MEXICO: Pemex Tender Results - Neutral

(PEMEX; B1/BBB/BB*+)

Pemex announced the principal amount they expect to accept for purchase which was capped at a maximum amount of up to USD9.9bn. We see the principal amount adding up to about USD9.7bn.

The company said they would accept all of the tendered bonds in priority levels 1 through 7 but only €550mn from level 8 out of about €908mn. Please see the following table for further details:

| Securities | Principal Amount Outstanding | Acceptance Priority Level | Principal Amount Tendered by the Early Tender Date | Principal Amount Expected to be Accepted for Purchase | ||||

| 4.500% Notes due 2026 | US$1,126,084,000 | 1 | U.S.$694,201,000 | U.S.$694,201,000 | ||||

| 3.750% Notes due 2026 | €1,000,000,000 | 2 | €532,898,000 | €532,898,000 | ||||

| 6.875% Notes due 2026 | US$2,526,854,000 | 3 | U.S.$1,491,549,000 | U.S.$1,491,549,000 | ||||

| 5.350% Notes due 2028 | US$1,988,837,000 | 4 | U.S.$1,189,743,000 | U.S.$1,189,743,000 | ||||

| 4.875% Notes due 2028 | €1,250,000,000 | 5 | €830,923,000 | €830,923,000 | ||||

| 6.490% Notes due 2027 | US$1,549,022,000 | 6 | U.S.$1,260,291,000 | U.S.$1,260,291,000 | ||||

| 6.500% Notes due 2027 | US$4,016,962,000 | 7 | U.S.$2,815,019,000 | U.S.$2,815,019,000 | ||||

| 2.750% Notes due 2027 | €1,250,000,000 | 8 | €907,754,000 | €550,001,000 | ||||

| 9.500% Notes due 2027 | US$265,797,000 | 9 | U.S.$182,595,000 | - | ||||

| 6.500% Notes due 2029 | US$1,206,861,000 | 10 | U.S.$571,595,000 | - | ||||

| 8.750% Notes due 2029 | US$1,984,688,669 | 11 | U.S.$1,057,210,723 | - |

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUDUSD TECHS: Approaching Key Short-Term Support

- RES 4: 0.6688 High Nov 7 ‘24

- RES 3: 0.6677 0.764 proj of the Jun 23 - Jul 11 - 17 price swing

- RES 2: 0.6569/6625 High Aug 14 / 24 and the bull trigger

- RES 1: 0.6500 50-day EMA

- PRICE: 0.6435 @ 16:20 BST Aug 20

- SUP 1: 0.6419 Low Aug 1 and a bear trigger

- SUP 2: 0.6373 Low Jun 23

- SUP 3: 0.6354 38.2% retracement of the Apr 9 - Jul 24 upleg

- SUP 4: 0.6323 Low Apr 16

AUDUSD is off its most recent highs to trade lower Wednesday. From a trend perspective, the condition remains bullish highlighted by MA studies that remain in a bull-mode position. However, the pair is approaching support at 0.6419, the Aug 1 low and a bear trigger. A clear break of this level would expose support at 0.6373, Jun 23 low and an important support. On the upside, a reversal higher would refocus attention on 0.6625, the Aug 24 high.

US TSYS: Late SOFR/Treasury Option Roundup: Year End Rate Cut Call Buying

Various upside call structures targeting more rate cuts than currently priced traded Wednesday, SOFR outpacing Treasury options for the most part - though paper bought over 100k TYV5 113 calls earlier, adding to some 78k Tuesday. Underlying futures trade modestly higher after the bell - paring gains slightly after mixed messaging in the July FOMC minutes. Projected rate cuts consolidate from midday high to near steady vs. early morning (*) levels: Sep'25 at -20.6bp (-21.1bp), Oct'25 at -34.1bp (-34.9bp), Dec'25 at -54.0bp (-54.1bp), Jan'26 at -65.4bp (-65.1bp).

- SOFR Options:

- Block, 5,000 SFRH6 96.25/97.25 call spds, 26.5

- +50,000 SFRH6 97.25 calls, 6.0-6.5 covered

- +50,000 SFRZ5 96.18/96.31/96.50/96.62 call condors, 3.0-3.125 ref 96.205

- +15,000 SFRU6 96.00/96.25/96.50 put flys, 3.25

- +5,000 SFRU5 95.81 puts, 3.25 vs. 95.90/0.30%

- 3,500 SFRU5 96.00/96.12/96.25 call flys ref 95.8975

- -20,000 SFRU5 95.81/SFRZ5 95.87 put spds, 0.75 net/Sep over

- +4,000 SFRU5 95.62/96.31 call over risk reversals, 0.25 ref 95.9025

- 8,000 SFRU6 96.75/97.25 2x1 put spds ref 96.805

- 1,400 SFRZ5 96.25/96.37/96.50/96.62 call condors ref 96.21

- Block, 4,500 SFRZ5 96.25/96.50/96.75/97.00 call condors, 6.0 ref 96.21

- 6,000 SFRU5 96.00/96.12/96.25 call flys ref 95.90

- 6,000 SFRU5 95.87/95.93 put spds ref 95.90

- Treasury Options: (reminder Sep options expire Friday)

- +10,000 USV5 119 calls, 16

- Block: -5,000 WNU5 117.5 puts 20 over the WNV5 116/119 put over risk reversal

- -8,000 TYV5 111.5 puts, 34 vs. 111-30.5/0.40%

- 1,700 FVU5 108.5 puts, 3.5 total volume over 6k

- 5,000 wk5 TU 103.75/103.87/104 put trees vs. TUU5 103.75 puts

- Block/screen, over 10,800 TYU5 111 puts, 2 vs. 111-22.5/0.08%

- over 5,600 TYU5 112 calls, 8 last

- over 5,300 TYU5 112.5 calls, 2 last

- over 103,600 TYV5 113 calls, 20-23 ref 111-24.5 to -25.5 (78k trade Tuesday)

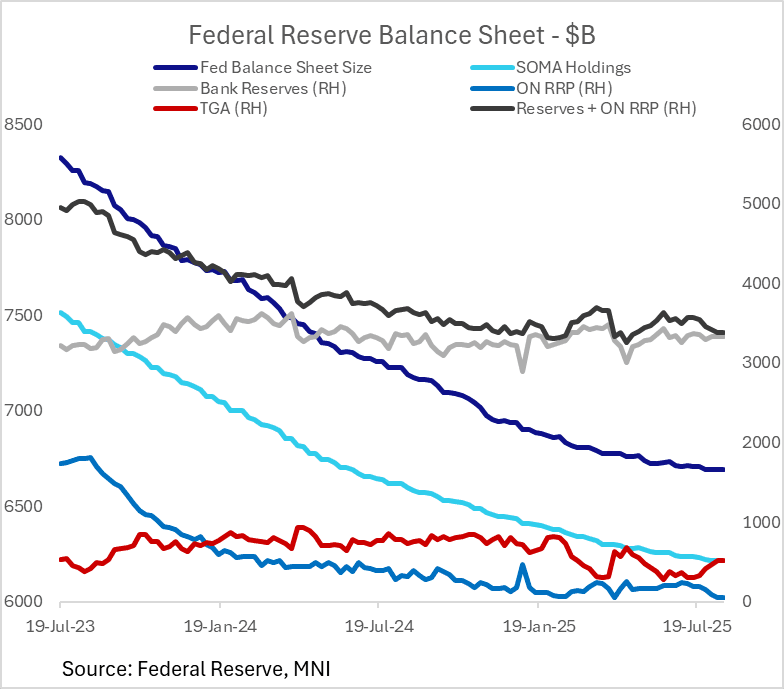

FED: July FOMC Minutes: Reserves "Abundant", Quarter-End SRF Takeup Eyed (3/3)

The July meeting devoted some discussion to the ongoing drawdown in reserves amid the Treasury cash rebuild. Overall, the Committee seem to be comfortable with the trajectory of reserves, despite some caution that reserves could be headed into "ample" from the current "abundant" territory.

- With regard to near-term funding pressures, namely potential for the mid-September tax date and Q3 quarter-end posing risks, the minutes suggest that while there may be some temporary acute liquidity issues, they can be resolved by takeup of the standing repo facility.

- As such, there was no real discussion of a shift in balance sheet management policy, particularly with QT proceeding "smoothly" and rerserves remaining "abundant", though vigilance of money market conditions would continue to be important.

- SOMA Manager Perli: "Market indicators continued to suggest that reserves remained abundant; however, ongoing System Open Market Account (SOMA) portfolio runoff, a substantial expected increase in the TGA balance, and the depletion of the ON RRP facility were together likely to bring about a sustained decline in reserves for the first time since portfolio runoff started in June 2022. Against this backdrop, the staff would continue to monitor indicators of reserve conditions closely. The manager also noted that there would be times—such as quarter-ends, tax dates, and days associated with large settlements of Treasury securities—when reserves were likely to dip temporarily to even lower levels. At those times, utilization of the SRF would likely support the smooth functioning of money markets and the implementation of monetary policy."

- And the broader FOMC: "Several participants remarked on issues related to the Federal Reserve's balance sheet. Of those who commented, participants observed that balance sheet reduction had been proceeding smoothly thus far and that various indicators pointed to reserves being abundant. They agreed that, with reserves projected to decline amid the rebuilding of the TGA balance following the resolution of the debt limit situation, it was important to monitor money market conditions closely and to continue to evaluate how close reserves were to their ample level. A few participants also assessed that, in this environment, abrupt further declines in reserves could occur on key reporting and payment flow days. They noted that, if such events created pressures in money markets, the Federal Reserve's existing tools would help supply additional reserves and keep the effective federal funds rate within the target range. A couple of participants highlighted the role of the SRF in monetary policy implementation—as reflected in increased usage at the June quarter-end—and expressed support for further study of the possibility of central clearing of the SRF to enhance its effectiveness."