JAPAN DATA: PPI Services Softer Than Forecast, Moving In Line With Headline CPI

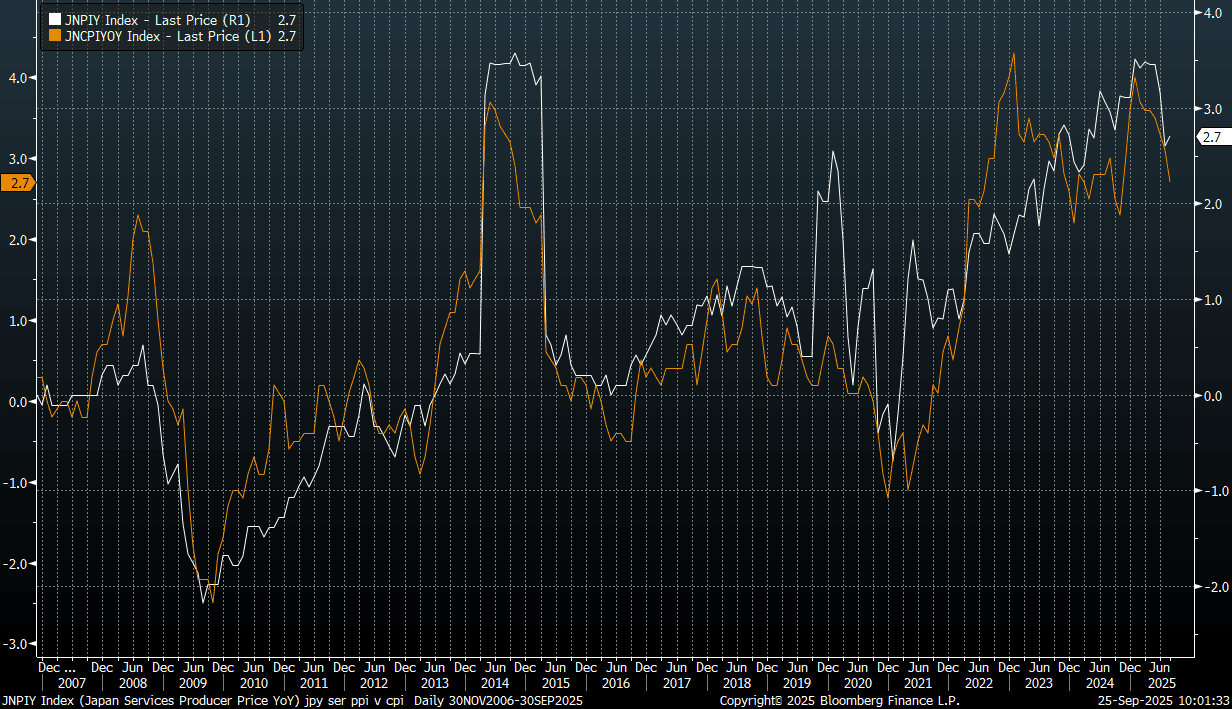

The Japan August PPI service print came in below expectations, printing at 2.7%y/y against a 2.9% forecast. Note that the July outcome was revised down to 2.6%y/y (originally reported at 2.9%). In m/m terms the services PPI was up 0.2%, same as the July outcome. This is up from June's -0.2%m/m, while April saw a 0.8% rise.

- The chart below plots the services PPI (white line) against headline CPI (orange line) (both in y/y terms). Today's PPI outcome brings it more into line with recent CPI outcomes, with the CPI tending to lead this recent period of softness in y/y momentum.

- Prices for services with high labour-cost ratios rose 3.3% y/y, unchanged from July, while those with low labor cost ratios climbed 2.2%, up from 1.7%.

- Via our Tokyo policy team: BOJ officials judge services prices continue to rise as companies pass on labour and distribution costs, though the pace lacks momentum. They remain focused on corporate price revisions due from October onward.

Fig 1: Japan PPI Services & Headline CPI (Y/Y)

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

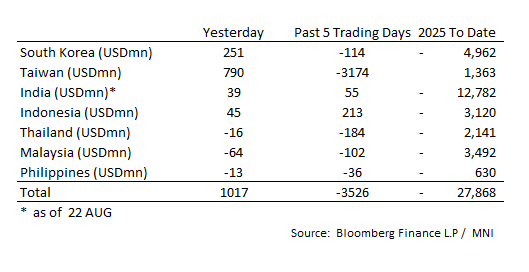

ASIA STOCKS: Daily Inflow Tops $1bn

The volatility in daily flows continues for Taiwan with a big inflow yesterday adding to a strong inflow for Korea to push total inflows for the major markets followed to over $1bn for the day.

- South Korea: Recorded inflows of +$251m yesterday, bringing the 5-day total to -$114m. 2025 to date flows are -$4,962. The 5-day average is -$23m, the 20-day average is +$68m and the 100-day average of -$9m.

- Taiwan: Had inflows of +$790m yesterday, with total outflows of -$3,174 m over the past 5 days. YTD flows are positive at +$1,363. The 5-day average is -$635m, the 20-day average of -$28m and the 100-day average of +$196m.

- India: Had inflows of +$39m as of the 22nd, with total inflows of +$55m over the past 5 days. YTD flows are negative -$12,782m. The 5-day average is +$11m, the 20-day average of -$189m and the 100-day average of +$12m.

- Indonesia: Had inflows of +$45m yesterday, with total inflows of +$213m over the prior five days. YTD flows are negative -$3,120m. The 5-day average is +$43m, the 20-day average +$25m and the 100-day average -$16m.

- Thailand: Recorded outflows of -$16m yesterday, with outflows totaling -$184m over the past 5 days. YTD flows are negative at -$2,141m. The 5-day average is -$37m, the 20-day average of -$7m and the 100-day average of -$11m.

- Malaysia: Recorded outflows as of -$64m yesterday, totaling -$102m over the past 5 days. YTD flows are negative at -$3,492m. The 5-day average is -$20m, the 20-day average of -$30m and the 100-day average of -$13m.

- Philippines: Recorded outflows of -$13m yesterday, with net outflows of -$36m over the past 5 days. YTD flows are negative at -$630m. The 5-day average is -$7m, the 20-day average of -$1m the 100-day average of -$4m.

MNI: JAPAN JULY SERVICES PPI +2.9% Y/Y; JUNE UNREV +3.2%

- MNI: JAPAN JULY SERVICES PPI +2.9% Y/Y; JUNE UNREV +3.2%

- JAPAN JULY SERVICES PPI +0.3% M/M: JUNE REV -0.2%

JGBS: JGB Futures Close To July Lows, PPI Services Coming Up Shortly

JGB futures settled at 137.45, -.05 versus settlement levels post the Tokyo close on Monday. We remain within striking distance of July lows at 137.32.

- The US bias was for weaker futures on Monday, as markets retraced some of Friday's rally in the aftermath of Powell's Jackson Hole speech. Some caution in markets remains ahead of key inflation data this week, whilst from Monday's US session we also better than expected housing data (which also weighed on futures). The early bias in US Tsy futures today is little changed.

- In the cash JGB space, the 10yr finished Monday trade around 1.62%, so close to recent cycle highs. The 30yr is near 3.22%. The Japan 2/30yield curve remains elevated, near +235bps.

- In the swap space, the 10yr was last near 1.42%.

- Coming up shortly we have the July PPI services print.

- On the Supply front, Thursday delivers a 2yr bond sale, but there will be greater focus on next week's 10yr auction.