AUDNZD: Near Term Risks Skewed Lower, But Dips Likely To Be Supported

The AUD/NZD cross is holding lower, last near 1.1420/25 just up from session lows of 1.1407. NZD is the main outperformer in the G10 space, up 1.25%, as the earlier hawkish RBNZ 25bps cut drove short covering (with a potential end to the easing cycle). NZD/USD may continue to outperform in the near term, particularly if broader risk trends stabilize/improve further. As we noted earlier, "the risk into the RBNZ today is if they are not dovish enough and any hint of a potential future pause could provide short-term headwinds for some of the weaker hands".

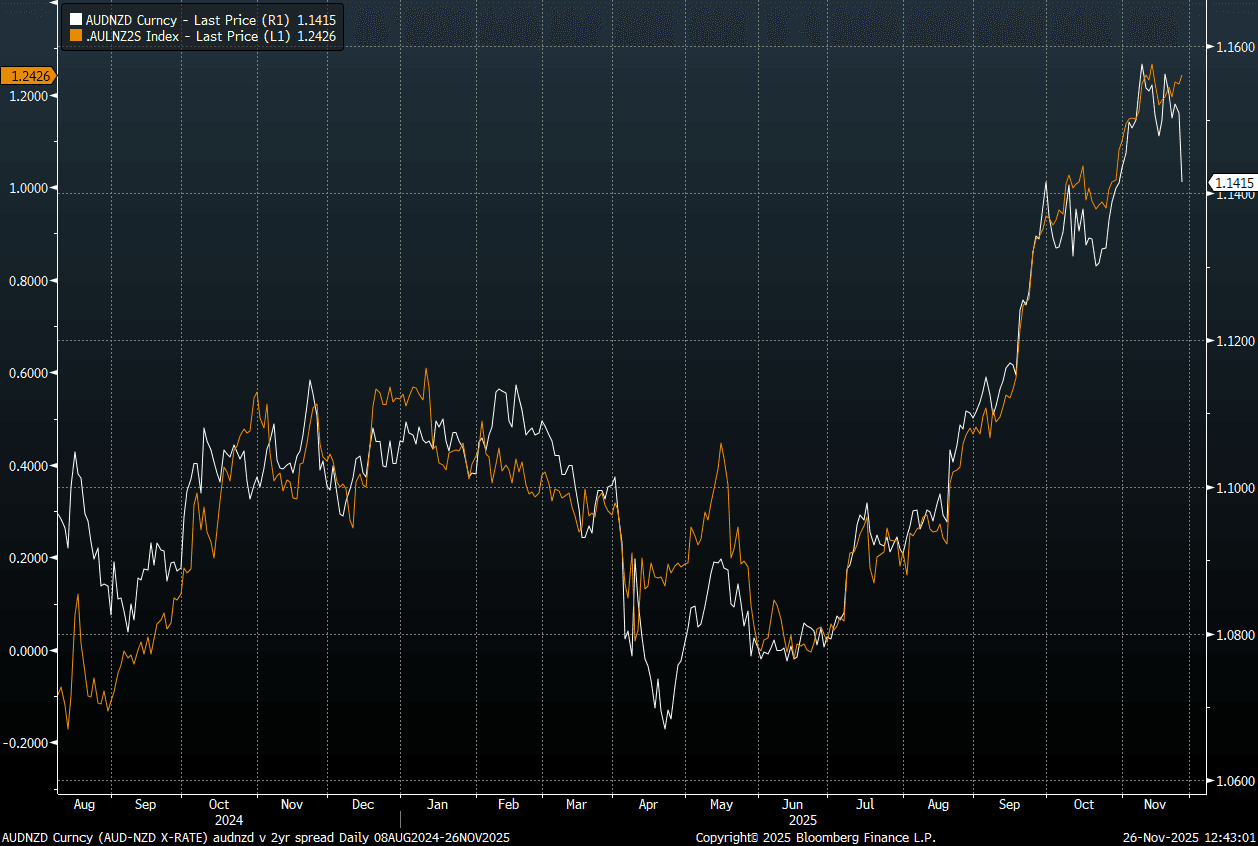

- Still, it is interesting to note the lack of downside in the AU-NZ 2yr swap spread in the aftermath of the RBNZ, see the chart below. If these trends persist, it suggests AUD/NZD dips should be supported. The 1.1250/1.1300 region is likely to generate demand.

- Of course earlier we also had the stronger-than-expected Oct monthly Australia CPI, which has supported local AU rates.

- With the AU–NZ 1-year forward 3-month swap (1Y3M) spread also holding near recent highs, the question of whether rates or FX markets have it right ultimately hinges on the outlook for the AU–NZ cash rate differential. At present, markets expect the AU–NZ 3-month rate spread to narrow by about 25bps over the next 12 months.

- However, we see risks skewed towards the most likely outcome as both the RBA and RBNZ keeping policy rates unchanged. Moreover, the balance of risks around that view leans toward the RBNZ cutting and the RBA hiking.

- The RBNZ maintained its easing bias in November, and Governor Hawkesby noted that the OCR track implies any next move in 2026 is more likely to be a cut than a hike.

- By contrast, the RBA has not adopted a clear stance. Q3 underlying inflation was at the top of the target band, and October’s print was above it. The Bank is watching closely for signs of inflation persistence, and if inflation proves stickier than expected, further tightening could return to the table.

Fig 1: AUD/NZD Spread & AU-NZ 2yr Swap Rate Differential

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CHINA PRESS: CSRC Deploys Key Focuses For Capital Market Reform

The China Securities Regulatory Commission will focus on strengthening the resilience and risk resistance of the capital market, improving the inclusiveness and adaptability of the market system, and deepening market opening to a higher level, Securities Daily reported. Analysts cited by the newspaper said the regulator will need to step up IPO supervision while enhancing the regular delisting mechanism, improve corporate governance, optimise mergers and acquisitions, restructuring, and equity incentive systems, and promote a stronger sense of responsibility among listed companies.

CHINA PRESS: China, U.S. Reach Basic Consensus

China and U.S. delegations have reached basic consensus on arrangements to address their respective trade concerns following two days of talks in Kuala Lumpur, the People’s Daily reported. Both sides will now work out specific details and proceed with their domestic approval processes. Guided by the important consensus reached by the two heads of state in phone conversations earlier this year, officials held candid, in-depth and constructive discussions on several issues. These included U.S. Section 301 measures covering China’s maritime, logistics and shipbuilding sectors, the extension of suspended reciprocal tariffs, fentanyl-related tariffs and law enforcement cooperation, agricultural trade, and export controls, according to the report.

CHINA PRESS: PBOC Likly To Cut RRR In Q4

The People’s Bank of China is likely to cut the reserve requirement ratio in Q4 and resume treasury bond trading timely to support growth, prices, and the real-estate market, National Business Daily reported, citing Wang Qing, analyst at Golden Credit Rating. The PBOC is also expected to use outright reverse repos and medium-term lending facilities to continue injecting medium-term liquidity, limiting the potential for market interest rates to rise, Wang said. On Monday, the Bank announced a CNY900 billion one-year MLF operation, leaving October net medium-term liquidity injection at a high level of CNY600 billion, as it seeks to ensure ample liquidity and stabilise bond market sentiment, the report added.