CANADA: Post-CPI And Jobs, Analysts Firmly See July BOC Hold

The broad scope of analysts followed by MNI are increasingly unanimous that the BOC will hold rates on July 30, following firmer-than-expected June core inflation data this week and strong June jobs data last week. Last week after the labour market report, CIBC revoked its call for a July cut, with National and BMO Economics appearing to also but confirming that in the wake of CPI. Note: a 25bp July cut is now just <8% priced.

- The last holdout among Canadian banks - Desjardins - no longer sees a BOC rate cut in July, a view it had stuck with after last week's strong labour market report. "Despite signs of an economic slowdown due to trade tensions with the United States, we expect the Bank to put more focus on recent employment gains and, to a larger degree, the rebound in core inflation. As such, the BoC is likely to keep rates steady at its upcoming meeting at the end of the July. However, with economic storm clouds still on the horizon, we are of the view that the Bank will resume cutting interest rates in September... Statistics Canada chalked some of the acceleration in June goods inflation to higher costs resulting from the trade war (see our analysis External link.). But even this pales in comparison to services inflation which, at 3.0% in June, has had a three-handle in it in every month but one since August 2021... the reprieve in underlying inflation in May could have been short lived."

- Citi also has pushed back its view for the next rate cut to September: "Core measures are still averaging above the target range at 3.05%, which will likely keep BoC officials on hold this month. But details of June inflation data do not leave us more concerned about fundamental stickiness in core inflation. Most importantly, shelter inflation should continue easing as home prices fall and slowing population growth implies less upward pressure on rents. Softer demand generally, with soft discretionary services prices in June should continue to weigh on inflationary pressures. We now expect the BoC to resume rate cuts in September."

- CIBC writes that "showed price pressures likely remained a bit too firm for the BoC’s liking... On the heels of a good job report and somewhat firm price pressures, we expect the BoC to remain on pause in July because this is a central bank that by its own admission isn’t very comfortable being forward-looking...Overall, the increases in prices seen today don't really look very durable and look more like idiosyncratic price level adjustments, especially considering the widening slack, high economic uncertainty and slowing income gains."

- National: "Given this morning's data, it is even more likely that the Bank of Canada will remain on the sidelines in July...While the Canadian economy was weakened in the first half of the year by tariff uncertainty, as evidenced by the decline in GDP in April and May and the unemployment rate rising by three-tenths of a percentage point from February to June, this has not yet resulted in lower inflationary pressures. We continue to believe that monetary accommodation will be necessary by the end of the year."

- Scotiabank: "The Bank of Canada is on an extended policy hold that is reinforced by this morning’s core inflation readings.... The inflation excuses have grown tired as every measure of core inflation is sending warning signals. There was no clear distorting role played by seasonal adjustment factors this time as the June 2025 SA factor wasn’t terribly dissimilar to past months of June."

- RBC: "We continue to expect Canada's restrained approach to retaliation to tariffs from the U.S. administration will limit the impact of the trade war on Canadian consumer prices. But firmer price growth among domestically produced and consumed services comes alongside a June labour market rebound, improved business sentiment, and resilient consumer spending trends. While downside risks to economic growth persist, recent data is consistent with our base-case view that the Bank of Canada will not cut interest rates again this cycle, having opted to skip cuts at its last two meetings."

- BMO: "gives the Bank of Canada almost nothing to justify a rate cut in July. If the solid employment report was the icing on the cake for that decision, this is the cherry on top. Simply put, underlying inflation remains stubbornly strong. We'll need to see a material deceleration in core for a cut in even the September meeting to be in play, barring a steep deterioration in the economy (which can't be ruled out with the ongoing tariff uncertainty)....The key question is: Why is core inflation so sticky, with growth struggling and the economy operating below capacity? The main reasons are that a) shelter costs have a long tail, and are receding only gradually, and b) there are some pressures from the trade war, notably in durable goods and some groceries. "

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US: FED Reverse Repo Operation

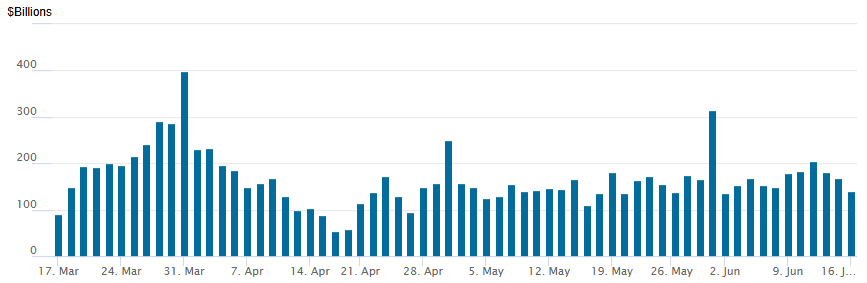

RRP usage retreats to $140.759B this afternoon from $168.645B Friday, total number of counterparties at 26. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B.

STIR: Narrow Ranges, US Retail Sales Tomorrow

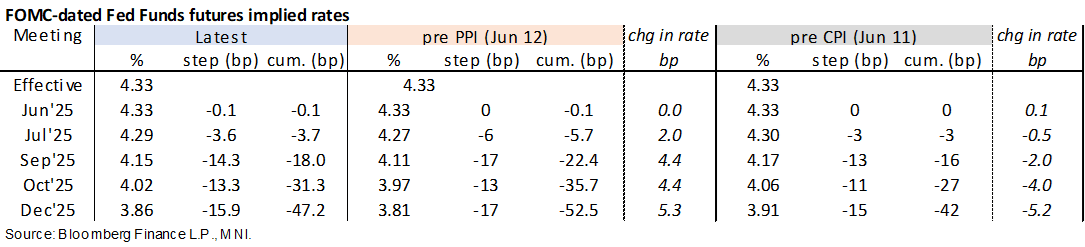

- Fed Funds implied rates for near-term meetings have pushed higher through today’s US session, whilst the Dec’25 has held narrow ranges since the US crossover to consolidate an overnight push higher as markets looked for Israel-Iran de-escalation.

- Cumulative cuts from 4.33% effective: 0bp for Wed, 3.5bp Jul, 18bp Sep, 31.5bp Oct and 47bp Dec.

- The SOFR implied terminal yield of 3.31% (SFRZ6) is 1bp lower on the day as it holds close to ~100bp of cuts for what’s left of the cycle.

- The limited change since the US crossover comes with net gains for US equity futures vs net losses for crude futures and spot gold.

- G7 headlines today have seen Trump unwilling to sign the statement on Israel-Iran and looking at a US-Canada deal being achievable within days or weeks.

- Today’s weak Empire manufacturing release didn’t move the needle, with the headline miss offset by a much-improved outlook within the report.

- Tomorrow sees more notable data including retail sales and import prices for May at 0830ET before industrial production for May at 0915ET. They provide important hard data updates for May heading into the two-day FOMC meeting starting tomorrow.

- MNI Fed Preview: https://media.marketnews.com/Fed_Prev_Jun2025_ba372b9458.pdf

LOOK AHEAD: Tuesday Data Calendar

- US Data/Speaker Calendar (prior, estimate)

- 17-Jun 0830 Retail Sales Adv MoM (0.1%, -0.6%); Ex Auto (0.1%, 0.2%)

- 17-Jun 0830 Retail Sales Control Group (-0.2%, 0.3%)

- 17-Jun 0830 Import Price Index MoM (0.1%, -0.2%), YoY (0.1%, 0.0%)

- 17-Jun 0830 Export Price Index MoM (0.1%, -0.2%), YoY (2.0%, --)

- 17-Jun 0830 New York Fed Services Business Activity (-16.2, --)

- 17-Jun 0915 Industrial Production MoM (0.0%, 0.0%)

- 17-Jun 0915 Capacity Utilization (77.7%, 77.7%)

- 17-Jun 0915 Manufacturing (SIC) Production (-0.4%, 0.1%)

- 17-Jun 1000 Business Inventories (0.1%, 0.0%)

- 17-Jun 1000 NAHB Housing Market Index (34, 36)

- 17-Jun 1130 US Tsy $55B 6W bill auction

- 17-Jun 1300 US Tsy $23B 5Y TIPS re-open auction (91282CNB3)

- Source: Bloomberg Finance L.P. / MNI