MNI US OPEN - Trump Wants Putin Meeting 'Soon'

EXECUTIVE SUMMARY

- TRUMP SAYS PUTIN MEETING WILL HAPPEN "AS SOON AS WE CAN SET IT UP”

- FED’S BOSTIC SAYS HE SEES ONE RATE CUT THIS YEAR, NO RECESSION

- JAPAN AIMS FOR CURRENCY TALKS WITH US BASED ON PAST DIALOGUE

- BOJ’S NAKAMURA SAYS APPROPRIATE TO KEEP POLICY STEADY FOR NOW

- JAPAN Q1 GDP POSTS 1ST CONTRACTION IN 4 QTRS

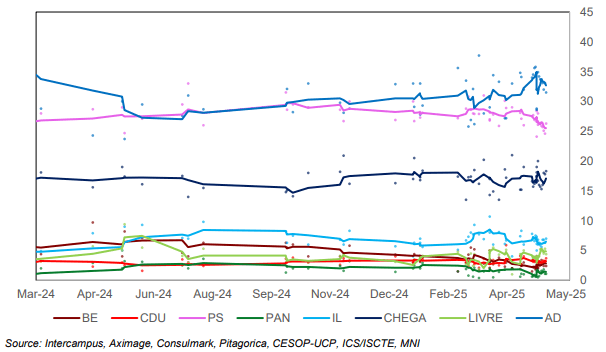

Figure 1: Portugal Legislative Election Opinion Polling (Short-Term), % and 5-Poll Moving Average

NEWS

MNI POLITICAL RISK ANALYSIS: Portugal Election Preview

Portugal holds a snap legislative election on 18 May following the successful parliamentary vote of no confidence against the minority government of Prime Minister Luís Montenegro in March. A fractured political landscape makes one party winning a majority in the Assembly of the Republic an unlikely scenario. As such, the formation of a coalition or minority government after the election is set to be required. There is significant focus on the postelection negotiations, given the prospect that the right-wing Chega is involved in supporting a minority administration for the first time.

MNI POLITICAL RISK ANALYSIS: Poland Election Preview

Poland will hold the first round of the presidential election on May 18, with the widely anticipated run-off between top two candidates expected on June 1. The head of state has many ceremonial functions, but is also equipped with a strong veto power, with the bar for its overruling by parliament set relatively high. Opinion polling and betting market data suggest that government ally Rafał Trzaskowski holds a lead over his closest rival Karol Nawrocki. Trzaskowski’s victory would give the government more leeway to implement its agenda, while Nawrocki’s win would prolong the existing political deadlock.

RUSSIA/UKRAINE (NYT): Peace Talks Between Russia and Ukraine to Begin Amid Doubt and Chaos

Ukrainian and Russian negotiators were poised to meet Friday for the first direct peace talks between their nations since the beginning of the war, after days of confusion and theatrics. The negotiations are not expected, even by foreign leaders like President Trump who called for them, to yield significant results. But the meeting itself is a win for President Vladimir V. Putin of Russia, who refused to agree to a battlefield cease-fire that Ukraine and almost all of its Western backers had sought as a precondition for talks.

US/RUSSIA (MNI): Summary of Trump's Comments in UAE

US President Donald Trump has delivered remarks to the press in Abu Dhabi, on a range of issues, to conclude his "incredible" four-day trip to the Middle East. Trump says he will go straight home after his stop in the UAE, nixing the possibility of an additional stop in Turkey to help facilitate peace talks between Ukraine and Russia. He says, "we'll see what happens with Russia and Ukraine." Trump later adds on a ceasefire, "we're going to get it done" and says he will meet with Russian President Vladimir Putin "as soon as we can set it up". Trump hints at some foreign policy announcements in the coming 2 or 3 weeks, noting: "We're looking at Gaza and we're going to get that taken care of". While discussion of Israel has been conspicuously absent from Trump's trip, Secretary of State Marco Rubio held a call with Prime Minister Netanyahu yesterday, affirming the US' 'ironclad' support for Israel's security.

US (BBG): Trump Says US Will Set Tariff Rates for Other Nations in Weeks

President Donald Trump said he would set tariff rates for US trading partners “over the next two to three weeks,” saying his administration lacks the capacity to negotiate deals with all of its trading partners. Trump said Friday that Treasury Secretary Scott Bessent and Commerce Secretary Howard Lutnick “will be sending letters out essentially telling people” what “they’ll be paying to do business in the United States.” “I think we’re going to be very fair. But it’s not possible to meet the number of people that want to see us,” the president said during a meeting with business executives in the United Arab Emirates.

FED (BBG): Fed’s Bostic Says He Sees One Rate Cut This Year, No Recession

Federal Reserve Bank of Atlanta President Raphael Bostic said he expects the US economy to slow this year but not fall into recession, and reiterated that he sees one interest-rate cut in 2025. Bostic said economic growth could come in at 0.5% or 1% this year, as uncertainty and concerns about the outlook weigh on consumers. Fluctuating trade policy has also made businesses more reluctant to make important decisions, Bostic said. “I have one cut for the year,” Bostic said during a May 14 interview for Bloomberg’s Odd Lots podcast. “In part, it’s because I think the uncertainty is unlikely to resolve itself quickly.”

US/CHINA (BBG): China Hopes US Firms to Help Boost Sino-US Ties, Han Zheng Says

China hopes US business community to play a greater role in promoting US-China relations, Vice President Han Zheng says in a meeting with Invesco Chairman Richard Wagoner. Han says he welcomes Invesco to step up cooperation with the country, the Xinhua report adds. China and US have extensive common interests and broad space for cooperation, Han adds.

US/CHINA (FT): Trump Administration Considers Adding Chinese Chipmakers to Export Blacklist

The Trump administration plans to put a number of Chinese chipmaking companies on an export blacklist, but some officials want to delay the move to avoid hurting efforts to strike a long-term trade agreement with China. The commerce department has compiled a list of Chinese companies — including memory chipmaker ChangXin Memory (CXMT) — to add to the “entity list,” according to five people familiar with the matter. Several of the people said the Bureau of Industry and Security, the commerce department arm that oversees export controls, had drafted a list that also includes the subsidiaries of Semiconductor Manufacturing International Corp, China’s biggest chipmaker, and Yangtze Memory Technologies Co, its largest memory chipmaker. SMIC and YMTC are already on the list.

US/JAPAN (BBG): Japan Aims for Currency Talks With US Based on Past Dialogue

Japanese Finance Minister Katsunobu Kato said he’ll seek another opportunity to talk with his US counterpart Scott Bessent next week to discuss currency matters, building on their dialogue last month. “We confirmed that currency rates should be determined by the market, and that excessive volatility can harm the economy and financial stability,” Kato said Friday at a post-cabinet meeting press conference, referring to his April bilateral meeting with the US Treasury secretary in Washington. “I’m looking for a chance to speak with Bessent again next week to discuss these points, if the circumstances allow,” Kato added.

BOJ (BBG): BOJ’s Nakamura Says Appropriate to Keep Policy Steady for Now

Bank of Japan Board Member Toyoaki Nakamura says it’s appropriate to keep monetary policy unchanged for the time being as the bank needs to carefully monitor the impacts of US tariffs. The bank needs to watch developments over corporate profits, capital spending and wage increases, Nakamura says in a speech in Fukuoka. The BOJ needs to conduct monetary policy cautiously as uncertainties are extremely high.

BOJ (MNI INTERVIEW): Ex-BOJ Sakurai Sees Next Hike After April 2026

MNI discusses the BOJ's policy strategy with a former board member. On MNI Policy MainWire now, for more details please contact sales@marketnews.com.

US/S.KOREA (MNI): No FX Discussions Between Korean Minister & U.S. Trade Rep

South Korean Trade Minister Heong notes that FX matters didn't come up in the meeting with his U.S. TR Greer. A reminder that the KRW has recently benefitted from a BBG report pointing to the two countries discussing FX policy earlier in May, with the prior meeting apparently generating an agreement to share a mutual understanding of principles when it comes to forex, as well as indicating "continued discussions on related policy".

US/INDIA (BBG): India Examining US Request to Abolish Curbs on Ethanol Imports

India is reviewing a US request to lift restrictions on ethanol imports as it negotiates a wider trade deal with Washington to avoid punitive tariffs. US negotiators want the South Asian country to allow shipments of the biofuel for blending with gasoline, according to people familiar with the matter, a change from current rules that promote domestic supply and permit overseas purchases of ethanol only for non-fuel use.

ECB (BBG): ECB Now ‘Relatively Close’ to Terminal Rate, Kazaks Tells CNBC

European Central Bank Governing Council member Martins Kazaks said cuts in euro-zone borrowing costs are nearing their end-point if the base case for inflation returning to 2% this year materializes. Speaking Friday to CNBC, the Latvian official said that there may still be a “couple” of reductions in the deposit rate this year from its current level of 2.25%. But he cautioned that with the global trade situation remaining unclear, policymakers shouldn’t hurry. Within the ECB’s baseline scenario, “we are relatively close to the terminal rate already,” Kazaks said. But uncertainty remains high and there’s “no need to rush.”

ECB (BBG): ECB to Propose Capital Neutral Regulation Changes by Year End

A high-level ECB taskforce will propose capital neutral measures to simplify Europe’s banking rulebook by the end of the year, European finance ministers were told this week, as the debate intensifies over the bloc’s regulatory burden. The scope of the work includes banks’ capital structure the implementation of the final package of Basel reforms, banks’ reporting requirements and their supervision, according to people familiar with the matter. The work is being carried out by group of euro zone governors and supervisory board member Sharon Donnery.

EUROPE (MNI): EPC Summit Gets Underway Shortly

The sixth meeting of the European Political Community (EPC) is due to get underway shortly in the Albanian capital, Tirana. The EPC is formed of 47 countries from across Europe, allowing for wider-ranging geopolitical discussions between leaders than is the case at European Council summits. According to the official schedule, the main topics of conversation at the leaders' roundtables will be Europe's security and democratic resilience, competitiveness and economic security, and mobility challenges and youth empowerment. Given the geostrategic context, it is the former, specifically the situation of the war in Ukraine and the need to increase European defence spending,g that will dominate talks.

EUROPE/CHINA (MNI INTERVIEW): China Agreement Would Need Overhaul - EU Chamber

A European business leader gives insight into a potential restart to trade agreement talks with Beijing. On MNI Policy MainWire now, for more details please contact sales@marketnews.com.

CHINA (MNI): China Calls on APEC to Support WTO Reforms

MNI (Beijing) China has called on APEC members to promote World Trade Organisation reform, including the early inclusion of the Investment Facilitation Agreement and the E-Commerce Agreement into the organisation's legal framework, the Ministry of Commerce said on Friday, citing comments made by Li Chenggang, international trade negotiator and vice minister at the 31st APEC Trade Ministers Meeting in South Korea. Li discussed China’s application to join the Digital Economy Partnership Agreement (DEPA) with current members, highlighting China's determination, ability and actions to meet the high standards of the agreement.

DATA

EUROZONE DATA (MNI): Record Trade Surplus Likely Driven by Tariff Front-Running

The Eurozone trade surplus rose to a record-high E27.9bln in March on a seasonally-adjusted basis. This is E5.2bln more than February's upwardly revised value of E22.7bln, and means in Q1'25, the EZ trade surplus was E64.2bln - around twice the tentative E32.3bln from Q4'24. The jump comes not as a surprise following the US March trade data - the takeaway there was that tariff front-running in particular in the pharmaceutical sector was in place, and Ireland was one of the countries standing out in that regard.

FRANCE DATA (MNI): Employment Absorbs Activity Rate Rise in Q1; Unemployment at 7.4%

The French Q1 ILO unemployment rate was in line with consensus at 7.4%, a tenth higher than Q4's reading. Alongside Eurostat's LFS measure, the unemployment rate has been quite steady between 7.0-7.5% since the start of 2024. Although the activity/employment rates showed encouraging developments in Q1, survey-based data suggests employment prospects ahead are weak. This may filter into higher unemployment rate readings in the coming quarters.

ITALY DATA (MNI): Energy Drives Downward Revision to Italian April HICP

- ITALY APRIL FINAL HICP 2.0% Y/Y (FLASH 2.1%, MARCH 2.1%)

The energy component drove the downward revision to Italian April HICP. Headline HICP inflation was 2.04% Y/Y (vs 2.13% prior, 2.1% flash), with energy at -0.74% Y/Y (vs 2.68% prior, -0.2% flash). A reminder that the few analyst estimates we had seen ahead of the flash release looked for an acceleration in energy to over 4% on a base effect.

HICP details indicate a -9.04% Y/Y rate on liquid fuels (vs -6.46% prior). HICP excluding energy and unprocessed foods was confirmed at 2.13% Y/Y (vs1.90% prior).

JAPAN DATA (MNI): Japan Q1 GDP Posts 1st Contraction in 4 Qtrs

- JAPAN Q1 REAL GDP -0.2% Q/Q; MNI MEDIAN -0.2%

- JAPAN Q1 REAL GDP -0.7% ANNUALIZED; MNI MEDIAN -0.5%

- JAPAN Q1 CAPEX +1.4% Q/Q; +0.2 PP CONTRIBUTION

- JAPAN Q1 CONSUMPTION 0.0% Q/Q; 0.0 PP CONTRIBUTION

Japan’s economy contracted 0.2% q/q, or an annualised 0.7%, over the first quarter, marking the first decline in four quarters, driven by weak private consumption and a sharp rise in imports, preliminary Cabinet Office data showed Friday. The result was slightly weaker than the MNI median forecast of -0.2% q/q, or -0.5% annualised, but broadly aligned with the Bank of Japan’s expectations of a moderate recovery trend despite sluggish consumption. BOJ officials are monitoring how exports perform from April onwards as the impact of U.S. tariffs begins to take hold. Private consumption, which makes up about 60% of GDP, was flat in Q1 after a revised 0.1% rise in Q4. Business investment rose 1.4%, extending gains for a fourth consecutive quarter.

NEW ZEALAND DATA (MNI): Inflation Expectations Rise in Q2, Up From Mid-Point of RBNZ Band

New Zealand's inflation expectations edged up in Q2, per the RBNZ survey. The 2yr ahead expectations rose to 2.29%, from 2.06% in Q1. Expectations had been near 2.0% (the mid point of the RBNZ band) since Q3 last year. We are still well off late 2022 cycle highs of 3.62%, but at face value this isn't a welcome development from an RBNZ standpoint, as it waits to see greater economic traction from its easing efforts. 1yr inflation expectations also pushed higher from 2.41%, versus 2.15% in Q1. 5 yr and 10yr inflation expectations edged slightly higher and remain above 2%.

RATINGS: Updates on Portugal & Greece Eyed After Close

Potential sovereign credit rating reviews of note scheduled for after hours on Friday include:

- Fitch on Greece (current rating: BBB-; Outlook Stable), Luxembourg (current rating: AAA; Outlook Stable) & Slovakia (current rating: A-; Outlook Stable)

- Moody’s on Malta (current rating: A2; Outlook Stable) & Portugal (current rating: A3; Outlook Stable)

- S&P on Cyprus (current rating: A-; Outlook Stable) & South Africa (current rating: BB-; Outlook Positive)

- Morningstar DBRS on the United Kingdom (current rating: AA, Stable Trend)

- Scope Ratings on Portugal (current rating: A; Outlook Stable) & Slovenia (current rating: A; Outlook Stable)

Most of the focus is likely to fall on the Greek and Portuguese updates from Fitch & Moody’s, respectively. We previously outlined the potential for positive action from Moody’s on Portugal in our political risk team’s election preview (vote due this weekend), click for that document. Please use this link to access the indicative sovereign rating review schedule covering the five most notable rating agencies for 2025. Note that this schedule is indicative only and ratings can be reviewed on an ad-hoc basis. Rating agencies may also adjust their schedules during the year.

FOREX: NZD Remains Outperformer as Inflation Expectations Shift Higher

- The New Zealand dollar remains the strongest performer in G10, following the release of inflation expectations data which has shifted higher in the latest RBNZ survey. The 2yr ahead expectations rose to 2.29%, from 2.06% in Q1. Expectations had been near 2.0% (the mid-point of the RBNZ band) since Q3 last year. We are still well off late 2022 cycle highs of 3.62%, but at face value this isn't a welcome development from an RBNZ standpoint.

- NZDUSD (+0.53%) has regained the 0.5900 handle in sympathy, although remains well shy of the week’s high at 0.5969. Solid support for the pair is buildig around the 0.5850 mark.

- The other notable move in G10 was for USDJPY, which finally bridged the gap to last Friday’s close overnight. Some downside momentum picked up following the moves below 145.37, gravitating to a low print at 144.92 before stabilising. Thepair remains broadly unchanged on the week despite the volatile intra-day ranges. Overall, the latest USDJPY pullback underpins the view that gains since Apr 22 appear corrective.

- Elsewhere, ranges across global currency markets have remained contained, as markets continue to digest the plethora of data releases on Thursday, and the data calendar remains relatively calm to end the week.

- As such EURUSD is a tad firmer on the session, consolidating just above 1.12, while GBPUSD is doing the same above 1.33. For cable, Tuesday’s gains highlight a possible reversal pattern - a bullish engulfing candle. If correct, the pattern signals the end of the corrective cycle and a resumption of the uptrend. A continuation higher would refocus attention on the key resistance and a bull trigger, at 1.3444, the Apr 28 / 29 high.

- Import prices, building permits and preliminary UMich sentiment & inflation expectations highlight the US calendar. We may also hear from SNB President Schlegel.

EGBS: Major Futures Rally; 100bp Support Eyed in BTP/Bund

Major EGB futures have rallied this morning, without an obvious headline trigger. Participants appear to have digested this week’s soft US data and weaker oil prices, and taken the opportunity to enter longs at attractive yield levels.

- Bund futures have extended to fresh intraday highs of 130.58 (+65 ticks today), piercing the 20-day EMA at 130.53. Participants may look to close the gap to the May 9 close of 130.76, with round number resistance then seen at 131.00.

- The German curve has bull flattened, with 30-year yields down 6bps.

- The psychological 100bp handle remains the focus for the 10-year BTP/Bund spread, which currently hovers around 100.5bps.

- Broader EGB spreads to Bunds are generally little changed, with GGBs widening slightly. Portuguese and Greek ratings reviews are eyed after the close, with the Portuguese election also crossing over the weekend.

- This morning’s Eurozone data and ECB speakers have not moved the needle. Chief Economist Lane speaks on a panel at 1600BST.

GILTS: Curve Flatter, Futures at Highs

Gilts hold their early rally, after continued adjustment to yesterday’s U.S. PPI data help promote a stabilisation/recovery in wider core global FI markets.

- Some key yield levels in German 10s (2.70%) and U.S. 30s (5.00%) have held over the last 24 hours, which will also be factoring into the rebound.

- Macro headline flow remains limited thus far.

- Futures register a fresh session high at 92.01 at typing, after breaking through first resistance at 91.95. Fresh extension higher would target the 20-day EMA (92.34) and chip further away at the recent bearish move.

- Yields 1.5-5.5bp lower on the day, with bull flattening starting dominate after a parallel ~4bp shift lower in yields in early trade. Steepener trades may still be crowded.

- 2s hold yesterday’s close back below 4.00%.

- SONIA futures flat to +4.5, strip flattens, taking cues from the longer end.

- BoE-dated OIS is little changed to 2bp more dovish on the day across ’25 meetings. 46bp of cuts priced through year-end, with 24.5bp of cuts priced through September and 38bp priced through November.

- Comments from BoE’s Lombardelli due later today, although don’t expect much new from her, as she has already provided plenty of post-MPC decision commentary outlining her support for a “finely balanced” 25bp cut.

- That should leave macro and cross-market cues at the fore for much of the day, with tariff talk, U.S. UoM sentiment data and central bank speak front and centre.

EQUITIES: This Week's Gains Bolster Bullish Outlook for Eurostoxx Futures

A bullish theme in Eurostoxx 50 futures remains intact. Gains this week reinforce current bullish conditions. The contract is extending the recent breach of 5263.01, 76.4% of the Mar 3 - Apr 7 bear leg. The continuation higher signals scope for a climb towards 5516.00, the Mar 3 high and the key bull trigger. Initial firm support to watch lies at 5171.52, the 50-day EMA. Clearance of this level would signal a possible reversal. A bullish trend condition in S&P E-Minis remains intact and this week’s appreciation reinforces current conditions. Price also continues to trade at its latest highs. The contract has cleared an important resistance at 5837.25, the Mar 25 high and a bull trigger. This strengthens the bullish theme, paving the way for a continuation near-term. Sights are on the 6000.00 handle next. Initial firm support to watch lies at 5669.26, the 50-day EMA.

- Japan's NIKKEI closed lower by 1.79 pts or 0% at 37753.72 and the TOPIX ended 1.49 pts higher or +0.05% at 2740.45.

- Elsewhere, in China the SHANGHAI closed lower by 13.359 pts or -0.4% at 3367.462 and the HANG SENG ended 108.11 pts lower or -0.46% at 23345.05.

- Across Europe, Germany's DAX trades higher by 169.66 pts or +0.72% at 23867.05, FTSE 100 higher by 31.81 pts or +0.37% at 8665.68, CAC 40 up 42.93 pts or +0.55% at 7896.41 and Euro Stoxx 50 up 28.38 pts or +0.52% at 5440.66.

- Dow Jones mini up 144 pts or +0.34% at 42529, S&P 500 mini up 15 pts or +0.25% at 5948.25, NASDAQ mini up 56.75 pts or +0.27% at 21458.25.

Time: 09:55 BST

COMMODITIES: Corrective Cycle in Gold Remains in Play

A downtrend in WTI futures remains intact and recent gains are considered corrective. Key resistance to watch is $63.46, the 50-day EMA. It has recently been pierced, a clear break of it would highlight a stronger reversal. This would open $66.41, the Apr 4 high. For bears a reversal lower would refocus attention on $54.67, the Apr 9 low and bear trigger. Clearance of this support would confirm a resumption of the downtrend. A corrective cycle in Gold remains in play and the metal has traded lower this week. A key support at $3202.0, the May 1 low has been breached. The break of this level signals scope for a deeper retracement, towards $3085.0, 76.4% of the Apr 7 - Apr 22 upleg. Note that the 50-day EMA at $3168.0, has been breached, strengthening a bearish threat. Initial resistance is $3265.4, the 20-day EMA.

- WTI Crude down $0.08 or -0.13% at $61.54

- Natural Gas down $0.02 or -0.48% at $3.346

- Gold spot down $33.47 or -1.03% at $3205.61

- Copper down $6.35 or -1.36% at $462

- Silver down $0.4 or -1.22% at $32.2378

- Platinum down $5.54 or -0.56% at $988.63

Time: 09:55 BST

| Date | GMT/Local | Impact | Country | Event |

| 16/05/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 16/05/2025 | 1230/0830 | *** | Housing Starts | |

| 16/05/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 16/05/2025 | 1230/0830 | New York Fed's Roberto Perli | ||

| 16/05/2025 | 1230/0830 | *** | Housing Starts | |

| 16/05/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 16/05/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 16/05/2025 | 1500/1700 | ECB's Lane On Central Bank Communication Panel | ||

| 16/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 16/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 16/05/2025 | 2000/1600 | ** | TICS | |

| 16/05/2025 | 0140/2140 | San Francisco Fed's Mary Daly |