CANADA DATA: Moderating Core Inflation Trends Keep BOC On Track To Cut Wednesday

August's Canadian CPI data will not present an obstacle to the BOC cutting its benchmark rate on Wednesday by 25bp to 2.50%. Headline CPI printed in line with expectations, ticking up to 1.9% Y/Y after 1.7% in July. In fact, on an unrounded basis, it was on the low side of expectations: 1.85% after 1.73%. And it kept the rate below 2% for a 5th consecutive month.

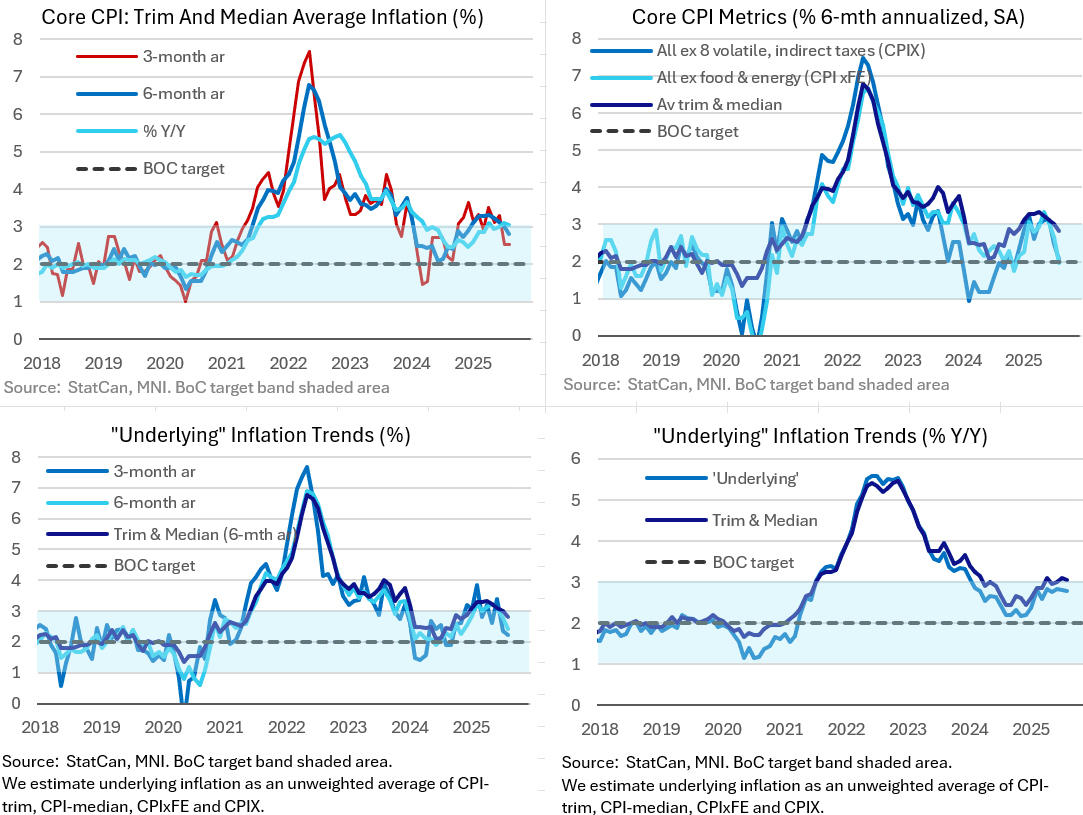

- While that will keep Bank of Canada officials persuaded that price pressures are under control, their closely-watched trim/median average measure continues to show little disinflationary progress, at an in-line-with-expectations 3.05% Y/Y, trim 3.0% and median 3.1% (prior trim/median was revised up to 3.10% from 3.05% prior so technically this was a deceleration).

- Other Y/Y core measures were somewhat mixed. Ex-food and energy inflation (2.44% Y/Y unrounded) was the lowest since March (2.50% prior), while the measure of CPI ex-8 most volatile/indirect taxes was relatively steady at 2.63% (2.57% prior). Ex-mortgage interest CPI was 1.73% Y/Y, up from 1.54% prior for the highest since March.

- When we look at the sequential measures, these too were relatively tame. All-items CPI rose 0.18% M/M on a seasonally-adjusted basis (0.12% prior), with the NSA reading of -0.06% M/M the joint-softest of the year (0.30% prior).

- Ex-food and energy rose 0.13% M/M (0.06% prior). Trim decelerated to 0.19% from 0.23%, with median up to 0.23% from 0.14% (which had been a 12-month low).

- This meant that the trend rates of major aggregates moderated. Ex-food and Energy ticked down to 1.6% on a 3-month moving average annualized rate basis, the lowest since September 2024, with the 6-month at 2.0%. Ex-8 most volatile/taxes was steady at 2.3% on the 3M but fell to a 9-month low 2.1% on a 6M basis. And while the trim/median average 3mma was steady at 2.5% (a joint-10 month low), the 6-month measure was a 9-month low 2.8%, printing below 3% for the first time this year.

- We will turn to the component details in a separate note but the details showed deceleration in shelter and core goods prices (durable goods Y/Y softened), with the only major upside concern being in non-shelter services which ticked higher.

- For the BOC, the OIS rate path now shows a fully-priced September cut, with about 4bp added across the implied cuts though next summer (a 2nd 25bp cut is priced through January 2026, vs March prior to the CPI release).

- The closest we got to a view change post-CPI was RBC, which came into this week as the only major Canadian institution eyeing a hold this week, a view it appears to maintain while acknowledging it's a close call: "The BoC will also have to consider upside inflation risks from sticky core inflation, resilient consumer spending, and planned fiscal stimulus that is likely more effective at addressing the targeted economic impact of trade-related disruptions than interest rate cuts. Today’s inflation report does little to sway that assessment, and we continue to think the Bank of Canada’s decision tomorrow will be a close call between a 25 basis point cut to the overnight rate and a hold.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 10-YEAR TECHS: (U5) Follows Fade in Treasuries

- RES 3: 96.501 - 76.4% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 2: 96.207 - 61.8% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 1: 95.960 - High Apr 7

- PRICE: 95.710 @ 15:17 BST Aug 15

- SUP 1: 95.415/95.300 - Low May 15 / Low Jan 14

- SUP 2: 95.275 - Low Nov 14 (cont) and a key support

- SUP 3: 94.707 - 1.0% 10-dma envelope

Aussie 10-yr futures received a boost from the US Treasury rally that followed both the recent poor NFP print as well as Tuesday’s inflation number. While this impact faded into the close of the week, 10-year futures remain toward the top end of the recent range. To the upside, next resistance is at 96.207, a Fibonacci retracement point. Next support undercuts at 95.420 (pierced), the Feb 13 low, ahead of 95.275, the Nov 14 low and a key support. Clearance of this level would strengthen a bearish condition.

FOREX: USD Index Pinned to 50-dma as Putin Shakes Hands with Trump

- USD slipped against all others Friday, with a poor set of retail sales and Uni of Michigan sentiment numbers meeting a higher-than-expected import price index to further stimulate concerns over a stagflarionary phase in the US economy. The USD Index trades either side of the 50-dma which, notably, has begun to flatten out after maintaining a solid downtrend throughout 2025.

- JPY is the strongest currency in G10, extending the breakout and bearish conclusion of the consolidation phase in USD/JPY. Recent weakness puts the price through support drawn off the early August lows as well as 146.71, a key retracement. Price action this week marks a full reversal of the previously overbought condition, keeping the downside argument in focus.

- Anticipation ahead of the Putin-Trump meeting has reached fever pitch. Footage showing the Presidents shaking hands in Alaska has helped ease concerns over a hostile meeting, but it's the outcomes that will matter to markets - particularly as equities hold at alltime highs. Any signs of progress toward a ceasefire would be warmly received by risk sentiment - although both Trump and Putin cautioned against a optimistic outcome in comments to press.

- We noted earlier in the week the pressure building on USD/HKD, with price action not matching the pattern of HKMA intervention. That move extended overnight, and is still building at typing, putting spot down to new pullback lows of 7.8119 shortly after the European open. Overnight swap rates have surged further still Friday (hitting 1.7% at typing), well ahead of the 0.3% prevailing rate mid-week and should continue to support a recovery in HIBOR fixes ahead. Today's 1m HIBOR fixed higher by 41bps, hitting 1.45% for the highest fix since mid-May. It's these factors that should work against the HKD carry trade (selling HKD, buying USD), evident in the further tightening of the HKD forward discount today: down 975 points from as high as 1270 this month.

- Focus in the coming week shifts to Jackson Hole and Powell's comments on Friday. With the September meeting still in flux - any conviction toward tipping the board toward a rate cut at the next FOMC will be carefully watched, but it's a hawkish outturn that could be more consequential for markets, as OIS prices a near 90% chance of easing on September 17th.

MNI: US TSY TICS NET FLOWS IN JUN +$77.8B

- MNI: US TSY TICS NET FLOWS IN JUN +$77.8B

- US TSY TICS NET L-T FLOWS IN JUN +$150.8B