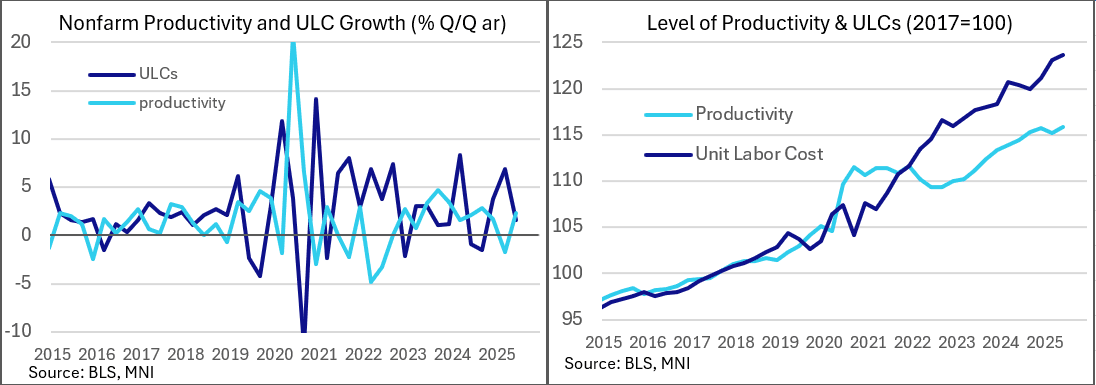

US DATA: Productivity And ULCs Suggest Disinflationary Progress Stalling

Aug-07 13:17

The BLS's preliminary report on Q2 Productivity and Costs was mixed: productivity growth exceeded expectations though saw a downward revision to Q1, while unit labor costs have been running a little hotter than previously thought. The data doesn't contradict many Federal Reserve officials' view that the labor market is not a significant source of inflation pressure, but disinflationary progress on this front has certainly stalled.

- Nonfarm productivity growth rose by 2.4% Q/Q SAAR in the preliminary estimate for Q2 2025 (2.0% SAAR expected, prior -1.8% rev from -1.5%). The breakdown: output increased by 3.7% while hours worked rose 1.3%.

- Unit labor costs meanwhile rose 1.6% Q/Q SAAR (1.5% expected, prior rev up to 6.9% from 6.6%). That was composed of a 4.0% rise in hourly compensation, offset by the aforementioned 2.4% increase in productivity. This is a reversion from Q1's very high reading which came amid a drop in productivity which now is recorded as even worse than previously estimated due to a downward revision to output.

- Private sector wages and salaries rose by the fastest rate (4.2% Q/Q SAAR) in Q2 in 5 quarters, up sharply from 3.1% prior, though we had this information from last week's Employment Cost Index release for Q2 which had come in slightly higher than expected.

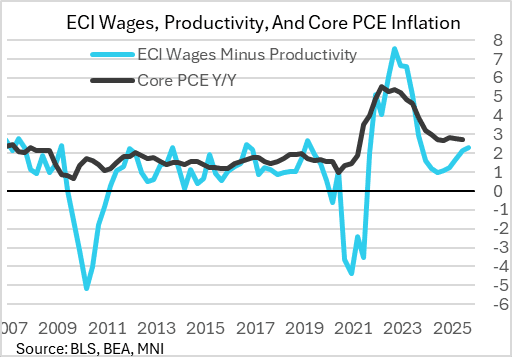

- Theoretically, to be consistent with the Fed's 2% inflation target, productivity growth could remain at Q2 rates with roughly 4.4% or below wage growth. Chair Powell said at July's FOMC press conference: "wages [are] still at a healthy level, but moving ever closer to what we would regard as long-run sustainable consistent with longer-run productivity and 2 percent inflation".

- Stepping back, productivity growth is running at just 1.3% Y/Y, less than half the rates seen throughout much of 2024 when inflation was coming down, with private industry wages and salaries rising at 3.6% Y/Y, down from 4+% in 2024.

- The differential between the two is running at a 2.3% clip, an 8-quarter high, suggesting potential inflationary pressures from the labor market slowly rebuilding. While a far cry from the 6+% rates in 2022 when core PCE was running at a 5+% clip, for perspective, it's roughly double the 1.2% differential that prevailed through the low-inflation 2010s.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: Effective Fed Funds Rate

Jul-08 13:05

FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $118B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $263B

MNI: RPT: Livestreamed MNI Connect VC with Fed Mary Daly On July 10

Jul-08 13:00

You are invited to listen to a Livestreamed MNI Connect Video Conference with the San Francisco Fed President Mary Daly.

Details below:

- Mary Daly joins us to discuss the ‘The US Economic Outlook and Challenges for Policymakers'

- DATE: Thursday, 10 July 2025

- TIME: 2:30 pm - 4 pm ET; 11:30am - 1pm PT; 7:30pm - 9pm London

- This event will be run as a Zoom Webinar and is a public, on-the-record event.

To register please go to: MNI Webcast Registration

MNI: US REDBOOK: JUL STORE SALES +5.1% V YR AGO MO

Jul-08 12:55

- MNI: US REDBOOK: JUL STORE SALES +5.1% V YR AGO MO

- US REDBOOK: STORE SALES +5.9% WK ENDED JUL 05 V YR AGO WK

Trending Top

Jun-25 06:23