MNI US OPEN - Trump Warns of 10% Tariffs Over BRICS Policies

EXECUTIVE SUMMARY

- TRUMP WARNS OF 10% TARIFF FOR ‘ANTI-AMERICAN’ BRICS POLICIES

- TRUMP SAYS WILL SEND LETTERS, ANNOUNCE TRADE DEALS FROM 12PM ET

- NAGEL CONTINUES TO EXPECT THIRD YEAR OF "MINIMAL GROWTH" IN GERMANY

- MNI RBA PREVIEW - 25BP CUT LIKELY

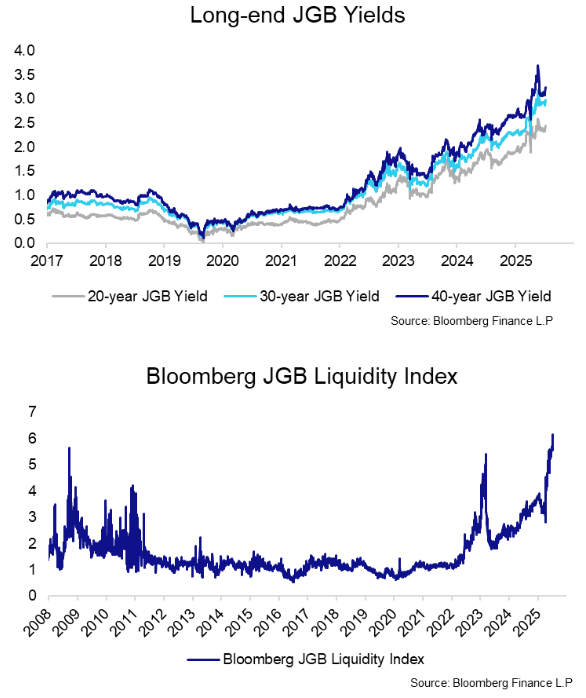

Figure 1: Long-end JGB pressure resumes overnight as election comes into view

NEWS

US (BBG): Trump Warns of 10% Tariff for ‘Anti-American’ BRICS Policies

President Donald Trump said he would put an additional 10% tariff on any country aligning themselves with “the Anti-American policies of BRICS,” injecting further uncertainty into global trade as the US continues to negotiate levies with many trading partners. “Any Country aligning themselves with the Anti-American policies of BRICS, will be charged an ADDITIONAL 10% Tariff,” Trump said in a Truth Social post. “There will be no exceptions to this policy.”

US (BBG): Trump Says Will Send Letters, Announce Trade Deals From 12pm ET

“I am pleased to announce that the United States Tariff Letters, and/or Deals, with various Countries from around the World, will be delivered starting 12:00 P.M. (Eastern) Monday, July 7th,” President Donald Trump says in Truth Social post.

US (NYT): Bessent Says He Expects Trade Deals by This Week’s Deadline

Treasury Secretary Scott Bessent said on Sunday that he was confident the Trump administration would be able to reach deals with some countries before the deadline on Tuesday for steep tariffs would take effect. But he also held out the possibility that the deadline could be extended to Aug. 1 for countries seeking to reach deals. “There’s a lot of foot dragging on the other side, and so I would expect to see several big announcements over the next couple of days,” Mr. Bessent said on CNN’s “State of the Union.” He added, “We’re going to be very busy over the next 72 hours.”

US (NYT): Trump Says Musk Is ‘Off the Rails’ With His Third-Party Effort

President Trump assailed Elon Musk on Sunday night, describing him as “off the rails” after Mr. Musk said he was creating a new political party amid an ongoing rift with the president. “I am saddened to watch Elon Musk go completely ‘off the rails,’ essentially becoming a TRAIN WRECK over the past five weeks,” Mr. Trump wrote on Truth Social on Sunday evening. “He even wants to start a Third Political Party, despite the fact that they have never succeeded in the United States.”

US/ISRAEL (WSJ): Trump and Netanyahu to Meet as New Middle East Tests Loom

Israel and Hamas have resumed indirect talks on a cease-fire in Gaza after months of heavy Israeli military action. Iran, battered by the U.S. and Israeli strikes, is sending signals that it might be willing to resume nuclear negotiations, albeit on its own terms. And the White House is reaching out to Syria’s new government, hoping for improved ties between Damascus and Israel. Trump and Netanyahu’s White House meeting is partly aimed at claiming credit for these shifts and partly to discuss next moves. But the durability and scope of the diplomacy remains in question.

ECB (MNI): Nagel Continues to Expect Third Year of "Minimal Growth" in Germany

ECB's Nagel does not comment on monetary policy in today's speech at the Bank of Estonia in Tallinn - but gives some views on domestic economic conditions and potential reforms in Germany: "The Bundesbank's June 2025 forecast indicates that the German economy is expected to more or less stagnate this year. Factoring in the

stronger-than-expected first-quarter growth figures, a slight annual increase appears possible. However, this would still represent three consecutive years of minimal growth."

UK (The Times): Keir Starmer Faces Fresh Labour Revolt Over Special Needs Support Reforms

Sir Keir Starmer is facing a fresh backbench revolt after ministers refused to guarantee millions of children the legal right to special needs support in school. Bridget Phillipson, the education secretary, said on Sunday that the government was committed to reforming help for children with learning difficulties or disabilities, which at present costs the taxpayer £12 billion a year. However, she failed to promise that parents would continue to have the same legally enforceable rights to ensure that their children receive bespoke support for their needs either in mainstream or special educational schools.

JAPAN (MNI): Fitch Says Debt Risks Contained in S/T, Significant in L/T

Fitch on Japan: "Reflationary dynamics will support a continued decline in Japan's government debt/GDP ratio in the next few years, Fitch Ratings says in a new report. This is despite long-term pressures on debt sustainability from higher interest payments, growing ageing-related costs, as well as increased spending on defence and childcare. Japan's government debt ratio is already significantly below pandemic-era highs".

JAPAN (MNI): LDP-Komeito May Struggle to Hold Onto Upper House Majority - Poll

The latest seat projection opinion polling ahead of the 20 July election for the House of Councillors shows PM Shigeru Ishiba's conservative Liberal Democratic Party (LDP) on course to lose a significant number of seats, and potentially for the governing coalition (alongside the Komeito party) to lose its overall majority in the upper chamber of the Japanese National Diet. The poll for Mainichi Shimbun, carried out 5-6 July, projects the LDP to win between 34 and 46 of the 124 seats up for election. The House of Councillors has 248 seats in total, with half of the seats up for grabs every three years.

MNI RBA PREVIEW - JULY 2025: 25bp Cut Likely

The RBA is widely expected to cut by 25bps at tomorrow's policy meeting. This is the sell-side consensus, albeit with a small number of economists expecting rates to be left on hold. Financial market pricing is also consistent with a 25bps cut. Our bias is also for a 25bps cut, which would take the RBA cash rate to 3.60% (still above neutral rates). If realized this would be 75bps worth of easing delivered so far in this cycle. Data towards the end of June, for May monthly CPI, should give the RBA confidence to cut. Headline inflation was close to the bottom end of the RBA's 2-3% target band, whilst the trimmed mean eased to 2.4%y/y.

TURKEY (MNI): Turkish Prosecutors Launch Probe Into Opposition Leader

Turkish prosecutors launched the probe into CHP Chairman Ozgur Ozel late Sunday on allegations of insulting the president and threating public officials in a speech in which he criticised the detention of the three of the party’s mayors, according to the state-run Anadolu Agency. The probe marks the latest escalation in a months-long campaign against dozens of opposition officials. Lawmakers from the party will hold a closed-door meeting at 14:00BST/16:00 local time this afternoon. The comments from Ozel came after Zeydan Karalar, Muhittin Bocek and Abdurrahman Tutdere - the mayors of Adana, Antalya and Adiyaman respectively - were taken into custody on Saturday.

DATA

EUROZONE DATA (MNI): May Retails Sales Weak as Expected, Non-Food & Fuel Carry Y/Y

- EUROZONE MAY RETAIL SALES -0.7% M/M, +1.8% Y/Y

Eurozone (real) retail sales were overall broadly in line with (weak) expectations in May on a sequential comparison, at -0.7% M/M (-0.6% M/M cons; +0.3% April, revised from +0.1%). Across sectors, all main categories fell: Food, drinks, tobacco -0.7% M/M, non-food products (except automotive fuel) -0.6%, automotive fuel -1.3% - neither of the categories has exhibited a clear directional trend YTD. Also across countries, May weakness appears quite broad-based, with Spain the strongest out of the "big 4" EZ countries at a mere 0.2% M/M.

GERMANY DATA (MNI): May Industrial Production Stronger on Manufacturing, Energy

- GERMANY MAY INDUSTRIAL PRODUCTION 1.2% M/M

German industrial production outperformed expectations in May at 1.2% M/M, compared to consensus of -0.2% following a slight downward revision of April's rate to -1.6% (-1.4% unrevised). On a yearly basis, IP came in at 1.0% (vs -0.3% cons; -2.1% Apr revised, from -1.8% unrevised). This means that the orders and production data from May point in different directions (May orders, published Friday, were weak) - that is not totally uncommon; overall, our reading remains that also taking consensus into consideration, the picture in the sector is arguably brighter than what it was a couple of months ago.

SWEDEN DATA (MNI): Big Upside Surprise in June Flash CPIF Ex-energy

- SWEDEN FLASH JUN CPIF +2.9% Y/Y

June flash inflation report sees a big upside surprise: CPIF ex-energy 3.29% Y/Y: Riksbank 2.86% Y/Y; BBG Consensus 2.9% Y/Y (range 2.8-3.0% Y/Y). 2.47% Y/Y prior CPIF 2.85% Y/Y: Riksbank 2.40% Y/Y; BBG Consensus 2.5% Y/Y (range 2.2-2.5% Y/Y). 2.26% Y/Y prior. EURSEK snaps 0.25% lower on the release, but the cross is off session lows and Friday's low of 11.2366 remains intact. The 20-day EMA presents more important support at 11.1042 today. Unfortunately, the lack of detail in the flash release makes it difficult to read much into the print for now - particularly given volatile components (e.g. package holidays) were pencilled in as the main upside drivers in June.

NORWAY DATA (MNI): Manufacturing IP Consolidates Recent Strength, But Focus on CPI Thurs

Although a serially volatile release, Norwegian manufacturing industrial production has broadly consolidated the rise since October 2024. However, petroleum-related industries remain the clear outperformer since 2022. Positive momentum through 2025 has come despite rates being held at 4.50% until June 19. Guidance that Norges Bank is willing to cut up to two more times this year should provide further support to the mainland industrial economy. However, inflation will (as always) dictate the scope for further easing, keeping main domestic focus on Thursday's June CPI report.

CHINA DATA (MNI): China's Forex Reserves Up USD32.2 Billion in June

MNI (Beijing) China's foreign exchange reserves rose by USD32.2 billion in June, as the U.S. dollar index fell and global financial asset prices generally rose, data by the State Administration of Foreign Exchange showed on Monday. The country's forex reserves, the world's largest, rose 0.98% to USD3.317 trillion last month, slightly higher than market expectation of USD3.313 trillion. The People’s Bank of China increased gold holdings for an eighth consecutive months to a record 73.9 million ounces by the end of June, compared to the previous 73.83 million ounces.

JAPAN DATA (MNI): Japan's May Negative Real Wage Widens

Japan’s inflation-adjusted real wages, a key gauge of household purchasing power, remained negative for the fifth straight month in May, falling 2.9% y/y following April's 2.0% decline, preliminary data from the Ministry of Health, Labour and Welfare showed Monday. The drop marks the steepest decline since September 2023, when real wages also fell 2.9%. Hefty pay increases agreed during spring wage negotiations are gradually being reflected in the data through July, helping narrow the negative wage gap.

AUSTRALIA DATA (MNI): ANZ Job Ads Rise in June, Pointing to Resilient Labor Market

The ANZ June job ads print was +1.8%m/m, after a revised fall of 0.6% in May (originally reported as a -1.2% decline). In y/y terms, jobs ads are -0.4%. At the start of the year we were at -13.7%. This was the best m/m increase for the index since Sep last year. It points to continued resilience in terms of labor market conditions. The chart below plots the ANZ job ads m/m change versus monthly employment growth in Australia.

FOREX: USD Bounce Dragging Key Pairs Off Highs

- The USD's bounce Monday is providing some relief for the USD Index, which now sits 1% above last week's cycle lows to put the currency on a surer footing. As a result, the major pairs are seeing pressure toward the the post-NFP lows - with EUR/USD and GBP/USD challenging 1.1718 and 1.3586 respectively.

- Rates markets are endorsing USD gains here: the US curve is steeper as the global long-end continues to underperform. This backdrop, allied with any deterioration in trade relations between the US and the RoW remains a key market focus, particularly with the fluidity around Trump's approach to tariffs and the suite of reciprocal trade tariff deadlines looming over markets this summer.

- Trump's ire toward BRICS countries has tilted EM FX to underperform. The ZAR underperformed throughout Asia-Pac trade and well through the European morning after the President warned there would be "no exceptions" to a policy of 10% additional trade tariffs on nations that adhere to the BRICS' anti-American policies.

- A correction lower through 1.3563 would be consequential for GBP/USD, and raise the likelihood of a test on the 50-dma support in the near-term. This level has held well and helped define the rally over the course of 2025 - crossing at 1.3477 today. In trend terms, we note that the 50-dma now trades with the largest % premium over the 200-dma since the bounce off lows in 2009. The premium currently sits at ~4.2% vs. the 2009 peak of ~8.2%, mid-Global Financial Crisis.

- The data schedule is few and far between Monday, with no tier 1 releases due until the RBA rate decision overnight. ECB's Holzmann speaks from Vienna at 1400BST.

EGBS: Bunds Inch Towards Session Lows On Crude and Equity Uptick; Support Untested

Bund futures are inching back towards session lows alongside core FI peers, currently -20 ticks at 130.31 (vs an earlier low of 130.19). Support is not seen till the July 3 low and bear trigger at 129.77

- Cross-market cues seemingly remain at the fore as crude oil & Euro Stoxx futures move to fresh session highs.

- Crude has shaken off the latest round of speculation OPEC+ production increases, while broader macro headline flow remains relatively limited.

- German yields are up to 1.5bps higher on the session, with a light steepening bias seen. 10-year EGB spreads to Bunds are little changed.

- Little of note on the macro calendar today – Eurozone May retail sales were slightly weaker-than-expected on a monthly basis (-0.7% Y/Y (vs -0.6% cons), but this was offset by an upward revision to April’s reading. German industrial production was stronger than expected at 1.2% M/M (vs -0.2% prior).

- No new signals from today’s ECB speak – Centeno provided similar comments to his interview with the MNI Policy Team from last week. Nagel did not speak on monetary policy, but noted the weak near-term German growth outlook.

- Trump’s letters surrounding tariff rates (due to be sent at 12:00 NY today) garner much of the interest, although the ongoing fluidity (U.S. willingness to cut deals/moderate tariffs in the past) when it comes to the global tariff backdrop continues to limit visibility on the matter.

GILTS: Yields a Little Lower, Focus on Macro & Cross-Market Cues

Cross-asset cues dominate, with gilts sticking to tight ranges after the recovery from Wednesday’s low through the latter half of last week.

- Oil has recovered from session lows, limiting any rallies.

- Futures last +11 at 92.49.

- Initial support and resistance (92.12 & 92.79) untouched.

- Yields 1-2bp lower, modest steepening of the curve. Cycle highs in 2s10s and 5s30s untouched.

- Macro focus centred on President Trump’s tariff letters, which will be sent to countries today (12:00 NY).

- Domestically, focus remains on the fragile fiscal situation with last week’s events underscoring the difficulty of enacting meaningful public spending cuts and increasing the odds of tax hikes in the Autumn (a negative for GDP growth).

- There are increasing odds that Reeves will have to hike at least one of the big three taxes (national insurance, income tax & VAT).

- Front end pricing little changed on the day, 21bp cuts priced for August, 28bp through September, 46bp through November and 54bp through year-end.

- We continue to look for cuts in August and November at this stage, with risks skewed dovishly.

- Further softening in the labour market presents the most likely dovish catalyst, with fresh developments on that front likely needed to promote the pricing of a more aggressive easing cycle through year-end.

- Monthly economic activity data (Friday) headlines this week’s local data calendar, while BoEspeak will come via Breeden on Thursday.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Aug-25 | 4.005 | -21.3 |

Sep-25 | 3.937 | -28.1 |

Nov-25 | 3.762 | -45.6 |

Dec-25 | 3.675 | -54.2 |

Feb-26 | 3.542 | -67.6 |

Mar-26 | 3.510 | -70.7 |

EQUITIES: E-Mini S&P Trend Signal Unchanged and Bullish

Short-term trend signals in Eurostoxx 50 futures remain bearish, however, the recovery from the Jun 23 low still appears to be a reversal and the contract is holding on to its most recent gains. Price has pierced both the 20- and 50-day EMAs. A clear break of both averages would strengthen a reversal theme. This would open 5486.00, the May 20 high and bull trigger. On the downside, a breach of 5194.00, the Jun 23 low, reinstates a bearish theme. The trend condition in S&P E-Minis is unchanged, it remains bullish. Resistance at 6128.75, the Jun 11 high, has recently been breached. The break confirmed a resumption of the uptrend that started Apr 7. This has been followed by a breach of key resistance and a bull trigger at 6277.50, the Feb 21 high. Sights are on 6356.12, a Fibonacci projection. Key support is at the 50-day EMA - at 6000.73.

- Japan's NIKKEI closed lower by 223.2 pts or -0.56% at 39587.68 and the TOPIX ended 16.23 pts lower or -0.57% at 2811.72.

- Elsewhere, in China the SHANGHAI closed higher by 0.808 pts or +0.02% at 3473.127 and the HANG SENG ended 28.23 pts lower or -0.12% at 23887.83.

- Across Europe, Germany's DAX trades higher by 85.68 pts or +0.36% at 23870.98, FTSE 100 lower by 9.93 pts or -0.11% at 8813.08, CAC 40 down 6.09 pts or -0.08% at 7690.49 and Euro Stoxx 50 up 6.13 pts or +0.12% at 5294.88.

- Dow Jones mini down 74 pts or -0.16% at 45024, S&P 500 mini down 29 pts or -0.46% at 6295.5, NASDAQ mini down 141.25 pts or -0.61% at 22921.5.

Time: 10:00 BST

COMMODITIES: Gold Continues to Hover Just Above Support at 50-Day EMA

WTI futures maintain a softer tone following the reversal from the Jun 23 high. Recent gains appear corrective. Support to watch is the 50-day EMA, at $64.84. It has been pierced, a clear break of it would signal scope for a deeper retracement. This would expose $58.87, the May 30 low. Initial resistance to watch is $71.20, the 50.0% retracement of the Jun 23 - 24 high-low range. Key resistance is at $78.40, the Jun 23 high. Recent weakness in Gold resulted in a breach of the 50-day EMA, and a trendline drawn from the Dec 30 ‘24 low and connected to the Feb 28 low. A clear break of both trend tools would signal scope for a deeper correction, and open $3245.5, May 29 low. Note that the latest recovery highlights a possible false trendline break. A resumption of gains would refocus attention $3451.3, the Jun 16 high. The bear trigger is $3248.7, the Jun 30 low.

- WTI Crude down $0.1 or -0.15% at $66.87

- Natural Gas down $0.11 or -3.34% at $3.295

- Gold spot down $27.21 or -0.82% at $3309.57

- Copper down $12.85 or -2.5% at $501.45

- Silver down $0.33 or -0.89% at $36.6015

- Platinum down $34.26 or -2.45% at $1363.77

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 07/07/2025 | - | ECB Lagarde and Cipollone In Eurogroup Meeting | ||

| 07/07/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 07/07/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 08/07/2025 | 2350/0850 | Balance of Payments | ||

| 08/07/2025 | 0430/1430 | *** | RBA Rate Decision | |

| 08/07/2025 | 0500/1400 | Economy Watchers Survey | ||

| 08/07/2025 | 0600/0800 | ** | Trade Balance | |

| 08/07/2025 | 0645/0845 | * | Foreign Trade | |

| 08/07/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 08/07/2025 | 1000/0600 | ** | NFIB Small Business Optimism Index | |

| 08/07/2025 | - | ECB de Guindos At ECOFIN Meeting | ||

| 08/07/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 08/07/2025 | 1400/1000 | * | Ivey PMI | |

| 08/07/2025 | 1500/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 08/07/2025 | 1530/1130 | ** | US Treasury Auction Result for 52 Week Bill | |

| 08/07/2025 | 1700/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 08/07/2025 | 1900/1500 | * | Consumer Credit |