MNI US OPEN - US-China Trade Tensions Flare Up Again

EXECUTIVE SUMMARY

- BESSENT ACCUSES CHINA OF TRYING TO DAMAGE GLOBAL ECONOMY - FT

- CHINA IS MAKING IT HARDER TO GET RARE EARTH MAGNET EXPORT LICENSES - RTRS

- CENSURE MOTIONS AGAINST FRANCE PM GO BEFORE PARL'T ON 16 OCT

- UK LABOUR MARKET DATA BROADLY DISAPPOINTS BUT PAYROLLS REVISED HIGHER

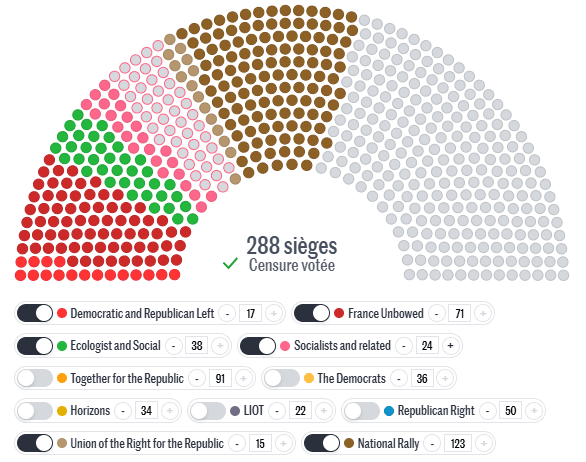

Figure 1: Hypothetical Censure Motion to Remove Lecornu II Gov't

Source: Le Monde

NEWS

US/CHINA (BBG): Bessent Accuses China of Trying to Damage Global Economy: FT

Scott Bessent has ‘accused’ China of trying to hurt the world’s economy after Beijing imposed sweeping export controls on rare earths and critical minerals, the Financial Times reports, citing an interview with the US treasury secretary. Bessent told FT that China’s introduction of the controls reflected problems in its own economy. “If they want to slow down the global economy, they will be hurt the most,” Bessent said on Monday.

CHINA (RTRS): China Is Making It Harder to Get Rare Earth Magnet Export Licenses, Sources Say

Chinese rare earth magnet companies have been facing tighter scrutiny on export license applications since September, sources say, even before Beijing's move last week to expand controls over the critical minerals used in magnets. The lengthier reviews magnet makers face raise questions about whether China, the top global supplier, is seeking to throttle back magnet shipments, contrary to its commitment to speed up exports in a trade truce with the U.S. in May, to further tighten its grip on the products essential in military and commercial technology.

US/CHINA (RTRS): US, China Roll Out Tit-For-Tat Port Fees, Threatening More Turmoil at Sea

The United States and China on Tuesday began charging additional port fees on ocean shipping firms that move everything from holiday toys to crude oil, making the high seas a key front in the trade war between the world's two largest economies. China said it had started to collect the special charges on U.S.-owned, operated, built, or flagged vessels but clarified that Chinese-built ships would be exempted from the levies. In details published by state broadcaster CCTV, China spelled out specific provisions on exemptions, which also include empty ships entering Chinese shipyards for repair.

US/CHINA (BBG): China Hits Back at US on Shipping With Hanwha Curbs, Probe

China sanctioned the US units of a South Korean shipping giant and threatened further retaliatory measures on the industry, the latest in a series of tit-for-tat moves as Beijing and Washington jockey for leverage before expected trade talks. The sanctions, targeting five US units of Hanwha Ocean Co., helped fuel a slump in global equities on Tuesday as traders dialed back hopes for an easing of tensions between the world’s largest economies. Hanwha Ocean closed down 6.2%, while shares of Chinese shipbuilders rallied.

US/CHINA (BBG): China Keeps US Communication Lines Open as Tensions Flare Up

China has signaled it’s keeping communication channels open with the US after a series of tit-for-tat moves that intensified a confrontation between the world’s two biggest economies. The Ministry of Commerce on Tuesday reiterated “the door is open” to talks even as it defended China’s decision to implement export curbs on rare earths amid escalating trade tensions in recent weeks. Separately, Vice Finance Minister Liao Min, a key member of Beijing’s trade negotiating team who’s in Washington this week, has held a meeting with his counterpart at the US Treasury, according to a person with knowledge of the matter.

US/CHINA (WSJ): How China and the U.S. Are Racing to De-Escalate the Trade War

President Trump is trying to publicly de-escalate tensions with China to soothe markets while privately keeping up pressure on Beijing—a difficult balancing act that is being closely watched by Wall Street. After threatening additional 100% tariffs on Chinese imports starting Nov. 1, Trump in recent days spoke with senior officials, including Treasury Secretary Scott Bessent, about sending a message to the world that the U.S. wants to de-escalate trade tensions with China, according to people familiar with the matter.

FRANCE (MNI): Budget Deficit to Be 4.7-5.0% in 2026; Watchdog Expresses Doubts

The French 2026 budget bill looks for a deficit of 4.7-5.0% next year (down from an expected 5.4% in 2025, 5.8% in 2024), according to the budget watchdog (via Reuters). Before resigning the first time round, PM Lecornu had said that he would target a deficit of 4.7%. His predecessor Bayrou had looked for a 4.6% deficit in 2026 before being

ousted by a no-confidence vote. The French fiscal watchdog notes that Lecornu's 2026 consolidation measures total "over E30bln". This is quite a bit less than the E44bln Bayrou was looking for.

FRANCE (MNI): Censure Motions Against PM Go Before Parl't On 16 Oct; PS Stance Crucial

AFP reports that according to its parliamentary sources, censure motions against PM Sebastien Lecornu's second gov't, put forward by the far-left La France Insoumise ('France Unbowed', LFI) and far-right Rassemblement National ('National Rally', RN), are due to go before the National Assembly on Thursday, 16 October. It is viewed as unlikely that either of these censure motions reaches the required 288 votes to oust Lecornu. In recent censure motions, those put forward by the RN have generally failed to win support from other parties. The LFI motion could win the backing of the RN and its allies. However, even if the LFI motion can get the backing of the RN and its allies, as well as the Communist bloc and the Ecologists, this would amount to 264 deputies, short of the majority threshold.

JAPAN (MNI): Diet to Elect New PM 21 Oct; Intense Negotiations on PM Candidate Ongoing

The chairpersons of the House of Councillors' Diet Affairs Committees from the governing Liberal Democratic Party (LDP) and main opposition Constitutional Democratic Party (CDP) met earlier today and agreed on the convening of an extraordinary session of the National Diet on 21 October (likely to elect a new PM). Negotiations between parties are ongoing, with the LDP looking to secure the backing from the opposition to ensure the election of new party president Sanae Takaichi as PM. However, given the LDP lacks a majority in either chamber, the liberal CDP, libertarian-federalist Japan Innovation Party (Ishin), populist conservative Democratic Party for the People (DPFP), and centrist social conservative Komeito could unite to put their own candidate in the PM's office.

RBA (MNI): RBA Sees Stronger Q3 CPI - Minutes

The Reserve Bank of Australia Board judged that September quarter inflation could be higher than expected and that the combination of stronger inflation and a steady labour market might imply staff had underestimated demand relative to supply, minutes of the September meeting showed Tuesday. The Board agreed that monetary policy was “probably still a little restrictive,” though the degree was uncertain, prior to unanimously deciding to hold the cash rate at 3.6%.

RBNZ (MNI): RBNZ to Adjust LVR Settings

The Reserve Bank of New Zealand will ease mortgage loan-to-value ratio (LVR) restrictions from Dec 1, increasing the share of new lending allowed at higher LVRs, the central bank said in a statement Tuesday. For owner-occupiers, the limit on loans with an LVR above 80% will rise to 25% from 20%, while for investors, the limit on loans with an LVR above 70% will increase to 10% from 5%.

OIL (BBG): IEA Raises Its Estimate for Record Oil Oversupply in 2026

A record oversupply of oil will be bigger than previously estimated and the excess is already starting to build up on ocean going tankers, the International Energy Agency said. World oil supply will exceed demand by almost 4 million barrels a day next year, an unprecedented overhang in annual terms, the IEA said in its latest monthly report. Its predicted surplus is up roughly 18% from last month’s estimate, as the OPEC+ alliance continues to revive output and the outlook for the group’s rivals in 2026 strengthens.

DATA

UK DATA (MNI): Labour Market Data Broadly Disappoints but Payrolls Revised Higher

- UK AUG AWE PRIVATE REGULAR PAY +4.42% 3MO Y/Y (VS +4.66% JUL)

- UK SEP PAYE PAYROLLS TOTAL EMPLOYEES 30.32M (VS 30.33M AUG)

- UK AUG UNEMPLOYMENT RATE 4.83% (VS 4.66% JUL)

Private regular AWE lower than expected, unemployment higher, a smaller 3-month LFS employment employment growth number and lower vacancies. All in all a disappointing UK labour market report - likely increasing the probability that Governor Bailey wants to keep optionality for voting for a Q4 cut. The brighter points were: Public sector bonuses were higher than expected (bringing up the total whole economy pay number) while there were some upward revisions to payroll growth so the 3-month fall in payrolls is only 0.2k (from 38k fall to the 3-months of Aug that was revised to -12.6k).

UK DATA (MNI): Retail Sales Slow Amid Budget Caution, Still Boosted by Food Inflation

BRC Retail Sales data for September posted a 2.3% Y/Y increase, a slowdown from the 3.1% of August, and marginally above the 12-month average of 2.1%. However, it is important to note that the monitor is a value measure and a large proportion of the increase is likely due to inflation. Food sales (the largest contributor) slowed slightly versus August, growing 4.3% Y/Y (vs 4.7% Aug), though the press release notes that "growth in food sales was largely inflationary rather than volume growth".

GERMANY DATA (MNI): Final German September Data Shows Move in Car Fuels

German final September HICP was unrevised from the flash readings at 2.4 Y/Y (2.1% in Aug) and 0.2% M/M. The final reading to CPI was also unrevised at 2.4% Y/Y (2.2% in Aug) and 0.2% M/M whilst core CPI printed at 2.8% Y/Y after three consecutive months at 2.7%. The main conclusions from the flash reading were confirmed. Services accelerated to 3.4% Y/Y (confirming the flash reading), a 0.3pp reacceleration after two consecutive prints at 3.1%, adding 0.13pp to headline inflation in September. Goods inflation meanwhile also accelerated, with a 0.08pp higher contribution to headline, mostly on the back of higher energy amid base effects.

AUSTRALIA DATA (MNI): NAB Survey Shows Recovery Continued & Inflation Stable in Q3

The September NAB business survey showed the gradual recovery in the Australian economy continued. Business confidence rose to 7.3 from 4.3 while conditions were similar to August at 7.6. The Q3 averages though were their highest since Q1 2022 and Q2 2024 respectively, suggesting stronger Q3 GDP growth. While the price/cost components were a bit higher in September, they were little changed in Q3 signalling steady inflation. The data are consistent with activity picking up and concerns that disinflation has stalled, and so with the RBA remaining cautious.

NEW ZEALAND (MNI): Q3 Retail Spend Up On Quarter But Still Soft Consistent With Easing

September retail card transactions fell 0.5% m/m after rising 0.6%, the first negative after three consecutive increases. Annual growth slowed to an anaemic 1.2% y/y signalling that while consumption is off its lows the recovery remains weak making additional RBNZ rate cuts more likely. The extent of further easing including in early 2026 remains highly data dependent though.

FOREX: Higher China Trade Tensions Help Pressure Risk; AUD Slides to New Lows

- Headlines confirming that China were ratcheting higher their controls on exports of rare earths provided a further dose of risk-off Tuesday, with markets clearly growing more concerned that global trade tensions will begin to hinder the global economy outside of just the US and China. Resultantly, AUD is in reverse, with AUDUSD making light work of Friday's lows to print the lowest level since mid-August. This narrows the gap with key support layered between the 0.6415 August 22 low and the 200-dma of 0.6423. Reports that Trump is looking to de-escalate the tensions have failed to help prop up markets.

- Infitting with the higher trade tensions, the USD is bid. The USD Index is yet to rally north of last week's highs, however further weakness in EURUSD would make this an inevitability. 99.563 is the level to watch, through which the dollar is at a new multi-month high.

- Similarly, USDCNH is bid - rate is through the 50-dma of 7.1452, but it's 7.1535 that marks the more salient level. It's worth noting last week's high in USDCNY & USDCNH came the session before the higher-than-expected CNY fix - which helped the course correction back down toward 7.12 in USDCNY.

- Renewed trade pressures have tipped EURUSD and GBPUSD to new pullback lows. GBP was already trading weaker on the back of a slower pace of change for private sector wages - helped reignite outside speculation that the BoE could look to cut rates again this year.

- Focus for the rest of today turns to the beginning of US earnings season, with Blackrock, Citigroup, Goldman Sachs, J&J, JPMorgan and Wells Fargo all due today.

EGBS: 10-Year Bund Yields Threatening to Breach 2.60%

10-year Bund yields are down 3.8bps to 2.599%, just off today’s session low of 2.583%. Bunds have traded in a fairly contained range between ~2.60-2.80% since the start of July. A clear breach of the 2.60% figure would open up a move towards 2.55%, which shields the July 1 low at 2.542%.

- The German curve has bull flattened, with Schatz yields down 3bps and 30-year yields down 4bps. Germany sold E5.5bln of the new 2.00% Dec-27 Schatz this morning. The bid-to-offer ratio (1.07x) was the lowest for a sub-3-year line since August 2023.

- The latest uptick in US-China tensions appears to have driven haven demand in global core FI overnight/this morning. The intraday move higher in German ASWs supports this view.

- Soft signals from this morning’s UK labour market report will also be factoring into the bond bid.

- Bund futures are +35 ticks at 129.75, off session highs of 129.94. A bullish theme remains intact, with initial resistance at 130.05, a Fibonacci retracement point.

- Upside in bonds comes despite today’s heavy sovereign supply calendar. The Netherlands, Italy and Germany have held auctions while the ESM is holding a syndication.

- 10-year EGB spreads to Bunds are biased up to ~1bp wider. French politics are in focus, with PM Lecornu presenting his 2026 budget proposal today. The Government will target a 4.7-5.0% deficit next year (vs 5.4% target this year).

- The October German ZEW survey was weaker than expected, while German September final HICP confirmed flash estimates. The remainder of today’s regional calendar includes ECB speak from Makhlouf, Kocher and Villeroy.

GILTS: Futures Through Key Resistance

Gilts have rallied on the back of the ongoing deterioration in Sino-U.S. trade relations and a soft UK labour market report.

- Futures pierce key resistance at 91.82. Bulls now look to the August 14 high (92.06).

- Yields are 5-7bp lower, 5- to 10-Year zone outperforms.

- 10s on track for the lowest close since mid-August, last 4.590%.

- The syndication of the 5.25% Jan-41 gilt sees the spread set at the tight end of the guidance range, with orderbooks (including JLM interest) topping GBP125bln.

- We pencilled in a sale of GBP4.0-8.5bln, with a bias towards the top end of that range. The bookbuild means that will be easily achievable.

- SONIA futures 0.5-7.5 higher.

- Liquid BoE-dated OIS 2-6bp more dovish on the day, ~9bp of easing now priced through year-end, next 25bp cut fully discounted come the end of the March MPC vs. April in recent weeks.

- GBP 1y1y threatens a move back below the broken downtrend line (3.5469%).

- BoE Governor Bailey will speak at 18:00 London. We will watch closely for any clues surrounding his preferences for the Q4 rate decisions.

- We see Bailey as the key swing voter on the finely balanced MPC.

- He previously pointed to a downside surprise in wage growth being one of his motivations for voting for an August rate cut. However, we aren't sure today’s data will convince him either way.

- Looking ahead, next week’s CPI report will be closely eyed.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Nov-25 | 3.939 | -2.9 |

Dec-25 | 3.881 | -8.7 |

Feb-26 | 3.760 | -20.8 |

Mar-26 | 3.716 | -25.2 |

Apr-26 | 3.623 | -34.5 |

Jun-26 | 3.589 | -37.9 |

Jul-26 | 3.532 | -43.6 |

Sep-26 | 3.517 | -45.1 |

EQUITIES: Recent Pullback for Eurostoxx 50 Futures Considered Corrective For Now

The trend condition in Eurostoxx 50 futures is unchanged, the direction is up and the latest pullback is - for now - considered corrective. The key support zone to monitor is 5552.07 - 5478.12, the area between the 20- and 50-day EMAs. A clear break of the 50-day average would highlight a stronger reversal. On the upside, the bull trigger has been defined at 5689.00, the Oct 2 high. Clearance of this hurdle would confirm a resumption of the uptrend. A sharp sell-off in S&P E-Minis on Friday appears corrective - for now. The contract has found support below the 50-day EMA, currently at 6602.32, and last Friday’s low of 6940.25 has been defined as a key short-term support. Note that moving average studies are in a bull-mode position, highlighting a dominant uptrend. The bull trigger is 6812.25, the Sep 9 high. A breach of this hurdle would confirm a resumption of the uptrend.

- Japan's NIKKEI closed lower by 1241.48 pts or -2.58% at 46847.32 and the TOPIX ended 63.6 pts lower or -1.99% at 3133.99.

- Elsewhere, in China the SHANGHAI closed lower by 24.273 pts or -0.62% at 3865.229 and the HANG SENG ended 448.13 pts lower or -1.73% at 25441.35.

- Across Europe, Germany's DAX trades lower by 196.61 pts or -0.81% at 24190.36, FTSE 100 lower by 10.76 pts or -0.11% at 9432.42, CAC 40 down 55.35 pts or -0.7% at 7879.03 and Euro Stoxx 50 down 39.31 pts or -0.71% at 5529.05.

- Dow Jones mini down 237 pts or -0.51% at 46061, S&P 500 mini down 54.25 pts or -0.81% at 6640.25, NASDAQ mini down 259.75 pts or -1.04% at 24663.

Time: 10:00 BST

COMMODITIES: Strong Start to the Week for Gold Reinforces Bullish Conditions

A bearish theme in WTI futures remains intact. Last Friday’s move down confirmed a resumption of the bear leg - support at $60.40, the Oct 2 low, has been breached. This highlights an extension of the bearish price sequence of lower lows and lower highs and the move down opens $57.50 next, the May 30 low. On the upside, initial key resistance is at $66.42, the Sep 29 high. Clearance of this level would highlight a reversal. A bull cycle in Gold remains intact and this week’s very strong start to the week reinforces current conditions. The move higher maintains the price sequence of higher highs and higher lows. Sights are on the $4200.00 handle, and $4239.7, a Fibonacci projection point. Note that the trend is in overbought territory. A move down would be considered corrective and would allow the overbought set-up to unwind. Support lies at $3862.6, 20-day EMA.

- WTI Crude down $1.34 or -2.25% at $58.16

- Natural Gas down $0.06 or -1.86% at $3.06

- Gold spot up $32.46 or +0.79% at $4141.83

- Copper down $15.3 or -2.97% at $499.4

- Silver down $0.35 or -0.67% at $51.9834

- Platinum up $30.81 or +1.88% at $1665.95

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 14/10/2025 | 1000/0600 | ** | NFIB Small Business Optimism Index | |

| 14/10/2025 | - | *** | Money Supply | |

| 14/10/2025 | - | *** | New Loans | |

| 14/10/2025 | - | *** | Social Financing | |

| 14/10/2025 | - | ECB Lagarde and Cipollone at G20 Meeting | ||

| 14/10/2025 | 1200/1300 | BOE Taylor Remarks and Fireside Chat at University of Cambridge | ||

| 14/10/2025 | 1230/0830 | * | Building Permits | |

| 14/10/2025 | 1245/0845 | Fed Governor Michelle Bowman | ||

| 14/10/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 14/10/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 14/10/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 14/10/2025 | 1610/1210 | BOC Sr Deputy Rogers fireside talk in Vancouver | ||

| 14/10/2025 | 1620/1220 | Fed Chair Jerome Powell | ||

| 14/10/2025 | 1700/1800 | BOE Bailey Fireside Chat at Institute of International Finance | ||

| 14/10/2025 | 1925/1525 | Fed Governor Christopher Waller | ||

| 14/10/2025 | 1930/1530 | Boston Fed's Susan Collins | ||

| 15/10/2025 | 0130/0930 | *** | CPI | |

| 15/10/2025 | 0130/0930 | *** | Producer Price Index | |

| 15/10/2025 | 0430/1330 | ** | Industrial Production | |

| 15/10/2025 | 0600/0800 | *** | Final Inflation Report | |

| 15/10/2025 | 0645/0845 | *** | HICP (f) | |

| 15/10/2025 | 0700/0900 | *** | HICP (f) | |

| 15/10/2025 | 0740/0940 | ECB de Guindos at Single Resolution Mechanism Conference | ||

| 15/10/2025 | 0800/0900 | BOE Ramsden in Panel at Resolution Mechanism Conference | ||

| 15/10/2025 | 0900/1100 | ** | EZ Industrial Production | |

| 15/10/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 15/10/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 15/10/2025 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 15/10/2025 | 1230/0830 | ** | Wholesale Trade | |

| 15/10/2025 | 1230/0830 | ** | Empire State Manufacturing Survey | |

| 15/10/2025 | 1330/0930 | Fed Governor Stephen Miran | ||

| 15/10/2025 | 1545/1645 | BOE Breeden in Panel on Financial Regulation | ||

| 15/10/2025 | 1610/1210 | Atlanta Fed's Raphael Bostic | ||

| 15/10/2025 | 1630/1230 | Fed Governor Stephen Miran | ||

| 15/10/2025 | 1700/1300 | Fed Governor Christopher Waller | ||

| 15/10/2025 | 1735/1335 | Kansas City Fed's Jeff Schmid | ||

| 15/10/2025 | 1800/1400 | Fed Beige Book | ||

| 15/10/2025 | 1800/2000 | ECB de Guindos at Alantra Anniversary Event | ||

| 15/10/2025 | 1800/1900 | BOE Breeden in Panel at Fintech Foundation |