CANADA DATA: Population Declines In Q3 As Government Curbs Immigration

- Canada's population fell 76,068 or 0.2% in Q3 to 41,575,585, StatsCan said Wed in a preliminary estimate.

- By comparison the population in Q3 2023 grew the fastest since 1957 at +1%, and by +0.6% in Q3 2024.

- Fall led by non-permanent residents -176,479, mainly those on work and student permits. They now represent 6.8% of Canada's population, a share the govt has said is too high.

- Swings in population have pressured housing costs and made it more difficult to assess slack in the economy and job market. Unemployment has declined in recent months as hiring advanced while labor force declined.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CANADA DATA: Core CPI Latest Trends: Flat/Softer

Canadian inflation gauges looked flat/softer almost across the board in terms of sequential pressures in October, including core and measures. Some of the 3M run rates for core metrics (xFE, ex-volatile / taxes) after a softer July was replaced in the calculation by stronger September/October figures, but the 6 month rates were uniformly softer.

Core CPI (median & trim av):

% M/M: 0.18 in Oct'25 after 0.23 in Sep'25

% 3mth ar: 2.6 in Oct'25 after 2.7 in Sep'25

% 6mth ar: 2.56 in Oct'25 after 2.95 in Sep'25

% Y/Y: 2.95 in Oct'25 after 3.1 in Sep'25

CPI xFE (ex food & energy):

% M/M: 0.26 in Oct'25 after 0.26 in Sep'25

% 3mth ar: 2.61 in Oct'25 after 1.82 in Sep'25

% 6mth ar: 2.35 in Oct'25 after 2.49 in Sep'25

CPIX (ex 8 most volatile & indirect taxes):

% M/M: 0.31 in Oct'25 after 0.31 in Sep'25

% 3mth ar: 3.31 in Oct'25 after 2.29 in Sep'25

% 6mth ar: 2.8 in Oct'25 after 3.08 in Sep'25

Source: Bloomberg Finance L.P., MNI

EQUITY OPTIONS: Santander Put Option trade

BSD (18/12/26) 8.5p, traded at 0.863 in 10k (suggest seller and new position).

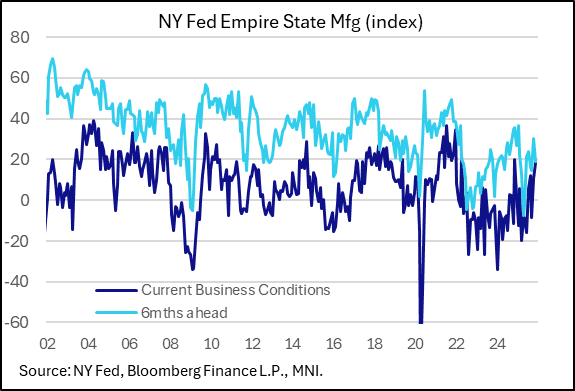

US DATA: Empire Manufacturing Solidifies For 2nd Consecutive Month

The NY Fed's Empire State Manufacturing Survey impressed in November, with the current General Business Conditions index rising 8 points to a 1-year high 18.7 (well above the 5.8 expected). As such it's the 2nd highest reading since April 2022, with solidly-above-long-term average-readings now for 2 consecutive months, the first time we've seen that since 2021 for this notoriously volatile survey.

- The 6-month outlook pulled back 19.1 from to 30.3 prior, which had been the highest optimism since January.

- Activity indices were strong. New orders jumped to 15.9 from 3.7, setting a 12-month high just 2 months after setting a 17-month low; shipments rose 2 points to 16.8 while inventories turned positive after 3 consecutive negative months.

- The employment gauge edged up to 6.6 from 6.2, for a fresh 4-month high, while the average workweek rose to a multiyear high.

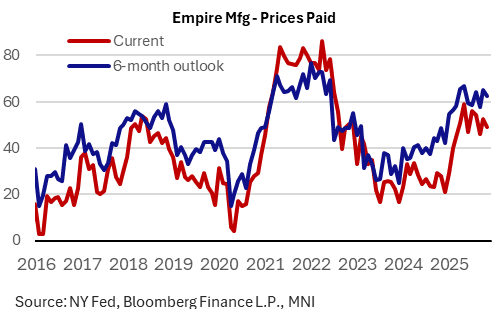

- Inflation remained stubbornly high but didn't show signs of worsening. Current prices paid fell to 49.0 after 52.4, with expected prices paid 6-months ahead down to 62.5 from 65.0. Both are elevated but suggest some moderation after October's sharp M/M rise that suggested inflation was picking up alongside with activity.

- In short, a solid start to the month's regional Fed manufacturing surveys.