MNI US OPEN - US Government Shutdown Closes In on Record

EXECUTIVE SUMMARY

- WHITE HOUSE SAYS US TO PAUSE PORT FEES ON CHINA SHIPS NEXT WEEK

- ECB’S NAGEL SAYS OUTLOOK HOLDING BUT OPTIONS OPEN IN DECEMBER

- REEVES TARGETS UK RICH WITH EXIT, MANSION TAXES

- MNI RBA PREVIEW - CPI OUTLOOK KEY TO RATES

Figure 1: EUR front-end retains easing bias, but bar to another cut has been raised

NEWS

US/CHINA (BBG): White House Says US to Pause Port Fees on China Ships Next Week

The US is expected to suspend port fees for a year on China-linked vessels starting next week, as the two countries deescalate a maritime contest that had become a sticking point in the trade war. From Nov. 10, the US will pause measures designed to combat China’s shipping dominance, the White House said in a fact sheet. Meanwhile, Beijing said it would suspend the countermeasures it imposed in retaliation.

US/CHINA (BBG): White House Says China Set to Restart Some Metals Exports to US

China agreed to allow US-bound exports of three critical metals including gallium as part of its trade truce, according to a White House statement, pointing to the removal of bans on such shipments. Flows of gallium, germanium and antimony to the US had been banned by Beijing in December 2024, after having been placed under the country’s export-control regime intended to stop sales for military uses.

US (WSJ): Democrats Urge Trump to Engage in Talks as Shutdown Closes In on Record

Democratic senators again urged President Trump to get involved directly in talks to end the government shutdown as the impasse entered a crucial week, with the lapse set to become the longest ever while pain for American households and travelers is deepening. Lawmakers indicated late last week that they were finally making progress on talks to reopen the government and begin discussions about how to address expiring enhanced Affordable Care Act subsidies, which are set to leave millions of Americans with sharply higher health-insurance bills. Democrats, who have repeatedly blocked a GOP measure to reopen the government, have made talks on healthcare a condition of voting to end the shutdown.

US/VENEZUELA (NYT): Trump Says War With Venezuela Is Unlikely but Suggests Maduro’s Time Is Up

President Trump said he doubted the United States would go to war with Venezuela in an interview aired on Sunday, even as he warned that the days were numbered for the nation’s authoritarian leader, Nicolás Maduro. “I doubt it,” Mr. Trump said of the prospect of war with Venezuela during the interview with CBS’s “60 Minutes.” “I don’t think so. But they’ve been treating us very badly.” Mr. Trump was pressed on the potential escalation against Venezuela as the U.S. military continues an offensive that has included 15 strikes against vessels suspected of smuggling drugs in the Caribbean and Eastern Pacific in the past month.

US/ASIA (BBG): Hegseth Visits Korean DMZ as US Bolsters Security Ties in Asia

US Defense Secretary Pete Hegseth visited the Demilitarized Zone dividing the Korean Peninsula on Monday afternoon, the last stop on his Asia trip aimed at deepening regional security ties to counter China and underscoring Washington’s commitment to Seoul. Hegseth visited the so-called Joint Security Area in Panmunjom with South Korean Defense Minister Ahn Gyu-back, the first joint visit by the two nations’ defense chiefs since 2017.

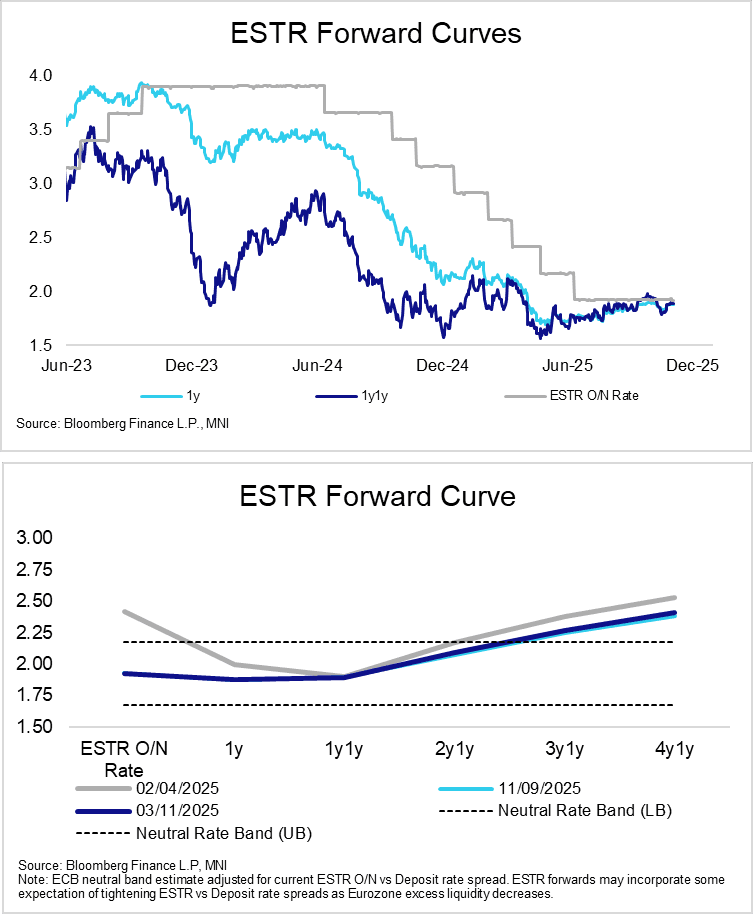

ECB (BBG): ECB’s Nagel Says Outlook Holding But Options Open in December

Euro-zone economic data aren’t diverging from the European Central Bank’s outlook but policymakers are keeping their options open, according to Governing Council member Joachim Nagel. There was “absolutely no reason” to change borrowing costs last week, when the ECB kept its deposit rate at 2% for a third meeting, the Bundesbank president told the Table Today podcast in an episode released Monday.

ECB (BBG): Kazimir Urges ECB to Keep Guard Up on Lingering Inflation Risks

The European Central Bank must be alert to upside inflation risks and resist the temptation to fine-tune policy, according to Governing Council member Peter Kazimir. The Slovak official pointed to supply-chain uncertainty, energy costs, and surprisingly strong underlying price pressures and earnings gauges in arguing that officials “must recognize the presence of lingering upside risks.”

UK (BBG): Reeves Targets UK Rich With Exit, Mansion Taxes Considered

An exit charge for wealthy Britons leaving the country and increased levies on expensive homes are on a long-list of possible tax increases being considered by Chancellor of the Exchequer Rachel Reeves ahead of the budget. Treasury officials have drawn up options for dozens of possible hikes to help Reeves fill a fiscal hole of as much as £35 billion ($46 billion) on Nov. 26, only some of which she will eventually proceed with, according to people familiar with the matter. They cautioned that the chancellor hasn’t decided which tax rises she’ll pick. She would only do so once she receives the final fiscal forecast from her budget watchdog and has a clear picture of how much revenue she needs to raise, they said.

FRANCE (BBG): France’s Lecornu Takes New Approach to Survive Budget Clash

The French government will begin closed-door talks with lawmakers this week in a bid to salvage a budget from a bitter, slow-moving parliamentary debate that risks toppling Prime Minister Sebastien Lecornu. The premier has asked his ministers to invite representatives of different parties as a part of a fresh attempt to agree on “broad principles” for next year’s budget, away from the partisan pressures of the fractured National Assembly. According to his office, he’ll meet with heads of political groups from the house on Monday.

MNI RBA PREVIEW - NOVEMBER 2025: CPI Outlook Key to Rates

The Q3 trimmed mean print at 3.0% y/y up from 2.7% and at the top of the 2-3% target band was a "material miss" for the RBA and meant that the Board is now highly likely to leave rates at 3.6% at its 4 November decision. The Board is likely to remain highly data dependent and cautious given inflation's renewed shift higher and the emerging domestic recovery but easing labour market conditions. Updated staff forecasts will be released and the underlying inflation path is likely to be the focus to see how far out the return to the 2.5% band mid-point has been pushed out.

CHINA (MNI EXCLUSIVE): China's Real Estate to Stabilise Over Next Five Years

Chinese advisors and analysts share their property market outlook/ On MNI Policy MainWire now, for more details please contact sales@marketnews.com

INDIA (BBG): Indian Central Bank Boosts Dollar Shorts to Rein in Rupee Slide

The Indian central bank’s short dollar book in the offshore derivatives market climbed in September for the first time in seven months, reflecting its efforts to stem the rupee losses. The Reserve Bank of India’s net short forward position — the amount of dollars it has agreed to sell in the future at a predetermined price — rose by $6 billion to $59.4 billion, according to Bloomberg calculations based on the central bank data. The RBI’s intervention isn’t limited to forwards — it has also been selling dollars in the onshore market to support the rupee, traders said Monday.

DATA

EUROZONE DATA (MNI): France Manufacturing Weakness Evident in Multiple PMI Reports

- EUROZONE OCT FINAL MANUF PMI 50.0 (50.0 FLASH, 49.8 SEP)

- GERMANY OCT FINAL MANUF PMI 49.6 (49.6 FLASH, 49.5 SEP)

- FRANCE OCT FINAL MANUF PMI 48.8 (48.3 FLASH, 48.2 SEP)

Although France's manufacturing PMI saw a 0.5pp upward revision relative to the flash, underlying details remain weak. Spain and Italy's reports also highlighted weak demand from France as one driver of poor export order performance. For the Eurozone as a whole, the October reading was bang-on neutral (50.0), in line with the flash. Industrial production was very weak in August, but analysts expect some payback in September. French IP is due on Wednesday while Germany is due on Thursday.

SPAIN DATA (MNI): Solid Oct Manufaturing PMI Driven by Domestic Demand

- SPAIN OCT MANUF PMI 52.1 (51.9 FCAST, 51.5 SEP)

The Spanish manufacturing PMI remains comfortably in expansionary territory. October's report signalled solid domestic demand, though export new orders declined at the fastest pace in 5 months. Softness in export orders signals a continuation of the trend seen in Q3. According to the flash national accounts release last week, goods exports fell 1.3% Q/Q.

ITALY DATA (MNI): Oct Manuf PMI Stronger-than-expected, But Details Mixed

- ITALY OCT MANUF PMI 49.9 (49.3 FCAST, 49.0 SEP)

Although 0.6 points stronger than consensus in October, the Italian manufacturing PMI remains below August's levels. Given the print was essentially neutral, it's not surprising to see mixed details. An uptick in production was offset by declines in new orders and employment. Underlying demand still appears subdued.

UK OCT FINAL MANUF PMI 49.7 (49.6 FLASH, 46.2 SEP) (MNI)

SWITZERLAND DATA (MNI): Light CHF Weakness After October Inflation Softer-Than-Expected

- SWISS OCT CPI -0.3% M/M, +0.1% Y/Y

- SWISS OCT CORE CPI +0.5% Y/Y

Core CPI was 0.5% Y/Y in October, below the 0.7% consensus and prior. Headline inflation was 0.1% Y/Y (vs 0.3% cons, 0.2% prior). A reminder that the SNB's latest conditional inflation forecast for Q4 2025 is 0.4%. Imported inflation looks soft again, falling 1.3% Y/Y (vs -0.9% in September, -1.3% in August). Food and non-alcoholic beverage inflation fell 0.5% Y/Y (vs -0.8% prior), while goods inflation was -1.6% for the second consecutive month.

CHINA DATA (MNI): Oct RatingDog China Mfg. PMI Falls on Softer Output

- CHINA OCT RATINGDOG MANUFACTURING PMI 50.6 VS 51.2 IN SEP

China's RatingDog manufacturing PMI, previously known as the Caixin manufacturing PMI, came in at 50.6 in October, down from September's 51.2, staying in the expansionary zone above the 50 mark for the third month, due to a softer rise in output linked to a slowdown in new order growth, the publisher said on Monday. The sub-indices for both demand and production slowed, though production-related sub-indices remained in expansion territory. The new export order sub-index fell sharply into contraction territory on heightened trade uncertainty in October, as market concerns about weakening exports persisted.

TURKEY DATA (MNI): Monthly CPI Inflation Below Expectations at +2.55% in October

- TURKEY OCT CPI +2.55% M/M

Monthly CPI inflation came in below expectations in October, up 2.55% M/M (Est: +2.80%; Prior: +3.23%), translating to +32.87% Y/Y (Est: +33.20% Y/Y; Prior: +33.29%) and marking the lowest for the annual series since 2021. The data will provide a boost to the central bank who are expected to lift its year-end inflation estimates at a presentation on Friday. Officials currently place headline CPI between 25-29% by the end of the year, though market expectations are closer to 30%.

AUSTRALIA DATA (MNI): Ex Alcohol & Tobacco, Q3 Consumer Spending Robust

September household spending was softer than expected rising 0.2% m/m to be up 5.1% y/y after a downwardly-revised 4.9% y/y. Q3 consumption volumes rose 0.2% q/q, the lowest rate since Q3 2024 but the fifth consecutive quarterly rise. Growth continued to recover rising 2.7% y/y, the highest since Q1 2024 but pressured by contracting alcohol & tobacco expenditure. The data point to a continued gradual recovery in private consumption. While the RBA is widely expected to be on hold this week, its consumption forecasts will be monitored for upward revisions.

AUSTRALIA SEP BUILDING APPROVALS +12% M/M, +15.3% Y/Y (MNI)

RATINGS: Positive for Italy & Portugal at Scope, EFSF to Negative at Moody's

Rating reviews of note from after hours on Friday include:

- Fitch affirmed Luxembourg at AAA; Outlook Stable

- Moody's affirmed Canada at Aaa, outlook stable

- Moody's affirmed the European Financial Stability Facility (EFSF) at Aaa, outlook changed to negative from stable

- Morningstar DBRS confirmed Luxembourg at AAA, Stable Trend

- Scope Ratings affirmed Italy at BBB+; Outlook changed to Positive

- Scope Ratings affirmed Portugal at A; Outlook changed to Positive

FOREX: ISM Data in Focus as Shutdown Drags into Another Week

- The US ISM manufacturing print takes focus Monday, with the dearth of official US government data meaning private sector data takes precedent. The US government shutdown enters a new week, with Democrats appealing to Trump directly to intervene and pressure lawmakers into a sustainable compromise - but there remains little expectation of a near-term resolution. As a result, markets expect the shutdown to persist for at least a few more weeks.

- AUD trades a little firmer Monday, keeping a technical bull cycle in play for AUDUSD as Tuesday's RBA decision looms. The Q3 trimmed mean CPI print at 3.0% y/y was at the top of the 2-3% target band, a "material miss" for the RBA, which reinforces the likelihood of rates being held at 3.6% tomorrow. Indeed, RBA-dated OIS pricing implies almost no chance of a cut, with just a 2% probability assigned.

- UK fiscal developments as we approach the Nov 26 budget have been key in shaping the short-term trajectory for sterling, however, there might be greater focus this week on the Bank of England decision, which is far from certain. Indeed, we would categorise our own view of the outcome as 50/50 between a 25bp cut and a hold. If it wasn't for the upcoming budget we would have more certainty that a cut would be delivered given the downside surprises to inflation (particularly as this was driven by food) and the downside surprise to wage growth. Despite Friday’s GBPUSD close, last week’s breach of key 1.3142 support is a meaningful development for the pair, strengthening current bearish conditions. Last week’s low at 1.3097 represents the immediate level of note, however, more meaningful support is at 1.3041, the Apr 14 low. Below here, support appears scant until 1.2709, the April 07 low.

- Meanwhile, ongoing strength for the major equity benchmarks, alongside the domestic narrative in Japan, continue to underpin the AUDJPY rally. The cross traded to fresh 11-month highs last Thursday above the 101 mark, of which a sustained break would place the focus on the US election related highs at 102.41.

EGBS: Recent Pullback In Bund Futures Still Considered Corrective

The 50-day EMA at 129.13 continues to limit downside in Bund futures, meaning the move down that started on Oct 17 is still considered corrective for now. A clear break of the 50-day EMA would signal scope for a deeper retracement towards 128.92 (61.8% retracement of the Sep 25 - Oct 17 bull leg).

- The EU will sell up to E6bln of 6/10/30-year EU-bonds at 1030GMT. Presence of this supply may be limiting recoveries in Bund futures this morning.

- German yields are up to 1bp higher across the curve, with a marginal bear flattening bias noted.

- With European equity futures up 0.6% on the session, 10-year EGB spreads to Bunds are up to 1bp narrower. French budget negotiations remain an area of focus for the OAT/Bund spread.

- Earlier comments suggest ECB’s Simkus has turned slightly less dovish in recent weeks. We had suspected this may be the case after his remarks on Friday were a little less supportive of a December cut than prior to the ECB’s October decision.

- The Eurozone October manufacturing PMI confirmed flash estimates at 50.0. France remains a point of sluggishness.

- ECB speak is due from Lane, Escriva and Kocher later today. The US calendar is headlined by the ISM manufacturing survey and Treasury Marketable Borrowing estimates ahead of Wednesday’s refunding announcement.

GILTS: Off Lows, BoE & Budget Continue to Dominate Headlines

Gilts have recovered from session lows.

- A move away from session highs in crude oil futures provided background support.

- Futures +7 at 93.69. Initial support and resistance located at 93.15 & 93.96, with the technical trend structure remaining bullish.

- Yields essentially unchanged on the day. October lows untested across the curve.

- Bulls haven’t managed to push 10-Year yields meaningfully below 4.40%.

- UK headline flow remains focused on this month’s Budget: In summary, a "settling-up charge", housing taxes, energy VAT reduction and CGT death exemption removal are amongst the major topics covered (see earlier bullet “UK FISCAL: Weekend media updates on the Budget” for more).

- GBP STIRs little changed vs. late Friday levels.

- SONIA futures flat to +1.5.

- BoE-dated OIS prices ~7bp of easing for this week’s BoE decision, 16.5bp through December and 31.5bp through February.

- The bulk of the dovish move that followed the latest CPI release has held, after Dec ’25 MPC pricing hit the most dovish level seen since early August

- We would categorise our own view of this week’s meeting as 50/50 between a 25bp cut and a hold. If it wasn't for the upcoming Budget we would have more certainty that a cut would be delivered given the downside surprises to inflation (particularly as this was driven by food) and the downside surprise to wage growth.

- Note that a GBP550mln sale from the long bucket of the BoE’s APF portfolio is due this afternoon.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Nov-25 | 3.897 | -7.3 |

Dec-25 | 3.805 | -16.5 |

Feb-26 | 3.654 | -31.5 |

Mar-26 | 3.592 | -37.7 |

Apr-26 | 3.479 | -49.1 |

Jun-26 | 3.448 | -52.1 |

Jul-26 | 3.386 | -58.3 |

Sep-26 | 3.371 | -59.8 |

EQUITIES: Trend Structure in Eurostoxx Bullish After Last Week's Cycle Highs

The trend structure in Eurostoxx 50 futures remains bullish. Last week’s fresh cycle highs reinforces a bull theme and the move higher maintains the rising price sequence of higher highs and higher lows. Note too that moving average studies are in a bull-mode position, highlighting a dominant medium-term uptrend. Sights are on 5777.41, a Fibonacci projection. First support lies at 5648.93, the 20-day EMA. The trend condition in S&P E-Minis is unchanged, it remains bullish and the latest pullback appears corrective. The fresh cycle high last week confirms a resumption of the primary uptrend and maintains the bullish price sequence of higher highs and higher lows. Sights are on 6974.04 next, a Fibonacci projection point. Initial firm support to watch lies at 6795.74, the 20-day EMA. Key pivot support lies at 6690.58, the 50-day EMA.

- In China the SHANGHAI closed higher by 21.731 pts or +0.55% at 3976.521 and the HANG SENG ended 251.71 pts higher or +0.97% at 26158.36.

- Across Europe, Germany's DAX trades higher by 208.43 pts or +0.87% at 24167.35, FTSE 100 higher by 11.02 pts or +0.11% at 9728.73, CAC 40 up 16.98 pts or +0.21% at 8138.78 and Euro Stoxx 50 up 34.94 pts or +0.62% at 5696.86.

- Dow Jones mini up 67 pts or +0.14% at 47789, S&P 500 mini up 23.75 pts or +0.35% at 6897.75, NASDAQ mini up 135 pts or +0.52% at 26139.25.

Time: 10:00 GMT

COMMODITIES: Nearby WTI Future Resistance Levels Remain Exposed

Recent gains in WTI futures appear corrective for now, however, note that price has recently traded through the 50-day EMA, currently at $61.05. The breach of this EMA signals scope for a stronger recovery. A resistance at $62.34, the Oct 8 high, has also been pierced. A clear move through it would expose key resistance at $65.77, the Sep 26 high. First key support and the bear trigger is unchanged at $55.96, the Oct 20 low. A fresh cycle low last week in Gold highlights an extension of the bear cycle that started Oct 20. The retracement since Oct 20 has allowed an overbought trend condition to unwind. The 20-day EMA has been breached, signalling scope for a test of the 50-day EMA, at $3859.1. Clearance of this EMA would strengthen a short-term bear theme. Initial resistance is at $4161.4, the Oct 22 high.

- WTI Crude down $0.04 or -0.07% at $60.92

- Natural Gas up $0.14 or +3.37% at $4.266

- Gold spot up $0.08 or +0% at $4002.66

- Copper down $0.7 or -0.14% at $508.2

- Silver down $0.02 or -0.05% at $48.651

- Platinum up $30.84 or +1.96% at $1604.83

Time: 10:00 GMT

| Date | GMT/Local | Impact | Country | Event |

| 03/11/2025 | 1200/1300 | ECB Lane Lecture In Dublin | ||

| 03/11/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 03/11/2025 | 1445/0945 | *** | S&P Global Manufacturing Index (final) | |

| 03/11/2025 | 1500/1000 | *** | ISM Manufacturing Index | |

| 03/11/2025 | 1500/1000 | * | Construction Spending | |

| 03/11/2025 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 03/11/2025 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 03/11/2025 | 1700/1200 | San Francisco Fed's Mary Daly | ||

| 03/11/2025 | 1830/1330 | BOC Governor fireside chat at The Logic conference | ||

| 03/11/2025 | 1900/1400 | Federal Reserve Governor Lisa Cook | ||

| 04/11/2025 | 0030/0930 | ** | S&P Global Final Japan Manufacturing PMI | |

| 04/11/2025 | 0330/1430 | *** | RBA Rate Decision | |

| 04/11/2025 | 0740/0840 | ECB Lagarde Keynote Speech At Bulgarian National Bank | ||

| 04/11/2025 | 0745/0845 | Budget Balance | ||

| 04/11/2025 | 0945/1045 | ECB Lagarde At Bulgarian National Bank Press Conference | ||

| 04/11/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 04/11/2025 | 1135/0635 | Fed Vice Chair Michelle Bowman | ||

| 04/11/2025 | 1140/1140 | BOE Breeden at International Banking Conference | ||

| 04/11/2025 | 1330/0830 | ** | Trade Balance | |

| 04/11/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 04/11/2025 | 1500/1000 | ** | Factory New Orders | |

| 04/11/2025 | 1500/1000 | *** | JOLTS jobs opening level | |

| 04/11/2025 | 1500/1000 | *** | JOLTS quits Rate | |

| 04/11/2025 | 1500/1000 | ** | Factory New Orders | |

| 04/11/2025 | 2100/1600 | Canada federal budget, release expected just after 4pm EST | ||

| 05/11/2025 | 2200/0900 | * | S&P Global Final Australia Services PMI | |

| 05/11/2025 | 2200/0900 | ** | S&P Global Final Australia Composite PMI |

Note: Due to U.S. government shutdown, some data may be unavailable.