JPY: Overnight Vols Elevated As USD/JPY Drifts Lower Ahead Of BoJ

USD/JPY overnight vol continues to climb as we await the BOJ decision, last 18.565%, although we sit off earlier highs close to +20%. This is fresh highs back to the middle part of the year. It implies a 151.13-153.80 range in USD/JPY, with a probability of 76%. USD/JPY is drifting a little lower, last back under 152.50. We do have a reasonable expiry at this strike rate for NY cut tomorrow ($1.2bn).

- Focus elsewhere is on the Trump-Xi meeting, which is now underway. US equity futures are tracking higher (earlier firm Samsung results in the chip space aiding sentiment). US Tsy yields are sitting slightly lower, although losses aren't much beyond 1bps at this stage (providing some offset for USD/JPY given the risk on tone from US equity futures). Broader USD sentiment is softer, with AUD and NZD ticking up +0.25%.

- A reminder on USD/JPY levels, 153.27 on the topside is the bull trigger, while the 20-day EMA has a 151.00 handle and the 50-day is back around 149.90.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Bull-Flattener Holding At Lunch, BOJ SOO: No Clear Hint For Oct Hike

At the Tokyo lunch break, JGB futures are stronger, +9 compared to settlement levels.

- MNI - Bank of Japan board members were split over whether to raise the policy rate at the September 18-19 meeting, with some calling for more data and others pushing for an increase, the summary of opinions released Tuesday showed. The disclosures gave no clear signal of an October move, with most members aside from Naoki Tamura and Hajime Takata - who dissented and proposed a hike - seeing little urgency.

- MNI - Japan's industrial output fell 1.2% m/m in August, marking a second straight decline after July's 1.2% drop, as stronger automobile production was offset by weakness in electrical machinery and information and communications equipment, data from the Ministry of Economy, Trade and Industry showed Tuesday.

- Industrial output is a key indicator for BOJ economists tracking the pace of Japan's modest recovery as it reflects both external and domestic demand.

- Cash US tsys are slightly cheaper, with a steepening bias, in today's Asia-Pac session after yesterday's bull-flattener.

- Cash JGBs have bull-flattened across benchmarks, with yields flat to 3bps richer. The benchmark 10-year yield is 1.2bps lower at 1.631% versus the cycle high of 1.670%.

- Swap rates are little changed.

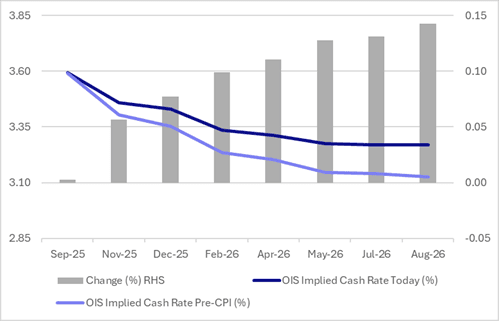

STIR: RBA Dated OIS Sharply Firmer Than August CPI Levels

Ahead of today’s RBA policy decision, RBA-dated OIS pricing is sharply firmer across 2026 meetings versus last Wednesday’s CPI levels.

- The headline August CPI print was 3.0%y/y, against a 2.9% market consensus and 2.8% July outcome. The trimmed mean was 2.6% y/y, after printing 2.7% in July.

- The Q3 CPI print is out on Oct 29, with the RBA outcome on Nov 4.

- A 25bp rate cut today is given a 3% probability, with a cumulative 17bps of easing priced by year-end.

Figure 1: RBA-Dated OIS – Today Vs. Pre-CPI

Source: Bloomberg Finance LP / MNI

AUSSIE BONDS: Little Changed Ahead Of RBA Policy Decision

ACGBs (YM -1.0 & XM +1.0) are slightly mixed ahead of the RBA Policy Decision.

- Building approvals fell 6.0% m/m (estimate +2.6%) in August versus revised -10.0% in July.

- Private-sector home approvals fell 2.6% m/m versus revised +1.3% in July.

- Cash US tsys are slightly cheaper, with a steepening bias, in today's Asia-Pac session after yesterday's bull-flattener.

- MNI SECURITY: Trump Admin Will Proceed w/AUKUS Following Pentagon Review - Nikkei. Nikkei Asia reporting, "The Trump administration will proceed with the AUKUS defence pact linking the U.S., U.K. and Australia, maintaining the original timeline that includes the sale of three Virginia-class submarines to Canberra beginning in 2032..." The report comes after a Pentagon review in June, ordered by US Undersecretary of Defence Elbridge Colby, threw doubt over US participation in the nuclear submarine alliance.

- Cash ACGBs are 1bp cheaper to 1bp richer with the AU-US 10-year yield differential at +17bps.

- The bills strip is -1 to -3 across contracts.

- RBA-dated OIS pricing gives a 25bp rate cut today a 3% probability, with a cumulative 17bps of easing by year-end.