CHILE: Nominal Wage Figures Due Today, August CPI, BCCh Rate Decision Next Week

- Amid a pullback in copper prices, USDCLP edged up by 0.3% yesterday to close at 972. A bull cycle in USDCLP remains in play, with scope seen for an extension towards 987.67, the 76.4% retracement of the sell-off between Apr 9 - Jul 2. Key support to watch is at 960.69, the 50-day EMA. A clear break of this average is required to instead signal a stronger reversal. This would expose 946.49, the Jul 23 low.

- On the data front, July nominal wage figures will be published at 1400BST(0900ET). In June, wages rose by 7.5% y/y, the slowest pace this year, following an 8.1% gain in May.

- Following this, attention will turn to key August CPI inflation data on Monday, which come just ahead of the central bank’s monetary policy meeting on Tuesday. After surprising to the upside last month, headline inflation is expected to edge down to 4.1% y/y in August, keeping it above the top of the 2-4% target range.

- Nonetheless, amid recent upbeat non-mining activity data as well, most analysts expect the central bank to stay on hold next week, before cutting again later this year. This is consistent with yesterday’s BCCh traders survey, which indicated that market participants expect a rate hold on Tuesday, followed by a 25bp cut to 4.5% in October.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GERMANY: Mixed Analyst Views On Today's Factory Orders Data

Analysts draw a bit mixed conclusions from today's German manufacturing orders data (our commentary here: June Factory Orders Constitute A Move Sideways On Weak Levels), with Commerzbank screening a little more pessimistic than JP Morgan:

- Commerzbank: "Overall, order intake excluding major orders is thus back at the level seen at the beginning of the year, once again dashing hopes for a sustained recovery in German industry. Early indicators such as the purchasing managers' index in the manufacturing sector and the Ifo business climate index had pointed to a slight recovery in the second quarter. However, these positive expectations are clearly not yet reflected in hard order figures. This underlines our assumption that the German economy will only grow moderately this year."

- "There is now a risk that US tariffs will create further headwinds for German industry. In June, orders from abroad fell by 3.0%. This is exclusively attributable to trade with countries outside the eurozone. This could already be an indication of the damaging effect of US tariffs on German exports."

- JP Morgan: "factory sales and VDA car production showed broad stability, although with some noise [...] Domestic orders are still not really turning higher, which is disappointing, but the fiscal shift is likely to provide support going forward. As a cross-check on the data, the new orders index of the German manufacturing PMI is signalling broadly stable orders at present, rather than positive growth. But even that is an improvement from where the PMI has been a few months ago."

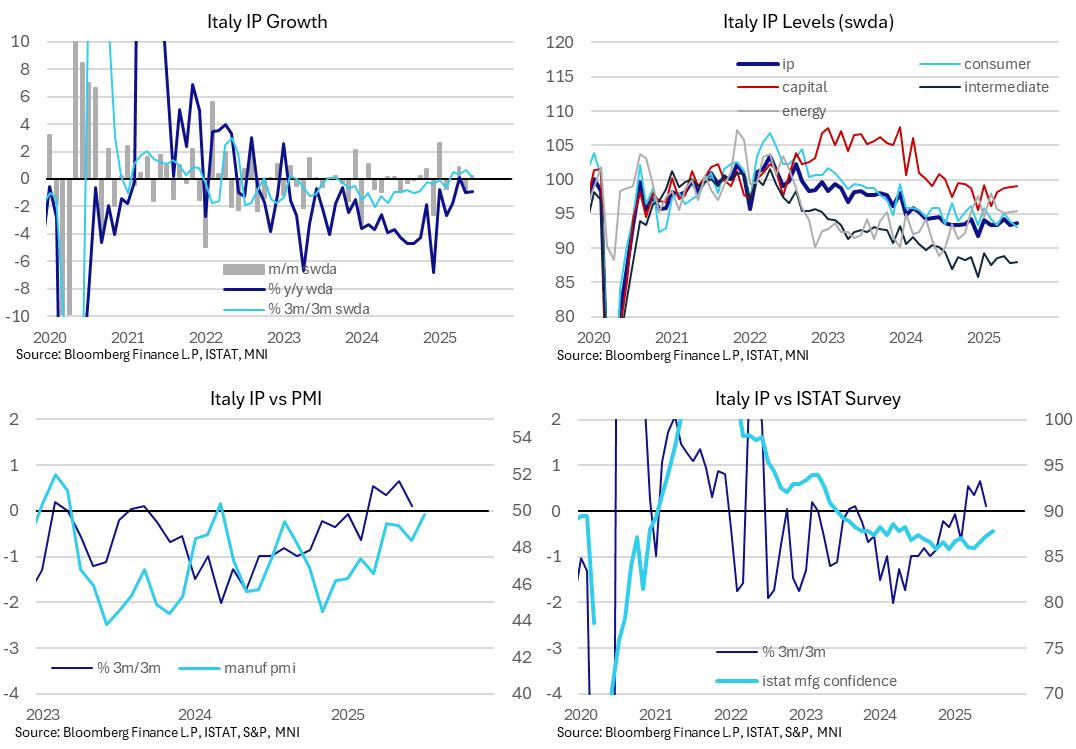

ITALY DATA: Another Stronger-than-expected June IP Report

Italian industrial production was stronger-than-expected in June at 0.2% M/M (vs -0.2% cons, a one tenth downwardly revised -0.8 prior). The Italian print follows stronger-than-expected readings in France and Spain yesterday. Germany will release its June IP figures tomorrow morning.

- Italian manufacturing sentiment data for July points to a continuation of this year’s gradual recovery, with the manufacturing PMI at its highest since March 2024 at 49.8 (vs 48.4 in June) and ISTAT’s manufacturing sentiment series at 87.8 (vs 87.3 in June).

- On a 3m/3m basis, IP rose just 0.1% in June, down from 0.6% in May. ISTAT noted that industry made a negative contribution to total gross value added in Q2, according to flash data released last month.

- Across components, there was slight growth in energy (0.1% M/M), intermediate goods (0.2% M/M) and capital goods (0.1% M/M) production in June. Meanwhile, consumer goods production fell 0.9% M/M (vs -1.3% in May).

US TSYS: Goldman Note Risk Of Further Curve Steepening

Goldman Sachs write “the shift in Fed cut pricing has compressed the gap between the market and our economists' expected Fed path. Despite the abruptness of last Friday's rally, we think risk/reward favours remaining long the front end in the U.S.. The timing and pace of any policy adjustment are key to dictating the curve shape, with the sustained outperformance of 5s at risk in the event of more rapid cuts”.

- They go on to note that “while the long end of the curve is somewhat cheap versus fundamentals, we nonetheless expect that evidence of further economic weakness would justify stronger front-end outperformance and sharper curve steepening”.

- Goldman’s “year-end forecasts of 3.45% 2-Year and 4.20% 10-Year yields imply steepening of the spot curve and relatively stable longer term rates”.