MEXICO: May Industrial Output Rises 0.7% M/m, Above Expectations

Jul-12 12:01

- "*MEXICO MAY INDUSTRIAL PRODUCTION RISES 0.7% M/M; EST. +0.4%"

- "*MEXICO MAY INDUSTRIAL PRODUCTION RISES 1.0% Y/Y; EST. +1.1%"

- "*MEXICO MAY MFG PRODUCTION FALLS 1.4% Y/Y; EST. +0.2%" (BBG)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: Sep'24 SOFR Call Spread Buy

Jun-12 11:56

- +5,000 SFRU4 94.81/94.93 call spds, 4.5 ref 94.82

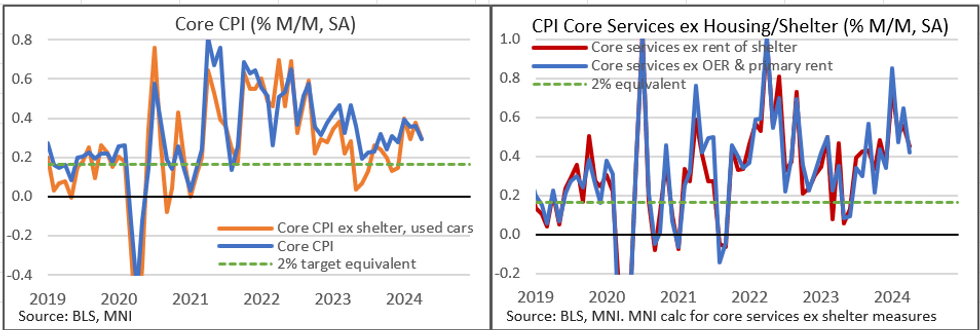

US INFLATION: May CPI (1/2): Core M/M Expected Slightly Lower, Supercore Steady

Jun-12 11:44

Here are a few areas to watch for today's May CPI release (0830ET/1330UK):

- Sequential core inflation is seen remaining relatively steady in May at 0.3% M/M (median; 0.28% average unrounded) vs 0.29% in April, per MNI’s compilation of sell-side previews.

- Headline CPI is expected to pull back fairly sharply to 0.1% (median; 0.12% average unrounded) vs 0.31% in April, owing largely to a drop in energy/gasoline prices on a seasonally-adjusted basis.

- Both core services and core goods inflation prints are seen relatively steady versus April, with owners’ equivalent rent (OER) and rents at around 0.4% M/M each, used car and lodging prices rebounding, and car insurance inflation cooling slightly but still very high.

- This outcome should likewise keep “supercore” (core services ex-shelter) inflation fairly steady also around 0.4%, albeit with a decent dispersion of analyst expectations (0.36-0.46%).

US TSYS: Early SOFR/Treasury Option Roundup

Jun-12 11:42

Mixed SOFR and Treasury option traded on modest overnight volumes so far. SOFR options seeing some recent put spds Blocked recently, Jul'24 5Y calls seeing some interest as underlying futures hold modest gains ahead this morning's CPI inflation data and FOMC policy annc this afternoon. Rate cut projections hold largely steady vs. late Tuesday levels: June 2024 at -1.3% w/ cumulative rate cut -.3bp at 5.328%, July'24 at -8% w/ cumulative at -2.3bp at 5.307%, Sep'24 cumulative -14.8bp, Nov'24 cumulative -22bp, Dec'24 -39.9bp.

- SOFR Options:

- Block, 3,000 SFRQ4 94.75/94.87 put spds, 7.0 ref 94.825

- Block, 4,395 SFRX4 94.56/94.62/94.68/94.75 put condors, 1.5 vs. 95.045/0.05%

- 2,000 SFRN4 94.87/94.93 call spds vs. SFRU4 94.81/94.87 call spds

- 1,500 SFRZ4 96.12/96.25 call spds ref 95.065

- 1,000 SFRU4/SFRZ4 94.62/94.81 put spd spd

- 1,600 SFRN4 94.87 calls ref 94.815

- 2,000 SFRN4 94.75/94.87 1x2 call spds ref 94.815

- Treasury Options:

- 3,700 Wednesday weekly 10Y 108.5/108.75 put spds

- 6,100 FVN4 107 calls ref 106-08.5

- over 6,500 FVN4 106.5 calls

- 5,000 wk2 5Y 107.5/108 call spds ref 106-08.75