISM Services reading for July ahead of release on August 5.

- Within the survey, Texas retail sales were flat, albeit at 0.8, the sales index was a strong improvement from -29.5 prior.